Each month we ask clients to spend a few minutes reading through our newsletter with the goal of raising their investor IQ. February's edition of Timely Topics focuses on the market impact of conflicts in Greenland and Venezuela, how credit card interest rates are priced, and a rotation in U.S. stock markets.

- Venezuela

- Greenland

- Credit card interest caps

- New year, new leadership

- NSAG News

- Where will the stock market go next?

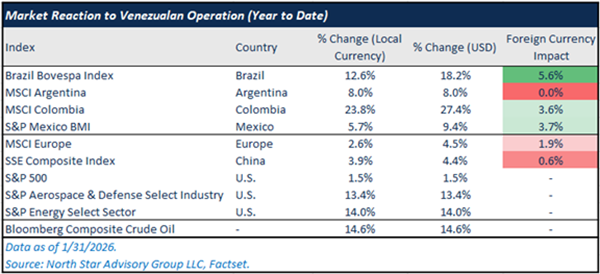

Venezuela

In early January 2026, the United States launched a major military operation in Venezuela that culminated in the capture of President Nicolás Maduro and his wife in Caracas. U.S. forces executed a coordinated strike involving airpower, special operations units, and intelligence assets, a highly unusual intervention in Latin America. Maduro was transported to the United States to face federal charges, including drug-related offenses.

Following the operation, the U.S. has begun scaling back its naval presence around Venezuela, though significant military and diplomatic involvement is likely to continue. The new Venezuelan interim leadership faces pressure to maintain order and cooperate with U.S. economic and security objectives, particularly regarding oil exports.

The immediate market impact in the following month saw Latin American stocks rise broadly, most notably in Brazil and Colombia, two bordering nations of Venezuela. We also saw currency strength in these countries be additive towards total stock gains in that short time frame. Oil prices (Bloomberg Composite Crude Oil Index) rose by ~15%. While we’d expect a theortetical increase in supply to put pressure on prices, there has also been growing tension with the U.S. and Iran which has taken over the short term narrative for oil prices. Additionally, the broad market narrative is that U.S. companies will begin extracting and exporting Venezuela’s oil reserves globally, but the majority of the drilling infrastructure in Venezuela needs significant capital investment to return to full production capacity. This timetable remains unclear and will likely be a multi-year process.

From a long-term perspective, if the situation in Venezuela stabilizes and its oil industry gradually returns to production under new frameworks, Brazil, Colombia, and other Latin American nations might benefit from improved regional energy flows, lower risk premiums, and expanded markets, although this would likely unfold over years rather than months. There is a risk that some of the major Latin American nations continue to further lean on eastern partnerships (Such as China and Russia) as both Brazil and Colombia strongly condemned the operation. Brazil is an original member of the BRICS organization.

Greenland

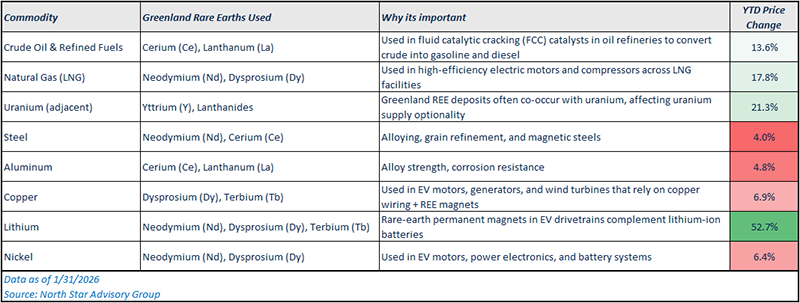

As global competition over critical minerals intensifies, Greenland has emerged as a strategic focal point in U.S. foreign and economic policy. Rare earth elements are essential inputs for advanced manufacturing, clean energy, defense systems, and emerging technologies, and their global supply is currently dominated by Chinese production and processing. This concentration has created supply chain vulnerabilities that concern policymakers across party lines. From national security hawks to clean energy advocates, there is growing bipartisan agreement that reducing dependence on a single foreign supplier is a strategic necessity. In this context, Greenland’s untapped rare earth potential, combined with its geographic importance in the Arctic, has elevated U.S. interest as part of a broader effort to diversify supply chains, strengthen allied resource access, and safeguard long term economic and security interests.

We aren’t here to decide or judge whether the actions/approach taken by the current administration are too harsh, not far enough, or anywhere in between. We want to view this situation through the lens of the market. In the table below, we’ve summarized the various commodities that use Greenland’s known rare earths in their production process.

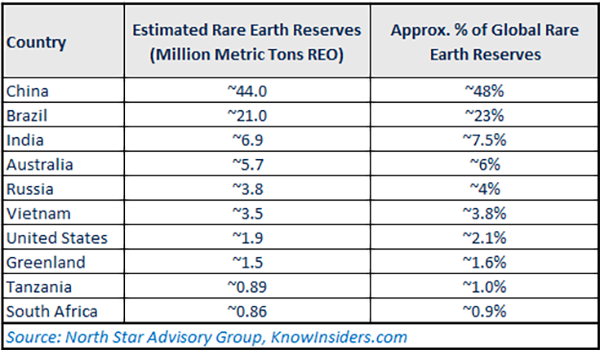

While Greenland’s rare earth reserves are dwarfed by countries like China and Brazil, control of the country would effectively increase the United States’ share of global rare earth reserves by ~80%. After 2025’s trade tension flare ups with China led to the CCP weaponizing their dominant control over rare earth supply, the administration was likely emboldened further to act, and we are now seeing this play out in real time. Initially there was significant European opposition to the administration’s attempt to control Greenland, and the market had mostly looked past this as the majority of expectations were that this will end in some sort of compromise between the U.S. and Denmark. Unsurprisingly, the potential conflict appeared to be resolved as Trump met with Nato leaders at the World Economic Forum. Tariff threats on European nations who opposed U.S. ownership of Greenland were rolled back and a deal was struck. While we don’t currently know the full scope of the deal, we know that it involves guarantees to the U.S. over Greenland’s rare earth deposits and “total” military access in the region.

Credit card interest caps

As part of his broader economic agenda, President Donald Trump has proposed a 10% cap on credit card interest rates, arguing that it would provide relief to consumers facing persistently high borrowing costs. The proposal has quickly drawn criticism from major financial institutions and much of the economics community, including JPMorgan Chase CEO Jamie Dimon, who has warned that such a cap could reduce credit availability and disrupt consumer lending markets. At the World Economic Forum, Dimon jokingly suggested that the administration should, “test this policy in Massachusetts and Vermont first”. Dimon went on further explaining in his view saying that, “the people crying the most won’t be the credit card companies, it’ll be the restaurants, the retailers, the travel companies, the schools, the municipalities, because people miss their water payments.” Most economists echo these concerns, pointing to historical examples of interest rate caps leading to tighter credit, higher fees, or the exclusion of higher-risk borrowers. This section examines the rationale behind the proposal, the objections raised by industry leaders and economists, and the potential implications for consumers and the financial system.

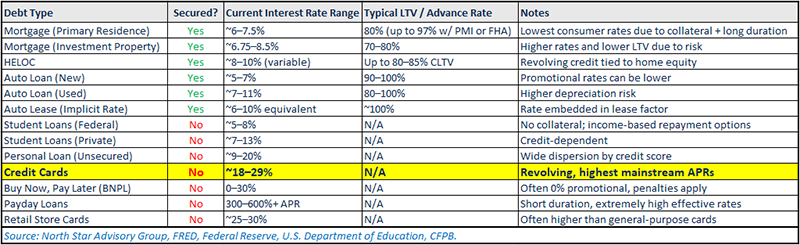

The Trump Administration is correct that interest rates on credit cards are high at anywhere from 20-30%. But are those rates justified based on the type of debt and risk associated with that debt? We’d argue that they are justified when comparing them to other forms of debt.

The wide dispersion in consumer borrowing rates is not arbitrary. It reflects fundamental differences in collateral, loan-to-value ratios, and loss severity across asset classes. Mortgages, auto loans, and home equity products are secured by tangible assets with measurable value and relatively predictable recovery rates. Low LTVs and strong collateral allow lenders to price these loans at comparatively low interest rates because expected losses are limited even in economic downturns.

Credit cards sit at the opposite end of the risk spectrum. They are unsecured, carry no loan-to-value constraint, and are typically extended with little visibility into how borrowed funds are ultimately used. In the event of default, recovery rates are minimal, meaning lenders must rely almost entirely on interest income from performing accounts to offset losses. As a result, credit card APRs embed not only expected credit losses, but also the cost of fraud, charge-offs, regulatory compliance, rewards programs, and capital requirements. High headline rates are therefore less about excess margin and more about risk absorption across a large, heterogeneous borrower base.

Lowering credit card interest rates through policy intervention would not simply compress lender profits. It would likely alter credit availability and reverberate through funding markets, particularly asset-backed securities. Credit card receivables are a major component of the ABS market, and investors price these securities based on expected yields, default rates, and excess spread. A mandated reduction in APRs would reduce excess spread, weakening the credit enhancement that protects senior bondholders. To compensate, issuers might need to tighten underwriting standards, reduce credit limits, increase fees, or pull back from extending credit to higher-risk consumers altogether.

In this way, credit card rates are not just a consumer pricing issue but a structural pillar supporting unsecured consumer credit and its securitization. Unlike mortgages or auto loans, where collateral value anchors risk, the credit card ecosystem depends on pricing flexibility to balance losses, fund capital markets issuance, and sustain broad access to revolving credit. Constraining that pricing without addressing underlying risk would shift, rather than eliminate, the economic costs of unsecured lending.

New year, new leadership

In last month’s issue of Timely Topics, we discussed the potential for a rotation of the mega-cap tech names within the U.S. and into small cap, mid cap, and international markets, given favorable risk-reward setups based on valuations and market estimates for earnings. Click HERE to read more.

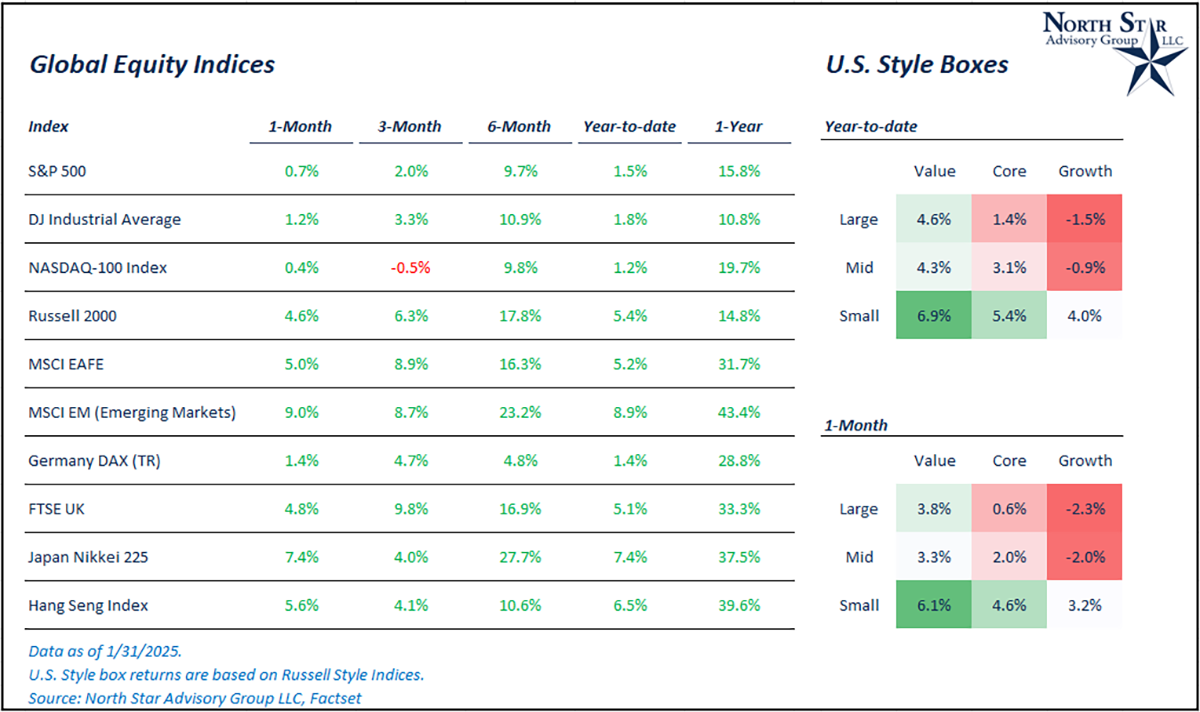

One month into 2026, we’ve began to see this rotation unfold. U.S. small cap stocks, represented by the Russell 2000 index, had positive performance in the month of January (+5.4%). Small caps outpaced U.S. large cap stocks, represented by the S&P 500, which were up by 1.5% in the month. If we dig deeper into the S&P 500 and zoom in on the “Magnificent 7” (Nvidia, Microsoft, Alphabet, Apple, Amazon, Meta, and Tesla), the average returns for these seven companies in January were just +0.4%. Additionally, we’ve seen a reversal in style leadership as value stocks are outperforming growth stocks. The Russell 1000 Value index gained 4.6% in January while the Russell 1000 Growth index fell by 1.5%

Looking abroad, emerging markets stocks are up by 5.2% and developed international markets are up 8.9%, continuing their strong performance trend from 2025.

NSAG News

Congratulations to Lisa and her Husband, Salvatore. Lisa left on maternity leave just two days before their second child, Lorenzo Luciano Saia was born on December 17th. Everyone is home and healthy, we look forward to welcoming Lisa back to the office in mid-March.

Claire Kallay joins NSAG as Executive Assistant to CEO Mark Kangas.

Claire serves as Executive Assistant to CEO Mark Kangas, where she manages a wide range of high impact responsibilities that keep the firm running smoothly and elevate the client experience. She is the first point of contact for visitors and inbound client communication, ensuring every interaction is handled with professionalism, care and quick turnaround times. Claire supports Mark with comprehensive calendar management, meeting preparation, organization of agendas and materials, and follow through on action items to maintain efficient operations. She coordinates client account servicing and money movement requests with precision and compliance, assists with office logistics and process improvements. Claire also plays a key role in advancing NSAG’s technology initiatives by implementing AI tools to streamline workflows and enhance team productivity. Her blend of organization, communication, and tech forward problem solving makes her an essential part of NSAG’s leadership support and client service infrastructure.

Claire serves as Executive Assistant to CEO Mark Kangas, where she manages a wide range of high impact responsibilities that keep the firm running smoothly and elevate the client experience. She is the first point of contact for visitors and inbound client communication, ensuring every interaction is handled with professionalism, care and quick turnaround times. Claire supports Mark with comprehensive calendar management, meeting preparation, organization of agendas and materials, and follow through on action items to maintain efficient operations. She coordinates client account servicing and money movement requests with precision and compliance, assists with office logistics and process improvements. Claire also plays a key role in advancing NSAG’s technology initiatives by implementing AI tools to streamline workflows and enhance team productivity. Her blend of organization, communication, and tech forward problem solving makes her an essential part of NSAG’s leadership support and client service infrastructure.

Claire graduated in 2025 from Bowling Green State University with a Bachelor of Science in Business Administration, with specializations in Marketing. During her time at BGSU, she served as Vice President of Member Education for Delta Gamma and was a member of the Women in Business organization.

Claire has returned to her hometown of Painesville, Ohio. In her free time, she enjoys connecting with friends and going to yoga. She also values family time and spending time with her nephews.

Where will the stock market go next?

As we reflect on January’s broad stock market performance, we find ourselves constructive on the possibility that the same trends continue through 2026. Those trends being stronger performance than small cap stocks, international stocks, and emerging markets stocks.

While the S&P 500, which represents U.S. Large Cap stock performance, has a positive return of 1.5% year-to-date, it is lagging other broad markets, mainly the three mentioned above. Small cap stocks were positive by 5.4% as investors rotated into the segment due to attractive valuation and growth dynamics. MSCI EAFE is up 5.2% on the year, which includes currency gains as the dollar continues its structural decline against the Euro and the Pound. Lastly, emerging markets stocks are up by 8.9%, led by Brazil (Venezuela Impact) and South Korea (AI infrastructure demand). All three of these markets are showing continued improvement and expected earnings growth while maintaining an attractive relative valuation versus U.S. large cap these tailwinds favor a continuation of their current trend.

We believe clients with balanced equity portfolios have a strong chance of continuing to outperform U.S.-centric portfolios in over the next 12+ months.

We are passionately devoted to our clients' families and portfolios. Contact us if you know somebody who would benefit from discovering the North Star difference, or if you just need a few minutes to talk. As a small business, our staff appreciates your continued trust and support.

Keep sending your questions for a chance to be featured in next month’s Timely Topics.

Best regards,

Mark Kangas, CFP®

CEO, Investment Advisor Representative

Brian Duffield, CFA®

Co-Portfolio Manager & Market Strategist