Each month we ask clients to spend a few minutes reading through our newsletter with the goal of raising their investor IQ. June's edition of Timely Topics touches on recent volatility within fixed income markets and what that means for the new Federal Reserve Chairman in the coming quarters. Additionally, we discuss some new economic developments involving China and OPEC and introduce new team members at North Star.

- Running out of reasons to cut

- Bond market reactions

- OPEC-XIT

- US-China summit

- NSAG News

- Where will the stock market go next?

Running out of reasons to cut

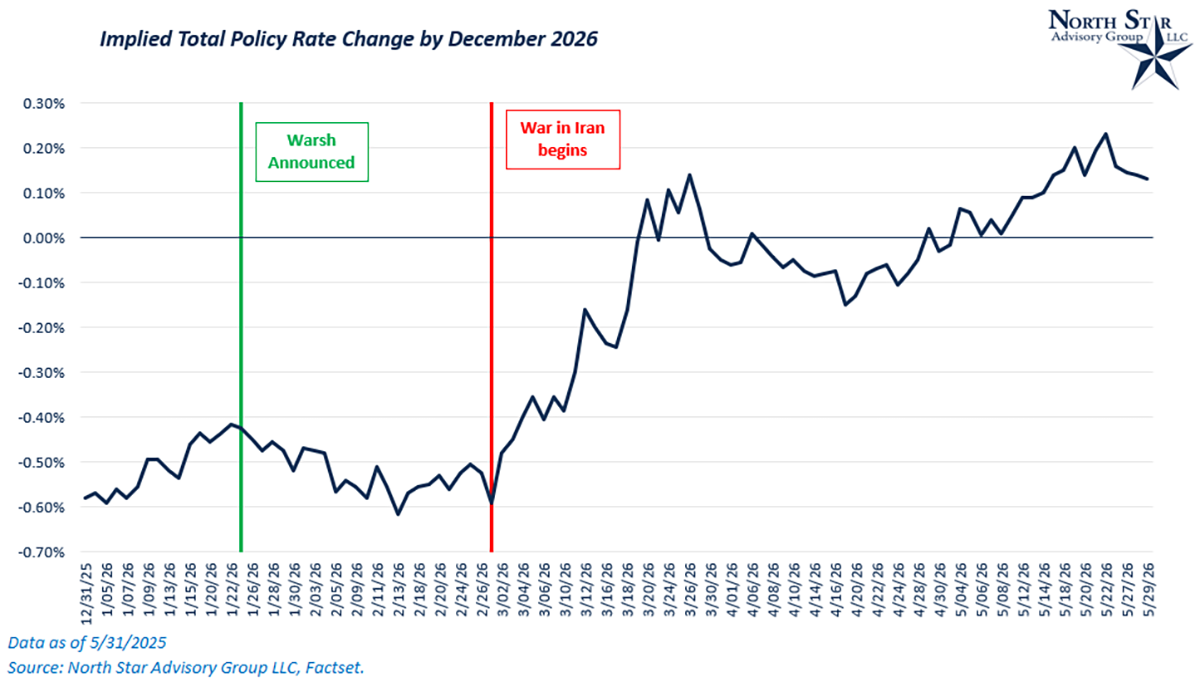

President Donald Trump nominated Kevin Warsh in January 2026 to serve both as a member of the Federal Reserve Board of Governors and as the next Chair of the Federal Reserve, succeeding Jerome Powell. After several weeks of delays tied to Senate concerns over the Fed’s independence and a Justice Department investigation involving Powell, Warsh’s nomination advanced through the Senate Banking Committee in late April. The Senate subsequently confirmed him both to a 14-year term on the Federal Reserve Board and as Chair of the Federal Reserve, officially completing the confirmation process. His confirmation is expected to mark a shift toward a more market oriented and potentially less restrictive monetary policy approach as investors closely watch how the Fed responds to inflation, economic growth, and rising fiscal pressures.

As we’ve discussed in previous Timely Topics articles, Federal Reserve independence has been under threat in the Trump 2.0 administration. Public calls to cut interest rates, DOJ probes into Jerome Powell, and threats of firing have muddied the perception of independence over the past 12+ months. Upon Warsh’s initial announcement, the market began pricing in more rate cuts as investors expected he would eventually deliver at least one or two rates cuts for the administration by the end of the year. This trend was upended by the war in Iran and higher oil prices leading to near term inflationary pressures. There are now zero cuts expected in 2026 as of the end of May, and the market is actually pricing in the probability of one rate hike at some point in ‘26. In the chart below, we used December 2026 Fed futures contract pricing to estimate the total change in the Federal Reserve’s policy through 2026.

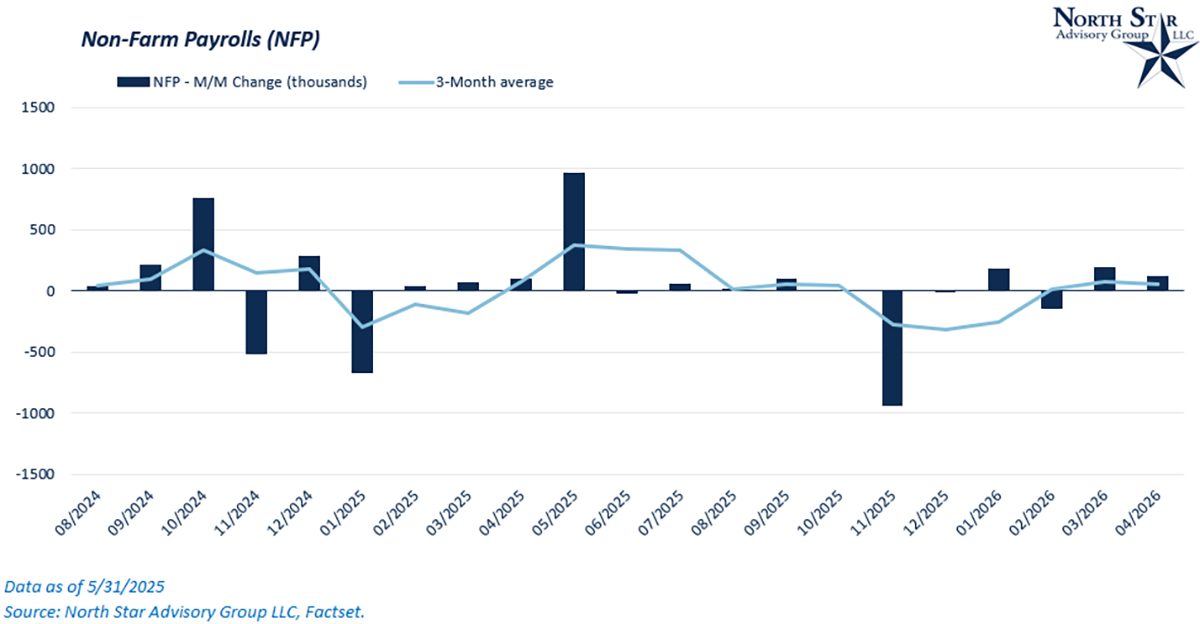

Near term inflationary pressures have taken rate cuts off the table for now, although there are other underlying factors that continue to chip away at the rationale to deliver a rate cut in 2026. While energy-driven inflation is almost always transitory in nature given the volatility of commodities, the job market remains resilient despite AI-driven corporate layoffs. While growth is relatively flat according to the BLS’ NFP report, we are seeing stabilization and no consistent deceleration over multiple months.

The Federal Reserve operates with a dual mandate; price stability and employment. If the economy is not experiencing an increase in unemployment and inflation remains solidly above the target annual rate of 2%, then justifying a cut becomes increasingly difficult.

Bond market reactions

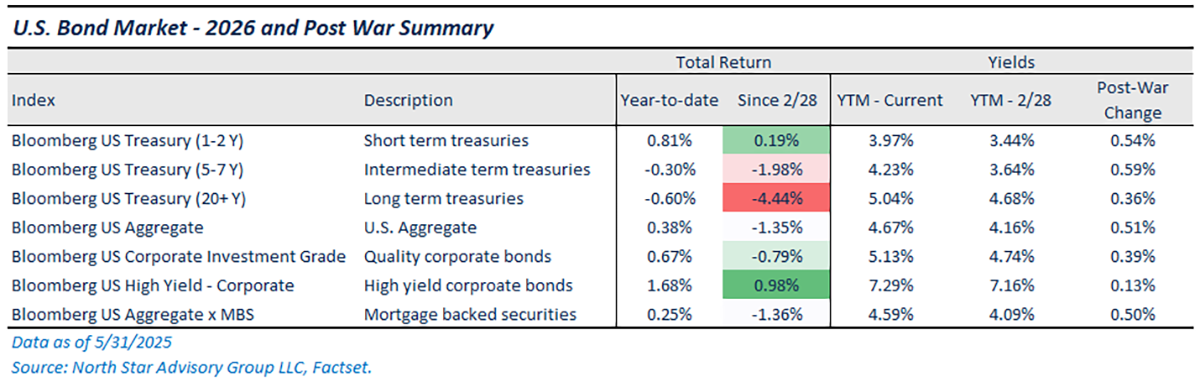

As near-term inflation expectations rise due to disruption in oil supply, treasury rates across the board have increased as well, pushing broad interest rate levels higher across segments. In the table below, we’ve summarized the change in yield levels and the total returns for various bond market segments within the U.S. on a year-to-date basis and since the war in Iran kicked off.

YTM = Yield to maturity

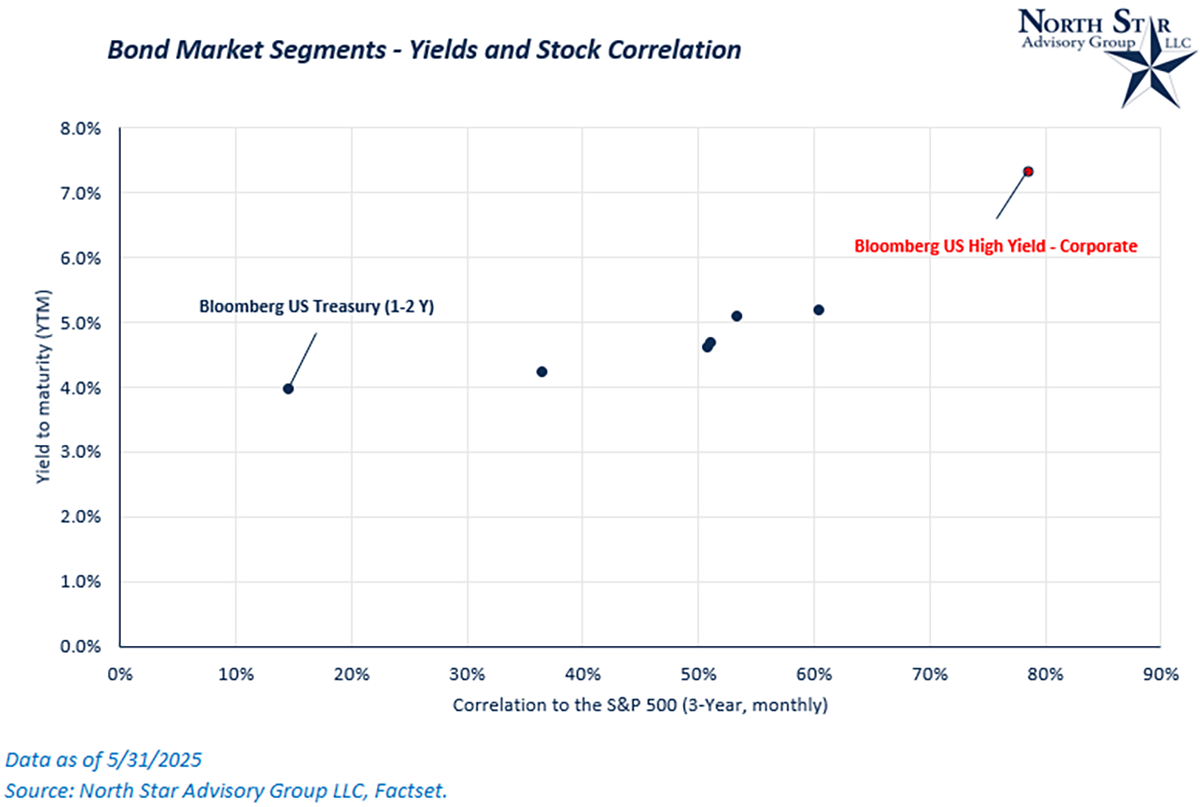

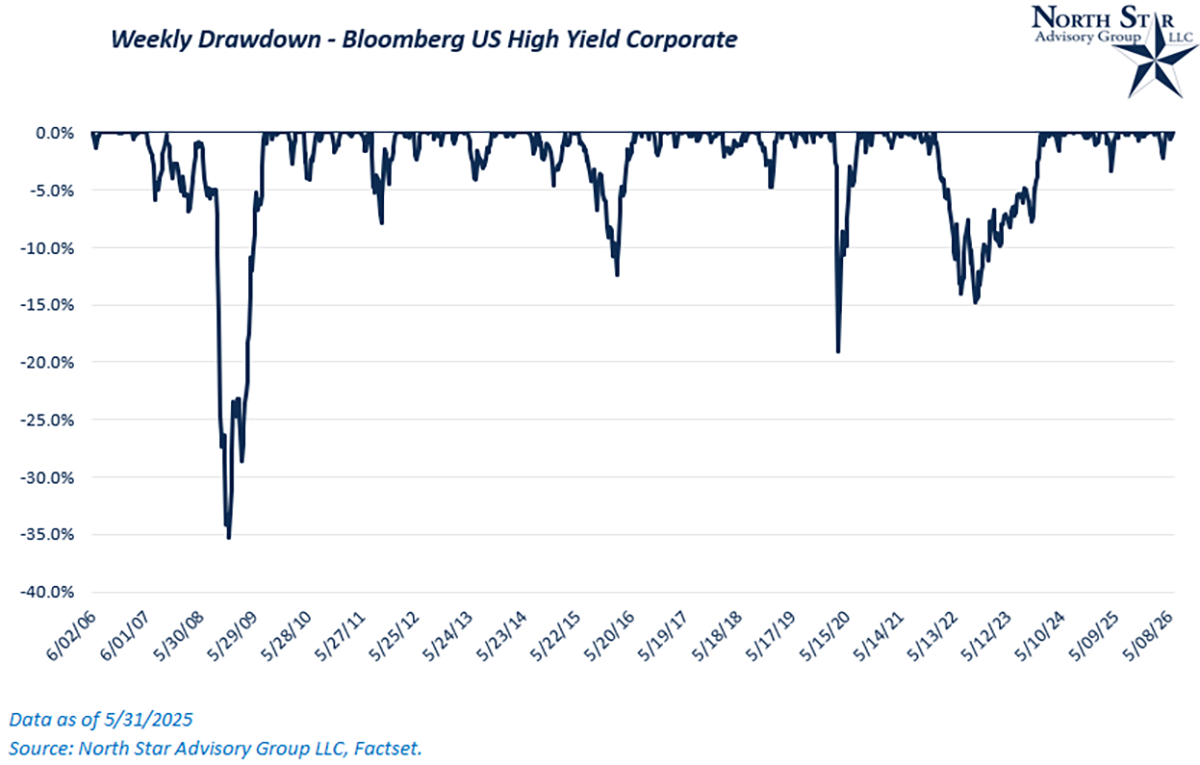

In both time frames listed, high yield bonds have been the best performing bond market segment. High yield bonds typically feature shorter term maturities and an extra yield spread due to credit risk, both of which have mitigated downside risk from higher oil prices in this segment. Defaults have continued to remain low as well. Long duration bonds (Bloomberg US Treasury 20+ Y) have the highest interest rate sensitivity. These bonds are down ~4.5% from just a 0.40% increase in interest rates. Short duration bonds (Bloomberg US Treasury 1-2 Y) has been the second-best performing segment on a year-to-date basis.

While the near-term impacts of war and oil shocks have pushed rates higher, there is still long-term uncertainty around the fiscal budget and what that means for long dated treasury rates. For this reason, we have continued to recommend a shorter duration strategy for fixed income portfolios as of 5/31/2026. While high yield bonds tend to be less sensitive to interest rate movements, the underlying risk associated with these types of bonds is more equity-like in nature and hasn’t provided strong downside protection during periods of economic stress.

OPEC-XIT

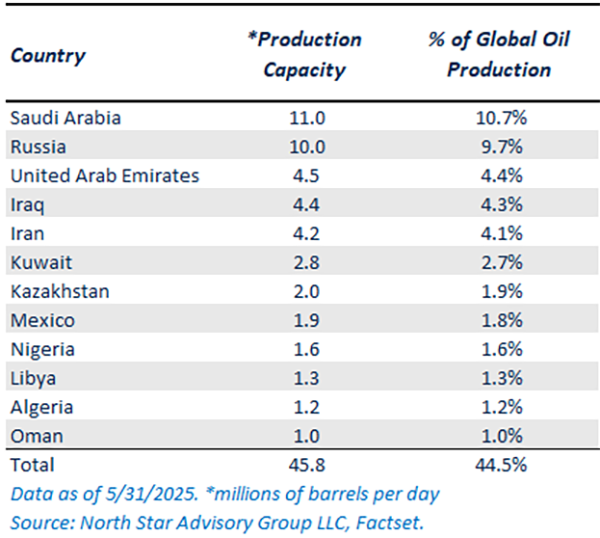

In May, it was announced that the United Arab Emirates (UAE) was leaving OPEC, a group of major oil-producing countries that coordinate oil production policies in an effort to influence global oil prices and stabilize energy markets. Originally, OPEC was founded in 1960 by Iran, Iraq, Kuwait, Saudia Arabia, and Venezuela after growing dissent of western nations’ influence over the price and production of the critical commodity. Since its founding, the group has expanded to include various other African, Middle Eastern (including the UAE), and Latin American nations. Most critically, Russia is included within “OPEC+”.

With the UAE being the group’s third most influential member, their departure will likely cause additional short-term volatility in oil markets and create long-term impacts to pricing. In recent years, the UAE has invested heavily into oil production capacity. They are now capable of producing 5-6 million barrels per day. Although, these investments are not able to be capitalized on if OPEC decision making puts a cap on production.

What does this mean in the long run? In our view, this could lead to pressure on oil prices if the UAE continues to expand capacity and utilize that capacity to its full potential. Commodity prices are extremely sensitive to supply and demand dynamics, and any incremental increase in supply can push down prices. The UAE has also seen its economy diversify into other sectors and industries including financial services, logistics, tourism, and AI/technology, so they have become less dependent on maximizing oil prices. This departure may also prompt other member nations to reconsider their place in OPEC. Saudi Arabia, the group’s most influential member, has also been investing heavily to diversify its economy.

US-China Summit

The mid-May summit between President Donald Trump and Chinese President Xi Jinping was viewed by markets as an important step toward stabilizing the relationship between the world’s two largest economies. While the meeting did not produce a major breakthrough on the deeper strategic disputes between the two countries, it did reduce fears of an immediate escalation in tariffs, sanctions, and trade restrictions. Both sides agreed to continue negotiations on trade and investment issues and established new economic dialogue mechanisms intended to improve communication and reduce future disruptions.

One of the most important outcomes was a partial easing of trade tensions. China reportedly agreed to increase purchases of U.S. agricultural products and Boeing aircraft, while both countries signaled openness to reducing tariffs on certain non-strategic goods. The summit also produced limited progress on technology and supply chain issues. The United States modestly relaxed restrictions on some lower tier semiconductor exports, while China eased certain rare earth export controls. However, restrictions involving advanced AI chips, military technology, and critical semiconductor equipment remain firmly in place.

Economically, the summit improved investor confidence by lowering the probability of a near term trade war or severe supply chain disruption. This was particularly positive for industrial companies, exporters, transportation firms, and multinational corporations with significant exposure to Chinese markets and manufacturing. Companies such as Boeing, Apple, Tesla, and several semiconductor firms benefited from improving sentiment around trade stability and cross border commerce. The agreement also modestly reduced concerns about a global economic slowdown by improving corporate visibility and encouraging investment activity.

Despite the constructive tone, markets still view the long-term outlook as uncertain. The summit did not resolve the underlying competition surrounding Taiwan, artificial intelligence, semiconductors, or national security policy. As a result, investors increasingly expect a future defined by managed economic competition rather than full normalization between the United States and China. In the near term, the summit was supportive of stocks and risk assets, but markets are likely to remain highly sensitive to future geopolitical developments and policy shifts between the two countries.

NSAG News

As we indicated in our 2025 holiday card, NSAG kicked off May with a new hire and 3 student interns at our office!

NSAG continues our commitment to giving back to our industry and support our client driven long-term growth. Our new hire will initially come on as a Paraplanner as he mentored towards eventually becoming a Financial Advisor to support NSAG clients. Interns on the other hand are provided with a comprehensive overview of our firm and industry to help them determine their personal interests in pursuing a career in our field and what development opportunities they would like to explore. All internships emphasize meaningful, hands-on experience with structured professional support.

Matthew Bechtol

Matthew Bechtol

Paraplanner / New Full Time Hire

Matthew started at North Star Advisory Group in 2026 as a paraplanner. He is responsible for coordinating client meetings, including scheduling, collecting, and analyzing necessary information. In addition, he prepares client investment reviews and retirement cash flow projections, as well as assists with the overall client relationship.

Matthew graduated Magna Cum Laude in 2026 from Bowling Green State University with a Bachelor of Science in Business Administration, specializations in Finance and Accounting, and a concentration in Financial Planning. He will continue his educational pursuits by working towards completing professional certifications including but not limited to the Financial Paraplanner Qualified Professional™, Ohio Notary, Series 65 exam, Ohio Insurance exam for Life and Health, and Certified Financial Planner™.

Originally from Findlay, OH, Matthew currently lives in Willoughby Hills, Ohio. Outside of work, he enjoys disc golfing, watching the Cleveland Guardians, Seattle Kraken, and Pittsburgh Steelers, and volunteering at his local church. Matthew’s favorite thing to do on the weekends is to play music on piano and guitar and enjoy time with friends and family. His bucket list includes enjoying a baseball game at every Major League Baseball stadium, visiting all 50 states in the United States, and one day watching the Cleveland Guardians win the World Series.

Riley Barczyk

Financial Planning Intern

Riley Barczyk

Financial Planning Intern

Riley serves as our Summer 2026 Financial Planning Intern and plays an integral role in supporting both our advisory team and client experience. She assists with gathering and analyzing key financial information to help prepare for client meetings, ensuring that our advisors have accurate and organized data to deliver thoughtful, personalized guidance.

Riley is actively involved in preparing client investment reviews and developing retirement cash flow projections. Her work helps provide clients with a clear understanding of their financial position and long-term outlook. In addition, she contributes to maintaining and strengthening client relationships by supporting ongoing communication and service needs.

Through her role, Riley gains hands on experience across a wide range of planning areas, including retirement plan analysis, investment strategy, and comprehensive financial planning. She supports work related to various retirement accounts such as IRAs, Roth IRAs, SIMPLE IRAs, SEP IRAs, 401(k), 403(b), and 457 plans.

Riley also assists in evaluating insurance solutions, including life insurance and long-term care coverage, helping ensure clients are protected as part of their broader financial plans.

Her experience extends across our full suite of services, including:

- College planning

- Financial planning

- Investment consulting and selection

- Retirement savings strategies

- Retirement plan rollovers

- Retirement cash flow planning

- Insurance planning

- Estate and tax planning

- Trust services

Riley’s attention to detail, analytical mindset, and commitment to client service make her a valuable member of our team as she continues to build her expertise in financial planning.

Riley is graduating in May of 2027 from Bowling Green State University with a Bachelor of Science in Business Administration, specializing in Finance, Accounting and International Business, with a concentration in Financial Planning. After graduation, she will continue her educational pursuits by working towards completing professional certifications including but not limited to the Financial Paraplanner Qualified Professional™, Ohio Notary, Series 65 exam, Ohio Insurance exam for Life and Health, and Certified Financial Planner™.

Riley currently lives in Medina, Ohio. Outside of work, she enjoys hiking, reading and spending time with family and friends. Riley’s favorite thing to do on the weekends is to explore new places.

Chris Barone

Chris Barone

Economics and Financial Analysis Intern

To ensuring a well-rounded professional development experience, Chris is receiving direct mentorship from NSAG’s CFA, Brian Duffield, along with additional guidance from a team of Certified Financial Planners and an attorney.

Under this mentorship, Chris will gain exposure to several core areas of investment analysis, including company research, evaluating macro and microeconomic factors, understanding competitive positioning, and learning fundamental valuation techniques such as discounted cash flow modeling. While these concepts may seem straightforward at a high level, the internship is designed to build the depth and discipline required to apply them effectively.

Chris’s summer internship will culminate in a formal stock presentation to the NSAG staff. After narrowing his focus to a single company, he will conduct a full analysis that incorporates economic context, competitor evaluation, and intrinsic valuation. The final presentation will demonstrate both technical rigor and the ability to communicate insights clearly at a higher level, making complex financial concepts accessible and easy to understand.

In the fall, Chris will return to Bowling Green State University where he is working towards his bachelor’s degree in Applied Economics. In his spare time, he is a College of Business Peer Leader, President of the AI Safety and Ethics Foundation as well as a Member of Economics Club.

Anderson Morrissey

Anderson Morrissey

Orange High School senior shadowing program

All seniors at Orange High School complete a real-world shadowing opportunity before graduating, and Anderson made a great impression during his time with our team. He had a chance to prepare for and sit on in client meetings. One unique project that he worked on was evaluating the rates of returns from his sneaker trading business.

Anderson graduated on May 31, 2026 and will be heading to Coastal Carolina University to major in Finance. He is currently exploring whether to pursue a specialization in Financial Planning or Financial Analysis, and we are confident he has a bright future ahead.

Where will the stock market go next?

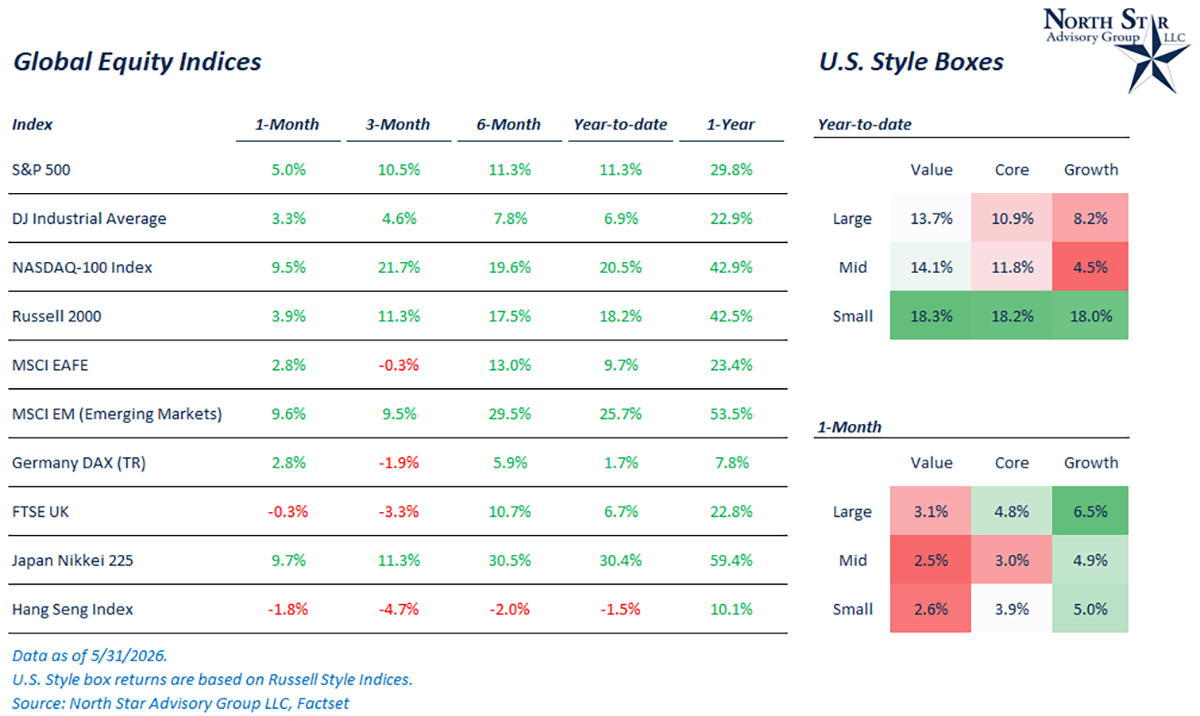

As we enter into the summer months, stock markets continue to show strength despite volatility tied to the war in Iran. While most indices were positive in May, technology was the leader of the pack. The Nasdaq 100 Index, the index tracking the 100 largest technology firms in the U.S., was up by 9.5% in May. Looking at sub-components of the tech sector, hardware stocks were the driving force of strong sector returns. As one might expect, this was due to continued optimism and increased earnings expectations within the broader AI trade and infrastructure build. With many of the LLM companies (OpenAI, Anthropic, etc.) rolling out agentic tools and products, the demand for computing power continues to rise. In May, the PHLX Semiconductor Index (SOX) was up by 21%. Additionally, the MSCI Emerging Markets index was up by 9.6% in May, as many companies within Taiwan and South Korea are critical to the AI infrastructure.

With recent market highs being driven largely by enthusiasm surrounding artificial intelligence, comparisons to the dot-com bubble have become increasingly common across financial media, research reports, and social media platforms. Opinions on the outlook vary widely, with some commentators warning of an imminent market correction while others argue that the growth trajectory for semiconductor and AI-related companies remains in its early stages. NSAG discussed some of these conversations in November’s Timely Topics article “Is the AI era the new dot-com era?”.

At NSAG, we believe the most likely outcome lies somewhere between these two extremes. While elevated valuations and investor enthusiasm warrant caution, the transformative potential of artificial intelligence is creating real economic value and long-term growth opportunities. As is often the case in both investing and life, the truth is rarely found at either end of the debate, but rather somewhere in the middle

While semiconductor stocks continue to rally, the earnings expectations continue to rise as well. This is a stark contrast in comparison to dot-com. The aggregate EPS expectations for the SOX index in 2026 have been revised upwards by ~30% and ~36% for 2027 since the end of February.

We are passionately devoted to our clients' families and portfolios. Contact us if you know somebody who would benefit from discovering the North Star difference, or if you just need a few minutes to talk. As a small business, our staff appreciates your continued trust and support.

Keep sending your questions for a chance to be featured in next month’s Timely Topics.

Best regards,

Mark Kangas, CFP®

CEO, Investment Advisor Representative

Brian Duffield, CFA®

Co-Portfolio Manager & Market Strategist