Each month we ask clients to spend a few minutes reading through our newsletter with the goal of raising their investor IQ. November's edition of Timely Topics dives into the comparison between today’s AI era and the dot-com era of the late 90s. We compare and contrast themes and patterns found within each era and discuss the potential risks and performance.

- Is the AI era the new dot-com era?

- Circular deals

- Index exposure

- Index performance

- NSAG News

- Where will the stock market go next?

Is the AI era the new dot-com era?

In the summer of 1995, Netscape’s IPO ignited what became known as the dot-com boom. More than 20 years later, the release of ChatGPT in November 2022 sparked a similar wave of enthusiasm, this time centered on artificial intelligence. Both moments marked turning points when a new technology captured investors’ imaginations and reshaped market behavior. The question now is whether the AI era is simply a replay of the internet bubble, or if important differences will alter the outcome.

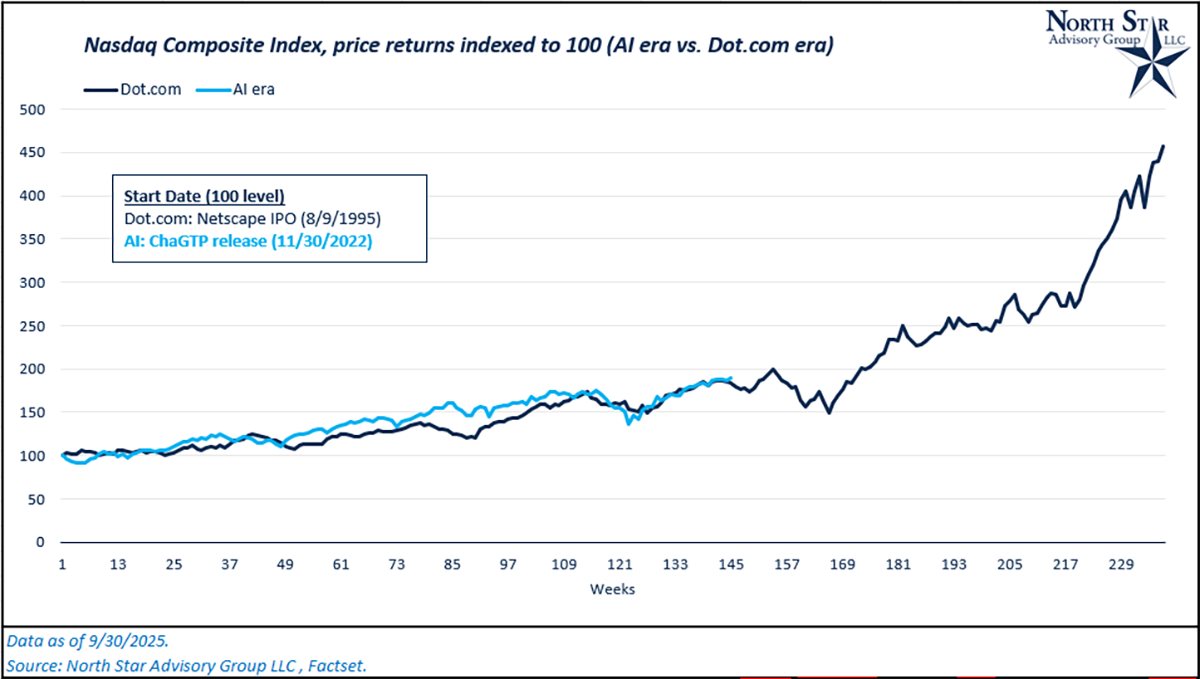

The Nasdaq Index offers a useful lens for comparing the two periods. In the 34 months following Netscape’s IPO, the Nasdaq rose about 84 percent. Over the same stretch since ChatGPT’s debut, it has gained roughly 89 percent. The pace of appreciation has been nearly identical, reflecting how quickly investors in both eras assigned high valuations to companies positioned to benefit from transformative technology.

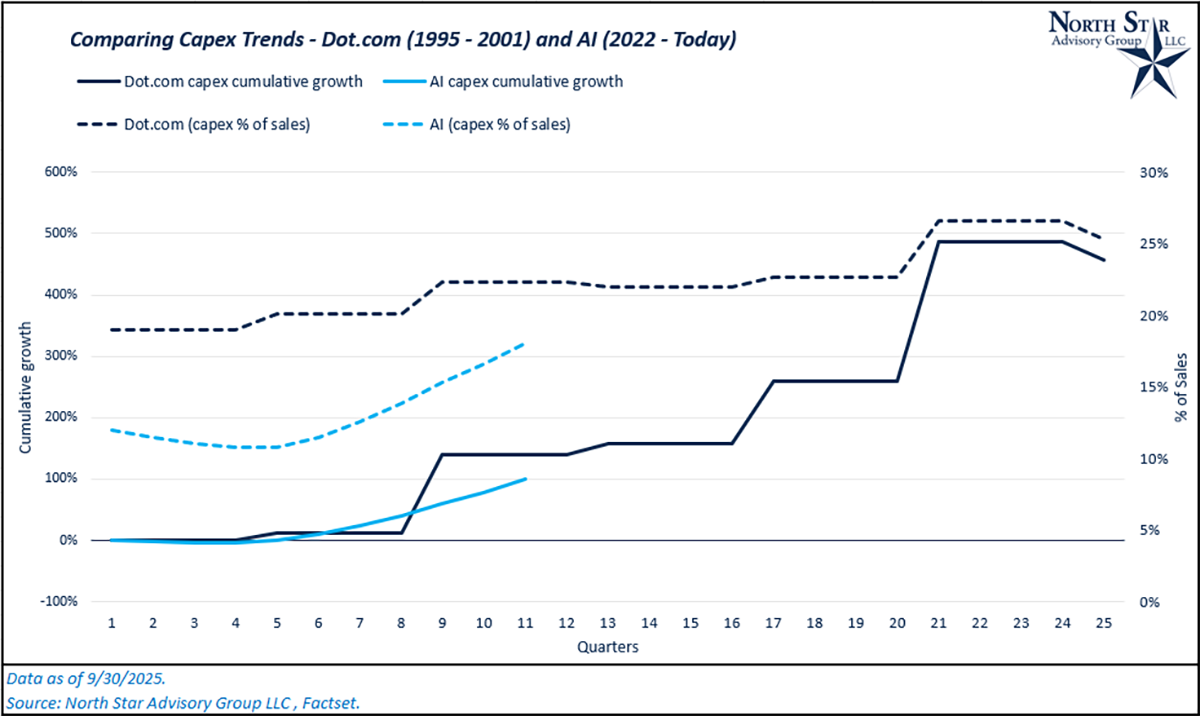

Behind each rally lies a powerful story of infrastructure buildout. In the 1990s, telecom companies raced to lay fiber optic cables and expand networks, pushing capital expenditures up about 144 percent and to 22 percent of sales. In today’s AI cycle, hyperscalers are driving a similar surge. Spending on data centers, GPUs, and networking equipment has nearly doubled, up about 99 percent, and now represent roughly 18 percent of aggregate sales. In both cases, companies poured money into the physical foundations of a new digital frontier.

The parallels are clear. Both periods saw rapid market gains, aggressive infrastructure spending, and a shared belief that a new economy was emerging. In the 1990s, the internet defined the future. In the 2020s, it is AI. Yet the contrasts are equally important. Many dot-com companies had little or no revenue, while AI is being embedded into profitable products at scale. Telecoms once faced commoditized businesses, whereas today’s hyperscalers integrate capital spending into already lucrative platforms. The macro backdrop also differs. A portion of the 1990s were marked by falling rates and a productivity surge, while today’s environment combines higher rates with strong corporate balance sheets and persistent demand for computing power. Adoption speed further distinguishes the two eras: the internet took years to reach scale, while AI applications have reached hundreds of millions of users in months.

History shows that rapid buildouts do not always reward the builders. Telecom firms learned that lesson when their investments led to overcapacity and financial strain. Hyperscalers may prove more resilient thanks to integrated platforms, but investors should still watch whether earnings growth keeps up with expectations. The dot-com bust did not end the internet; it marked a difficult middle chapter in a lasting transformation. The AI boom may rhyme with that history, but stronger business models, faster adoption, and greater financial strength suggest the outcome will be different. The real question is no longer whether AI will reshape the economy, but how far its impact will reach.

Circular deals

One of the defining features of the current AI investment cycle is the rise of what might be called “circular” deals. These are arrangements where a company invests in or finances another firm that, in turn, becomes a major customer of the investor. The setup guarantees demand, supports aggressive growth targets, and creates a self-reinforcing loop of spending and revenue recognition. While such deals can make strategic sense, they also carry risks of overdependence, inflated valuations, and misallocated capital.

A clear example is Nvidia’s recently announced $100 billion partnership with OpenAI. Nvidia will help fund new data centers built around its hardware, while OpenAI commits to purchasing large quantities of Nvidia GPUs to power its models. In effect, Nvidia is investing to secure future sales of its own products. Similar arrangements are emerging across the AI ecosystem, as hyperscalers, infrastructure providers, and chipmakers strike multi-billion-dollar agreements that both finance and guarantee demand for the technology stack they control.

The pattern is not new. During the dot-com era, companies often blurred the lines between investor, supplier, and customer. Cisco, for example, invested in infrastructure ventures like Equinix, whose internet exchanges relied heavily on Cisco equipment. Telecom companies poured billions into networks built in tandem with content providers and ISPs that promised to drive traffic across them. In many cases, capital effectively flowed in circles, with companies funding their own demand.

The parallels are instructive. Just as dot-com infrastructure spending often exceeded real demand, today’s AI-driven capex boom risks building capacity faster than it can be monetized. These self-reinforcing deals can inflate near-term revenue but also raise concerns about sustainability if adoption fails to match expectations. When investor enthusiasm cools, the logic behind these arrangements can unravel quickly.

For investors, the lesson is not to dismiss these deals outright but to approach them with skepticism. They may accelerate adoption and help dominant players consolidate power, yet they also reflect the same vulnerabilities that defined the late 1990s: capital chasing narrative, overstated projections, and the risk of stranded assets. As history rhymes once again, the challenge is to distinguish between genuine, durable demand and growth that is, in large part, self-financed.

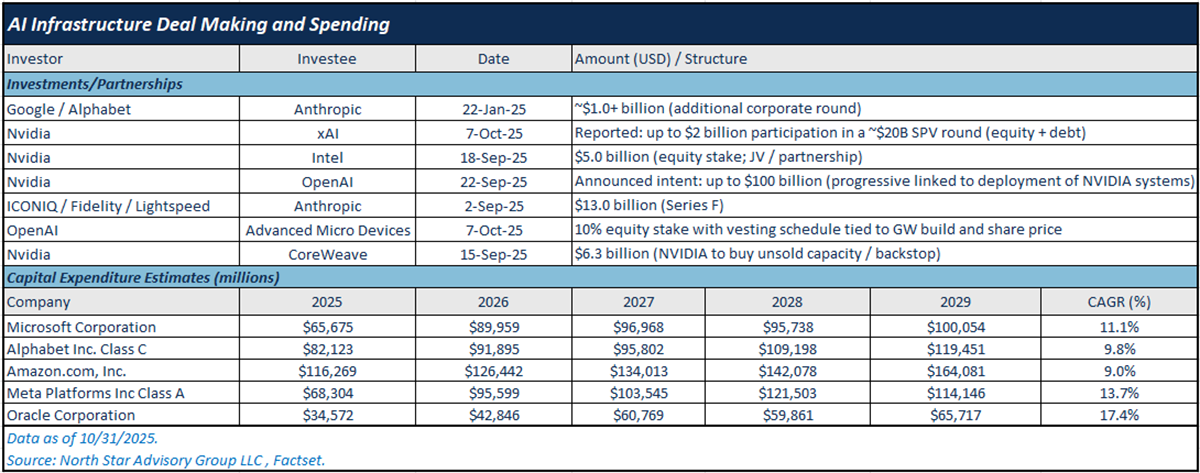

The table below highlights several examples of major AI infrastructure deals announced in 2025 that illustrate this dynamic. We’ve also included capital expenditure estimates for various hyperscalers.

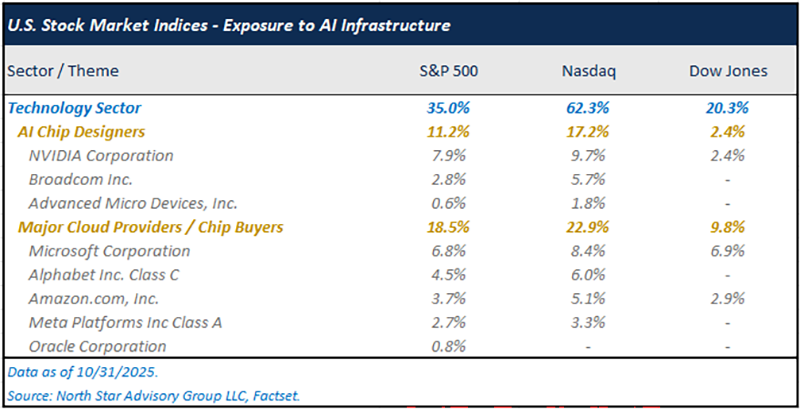

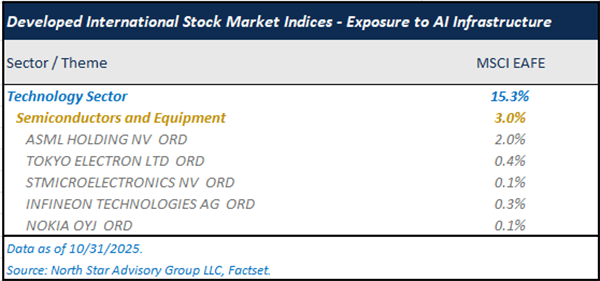

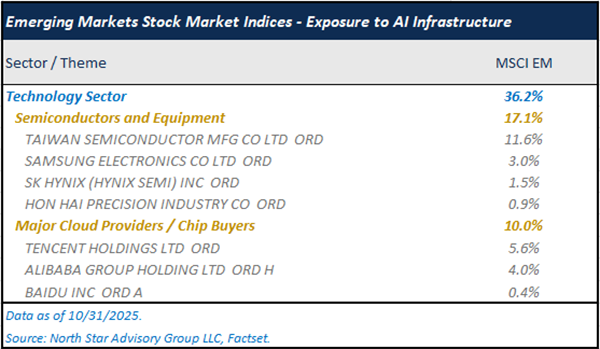

Index exposure

The market’s fascination with artificial intelligence has not only reshaped corporate investment behavior but also redefined the composition of the world’s most followed stock indices. The same companies driving the buildout of AI infrastructure now anchor the performance of U.S. benchmarks to an unprecedented degree. Their dominance has created a feedback loop in which index-weighted capital flows reinforce valuations, and valuations in turn drive index performance. As investors gain exposure through passive vehicles, they may be assuming more concentration risk in AI infrastructure than they realize.

While the S&P 500 and Nasdaq 100 have become heavily tilted toward these AI enablers, other indices tell a different story. The Dow Jones Industrial Average remains only modestly exposed because its price-weight structure limits the influence of large technology names. Outside the United States, the MSCI EAFE index has far less exposure to companies involved in building AI infrastructure. This index, which includes European, Japanese, and Australian firms, contains a few notable semiconductor equipment makers, but at much lower weightings than their U.S. counterparts. The MSCI Emerging Markets index shows more comparable exposure to the S&P 500, driven by companies tied to the AI hardware supply chain, particularly in Taiwan. China, the largest country weighting, contributes through its data center and cloud providers.

The table below highlights the double-digit exposure of both the S&P 500 and Nasdaq 100 to companies such as Nvidia and Broadcom, which design chips used in AI data centers including GPUs, ASICs, and CPUs. Nvidia is included in the Dow as well, though with a smaller influence because of the index’s price-weighted structure.

Market-cap weighting: weights stocks by their total market value (larger companies have more influence). Price-weighting: weights stocks by their share price (higher-priced stocks have more influence regardless of company size).

The MSCI EAFE index includes several key players in the AI hardware supply chain, such as ASML, which produces ultraviolet lithography machines that enable faster, denser, and more efficient microchips.

The MSCI Emerging Markets index has roughly 27% of its weight in AI infrastructure companies, though these firms participate far less in circular financing arrangements and operate within increasingly regionalized supply chains across the Asia-Pacific region, with TSMC remaining a major global exception.

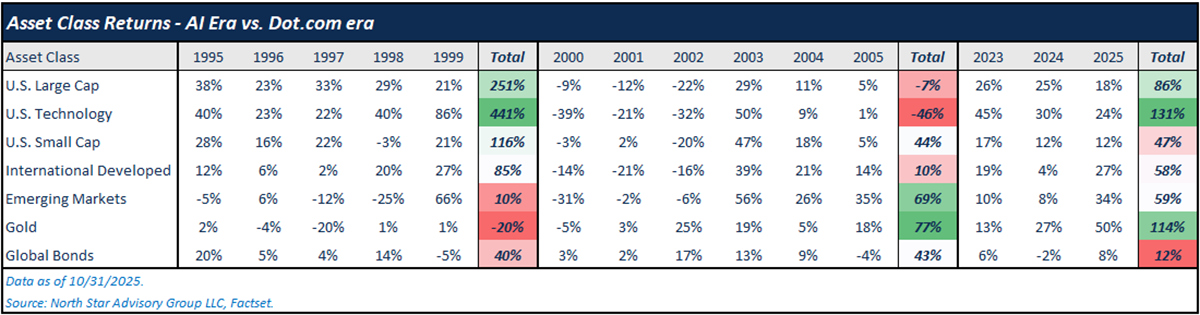

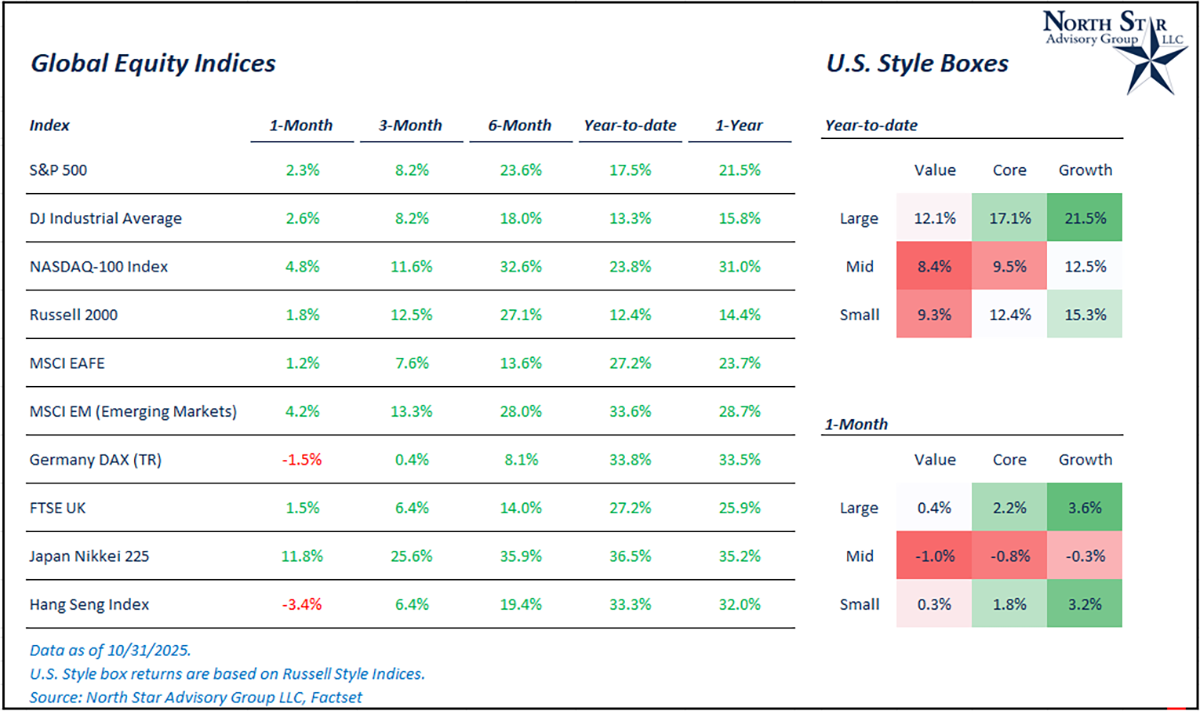

Index performance

If history doesn’t repeat, but it rhymes, the melody of market leadership during technological revolutions sounds strikingly familiar. In the late 1990s, technology stocks led an extraordinary surge that lifted major equity indices, with the Nasdaq and S&P 500 driven by a narrow group of growth names. From 1995 to 1999, U.S. technology returned more than 440%, far outpacing every other asset class. When the bubble burst, leadership flipped as technology fell nearly 70% from 2000 to 2002, while small cap, international developed, emerging markets, gold, and global bonds all outperformed during the 2000 to 2005 period.

Two decades later, the pattern is beginning to rhyme. Since 2023, AI-linked technology stocks have again powered market indices to outsized gains, while other asset classes have moved unevenly. Index performance is once more concentrated in a handful of companies, tied to a single transformative theme: the buildout of artificial intelligence. The key question is whether this cycle will follow the same arc of dominance and correction that defined the dot-com boom, or if the stronger balance sheets and profitability of today’s leaders will allow the rhyme to end differently. Notably, small cap and international developed stocks now trade at lower relative valuations, similarly to how they outperformed during the post-2000’s rotation.

Unlike the internet upstarts of the early 2000s, today’s AI leaders such as Amazon, Google, and Meta entered this cycle with durable earnings and established business models. This may limit the downside if AI spending normalizes, though risks remain. The table below also highlights how monetary policy diverges from the past. Gold, which fell in the late 1990s but rallied after 2000, has nearly matched U.S. technology returns since 2023, reflecting years of easy monetary policy and post-pandemic inflation.

In this environment, diversification and disciplined risk management remain essential. While it may be premature to turn away from hyperscalers entirely, investors should recognize how concentrated leadership and shifting macro conditions can alter the rhythm of market performance.

NSAG News

In October, North Star Advisory Group (NSAG) CEO Mark Kangas, along with team members Forrest Kuchling and Nick Stern, visited Bowling Green State University’s Schmidhorst College of Business to speak with more than 50 finance students. The presentation offered valuable insights into the world of Registered Investment Advisory (RIA) firms, highlighting current industry trends, the evolving landscape of financial planning, and the growing importance of fiduciary client care. Mark and his team also shared practical advice on career development, including internships, networking, and resume-building, giving students a meaningful connection between academic study and real-world experience.

This visit reflects NSAG’s deep commitment to fostering the next generation of financial professionals and its belief that the industry grows stronger through education and collaboration. By engaging directly with students and universities, NSAG helps prepare future advisors while reinforcing its core values of transparency, client-centered service, and continuous improvement. The presentation at BGSU underscores NSAG’s dedication to both its clients and the broader financial community, demonstrating the firm’s ongoing investment in knowledge, people, and progress.

Where will the stock market go next?

October saw a return to tariff volatility in the market. Trade war fears between the U.S. and China reignited after a rapid series of tit-for-tat moves. It began when China imposed new export controls on rare earths and tech materials and blacklisted 14 foreign firms, prompting President Trump to threaten 100% tariffs and tighter export bans in retaliation. Beijing hit back with increased port fees on American vessels, and sanctions against U.S. affiliates tied to shipbuilding. Both sides escalated rhetoric, with China vowing to “fight to the end,” while Washington signaled talks were still possible. The clash over rare earths, semiconductors, and shipping marked the sharpest flare-up in U.S.–China trade tensions since April.

We continue to believe the recent market volatility stemming from this trade tension is temporary and primarily driven by political posturing. We view these actions as negotiating tactics rather than the start of a prolonged trade conflict, similar to our view in the first quarter with reciprocal tariffs. As of the end of the month, both Trump and China’s Xi Jinping agreed to a temporary truce over trade war escalations, roughly two weeks after the flare up began. While anything is possible, we continue to view any potential future trade tensions with a similar lens.

Performance in October was driven by a slew of AI infrastructure announcements. Multiple technology companies, particularly chip designers, saw outsized gains off the backs of infrastructure spending announcements. The technology focused Nasdaq 100 Index gained 4.8% while the S&P 500 gained 2.3%. U.S. small cap stocks gained 1.8% during the month. Emerging Markets stocks continued to perform positively, gaining 4.2%, although reignited trade tensions put pressure on Chinese names.

We are passionately devoted to our clients' families and portfolios. Contact us if you know somebody who would benefit from discovering the North Star difference, or if you just need a few minutes to talk. As a small business, our staff appreciates your continued trust and support.

Keep sending your questions for a chance to be featured in next month’s Timely Topics.

Best regards,

Mark Kangas, CFP®

CEO, Investment Advisor Representative

Brian Duffield, CFA®

Co-Portfolio Manager & Market Strategist