Each month we ask clients to spend a few minutes reading through our newsletter with the goal of raising their investor IQ. January's edition of Timely Topics focuses on a broad outlook for 2026, U.S. equity leadership, mid-term elections, and resolutions that can help to improve client’s financial life.

- 2025 Recap

- 2026 Outlook

- U.S. equity leadership

- Mid-Terms

- New Year’s resolutions

- Where will the stock market go next?

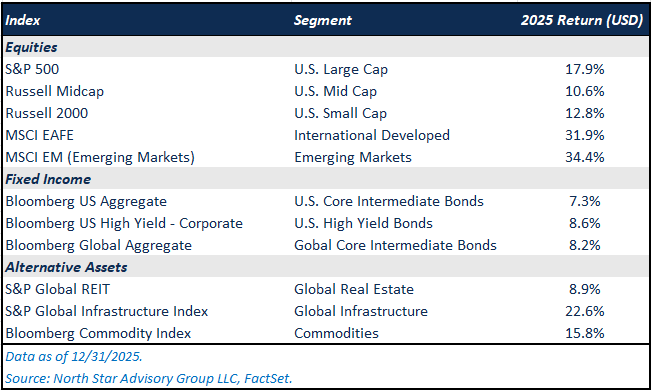

2025 Recap

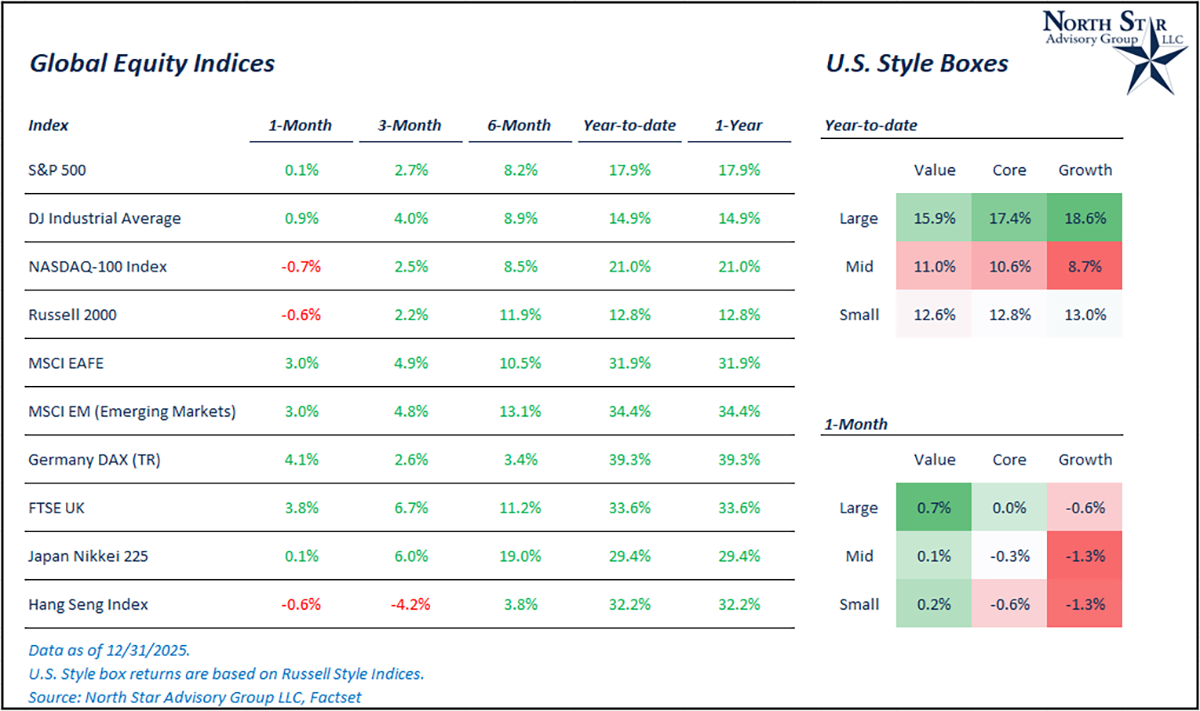

Before we dive into our outlook for 2026, it’s helpful to look back at what drove markets in 2025. U.S. equities delivered another year of solid gains, though leadership broadened meaningfully compared to prior years. Large-cap stocks rose 17.9%, while mid-caps and small-caps posted returns of 10.6% and 12.8%, respectively. This broadening performance spread reflects a healthier backdrop for market breadth, with investors showing renewed interest in areas that had lagged earlier in the cycle. AI infrastructure spending and easing inflation pressures contributed to a constructive U.S. equity environment.

International markets were the real standout. Developed international equities (MSCI EAFE) surged 31.9%, and emerging markets delivered an impressive 34.4% return, the strongest among major risk asset classes. Several tailwinds supported these regions: improving global manufacturing activity, moderating geopolitical tensions, and a more stable currency environment following the U.S. dollar’s sharp increase in 2024. Emerging markets in particular benefited from recovering domestic demand and ongoing fiscal stimulus in key Asian economies. After several years where U.S. equities dominated global performance, 2025 marked a notable shift toward more balanced global leadership.

Fixed income and alternative assets also contributed positively to diversified portfolios. Core U.S. bonds returned 7.3%, while global bonds gained 8.2% amid declining inflation and expectations of further central bank easing in 2026. High-yield bonds posted an 8.6% gain, supported by low default rates and steady credit demand. In alternatives, global infrastructure advanced 22.6%, real estate rose 8.9%, and commodities gained 15.8%. Commodities were supported by precious metals and infrastructure was supported by continued government spending. Higher mortgage rates continued to be a headwind for real estate prices despite positive performance. Altogether, 2025 proved to be a year where diversification paid off, with nearly every major asset class contributing meaningfully to returns.

2026 Outlook

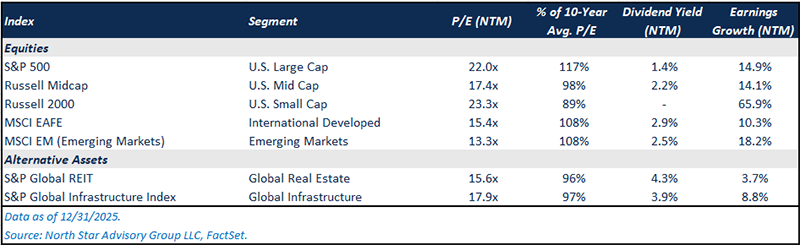

Looking ahead, forward valuations suggest a more balanced opportunity set across global equity markets as we enter 2026. On a next-twelve-month basis, U.S. large-cap equities trade at 22x earnings, or 17% higher than their ten-year average. While valuations remain elevated relative to history, they are supported by solid expected earnings growth (higher than ten-year average) and continued confidence in the durability of large-cap business models. Mid-cap stocks appear more reasonably valued, trading in line with their long-term average, while small-cap valuations have compressed meaningfully relative to history despite strong projected earnings growth.

International equities continue to offer more attractive forward valuations. Developed international markets trade at 15.4x forward earnings, only modestly above their ten-year average, while offering higher dividend yields and more balanced growth expectations as earnings aren’t as heavily tied to AI infrastructure spending. Emerging markets remain the least expensive major equity segment at 13.3x forward earnings, even as earnings growth expectations exceed those of developed markets. This combination of lower valuations and improving growth prospects underscores the diversification benefits of maintaining global equity exposure.

Alternative assets present a differentiated return profile, emphasizing income and stability. Global real estate and infrastructure both trade below their historical valuation averages and offer some of the highest dividend yields across asset classes. While forward earnings growth is more modest compared to equities, these segments can play an important role in portfolios by providing income, diversification, and potential resilience in a moderating growth environment. Overall, forward valuations highlight the importance of balancing growth, valuation, and income as markets transition into the next phase of this cycle.

U.S. equity leadership

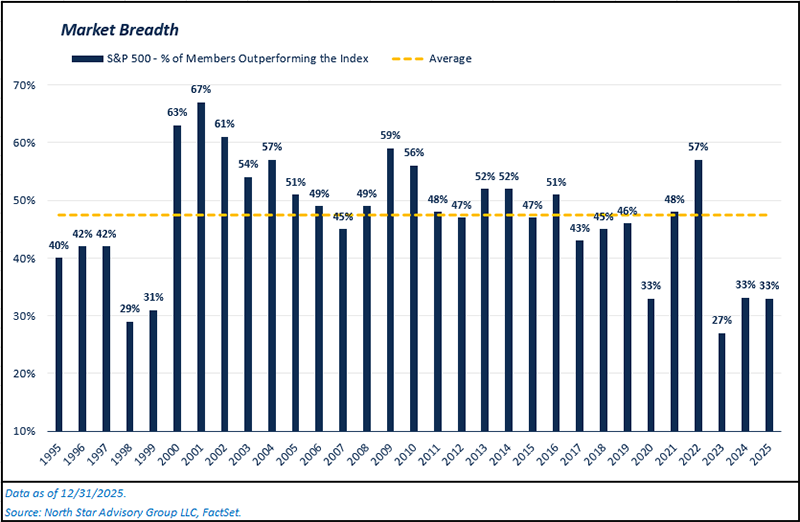

One of the more important developments beneath the surface of U.S. equity markets has been the gradual rotation in market leadership. While headline index returns have remained strong in recent years, market breadth has often been narrower than historical norms. The first chart highlights this dynamic, showing the percentage of S&P 500 constituents outperforming the index each year. Periods when breadth falls meaningfully below the long-term average have historically coincided with markets driven by a relatively small group of large-cap leaders (mega-cap technology firms in the current cycle), rather than broad participation across sectors and styles.

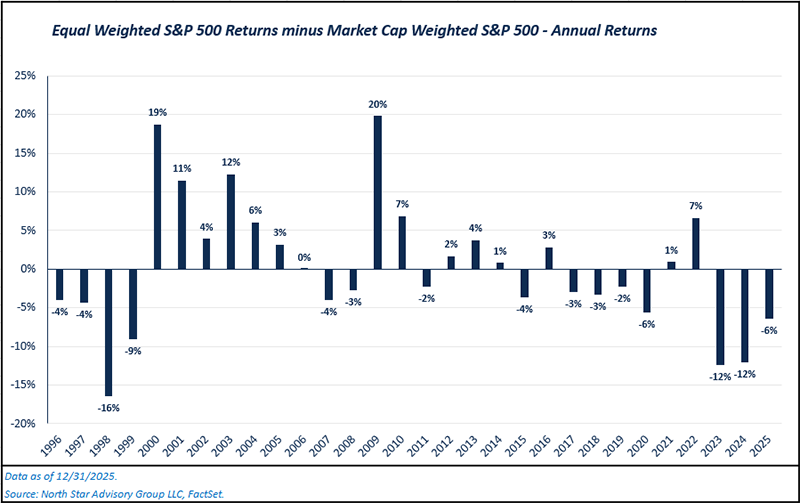

The second chart reinforces this point by comparing equal-weighted versus market-cap-weighted S&P 500 returns. When equal-weighted performance lags, it suggests that a handful of the largest companies are driving index-level results. Conversely, periods when equal-weighted returns outperform have often marked leadership rotation and improving participation from mid-sized and smaller constituents within the index. Historically, these inflection points have tended to occur as economic growth broadens, monetary policy becomes less restrictive, or valuations between leaders and laggards become more pronounced.

This potential rotation is further supported by current valuation and earnings dynamics across U.S. market capitalizations. Large-cap stocks continue to trade at a premium relative to history, reflecting their strong earnings profiles and dominant market positions. Mid-cap equities appear more reasonably valued and closer to long-term averages, while small-cap stocks currently trade below their historical average and have strong earnings growth potential over the next year. As earnings recover more broadly and financial conditions gradually ease, these valuation and growth differentials could create a more favorable backdrop for mid- and small-cap participation in 2026, reinforcing the case for a more balanced leadership environment.

Looking ahead, this history suggests that leadership rotation could remain a meaningful theme for U.S. equities. As markets move further into a late-cycle environment, returns may become less dependent on a narrow group of mega-cap stocks and more reflective of broader earnings growth across industries. While leadership rotation does not imply weaker overall market returns, it often favors diversification and balanced exposure rather than concentrated positioning. For investors, this reinforces the importance of maintaining exposure across market capitalizations and sectors as the drivers of performance evolve.

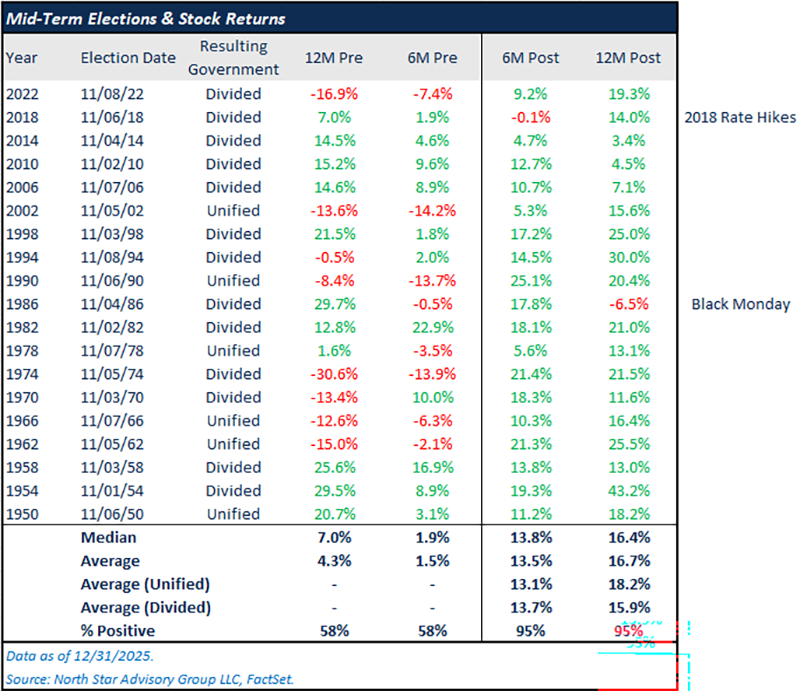

Mid-Terms

With a U.S. mid-term election approaching in 2026, investors often question how political cycles have historically influenced market returns. While elections can introduce short-term uncertainty, history suggests that markets have tended to look through the political noise and refocus on fundamentals relatively quickly. Examining equity performance around past mid-term elections provides helpful context for separating sentiment from longer-term market behavior.

Historically, stock market returns in the months leading up to mid-term elections have been mixed, reflecting elevated uncertainty and shifting expectations. Over the past 19 mid-term cycles, returns during the 12 months prior to the election have been positive just 58% of the time, with average returns of 4.3%. The six months immediately preceding the election have shown similarly modest results. This pattern highlights how policy uncertainty, campaign rhetoric, and shifting control expectations can weigh on investor confidence ahead of the vote.

Post-election outcomes, however, have been markedly stronger. In the six- and twelve-months following mid-term elections, markets have posted positive returns approximately 95% of the time, with average gains of 13.5% and 16.7%, respectively. Notably, these post-election returns have been strong regardless of whether government control was unified or divided, suggesting that clarity and reduced uncertainty often matter more than the specific political outcome. While past performance does not guarantee future results, this historical pattern reinforces the importance of maintaining a long-term perspective and avoiding reactionary decisions during politically charged periods.

It’s important to give context to the two negative performance periods following past mid-term election. The market crash of 1987, known as “Black Monday”, came in late October of 1987. The single day decline of -22% caused the 12-month post return after the 1986 mid-term elections to be negative. In Q4 2018, the Federal Reserve began raising interest rates amid concerns of rising inflation. This took place shortly after the 2018 mid-term elections, causing a slightly negative return in the six months that followed.

New Year’s Resolutions: Small Habits, Big Changes

Working out and maintaining a routine/Contributing consistently to retirement accounts

Just as occasional workouts rarely lead to lasting health improvements, sporadic investing often falls short of long-term goals. Making regular contributions to a 401(k), particularly enough to receive an employer match when available, can be one of the most effective ways to build financial strength over time. Consistency is often more important than attempting to time markets or make large, one-time changes.

Call to action: Set up automatic retirement contributions and let consistency do the heavy lifting.

Healthy eating and balanced nutrition/Thoughtful budgeting and cash flow awareness

Successful diets tend to focus on balance rather than restriction, and the same principle applies to personal finances. Accurately understanding income, expenses, and savings help individuals make informed decisions while maintaining flexibility. A realistic budget can support financial goals without requiring drastic or unsustainable changes.

Call to action: Set up Monarch access. Reach out to the NSAG team if you haven’t yet started using this budgeting tool.

Building strength gradually/Long-term tax-advantaged savings

Physical strength develops through steady effort, and meaningful wealth accumulation follows a similar path. Making regular contributions to tax-advantaged accounts (Roth IRAs, 401ks, 403bs, etc.) when appropriate, can provide long-term benefits through compounding and tax efficiency. The impact may feel modest in the short term but can be meaningful over time.

Call to action: Max out Roth IRAs in 2026, consult with NSAG about eligibility.

Staying disciplined when progress feels slow/Avoiding emotional financial decisions

Many fitness plans fail not because they are ineffective, but because they are abandoned during periods of frustration. Financial plans can face similar challenges during market volatility. Maintaining discipline and staying focused on long-term objectives can help investors avoid decisions driven by short-term market movements.

Call to action: Avoid short-term market noise and attention-grabbing news headlines.

Rest and recovery/Periodic financial check-ins and rebalancing

Rest days play an important role in physical improvement, just as regular financial reviews help maintain alignment with long-term goals. Periodic check-ins, including reviewing asset allocation and rebalancing when appropriate, can help ensure a portfolio continues to reflect changing market conditions and personal circumstances.

Call to action: Schedule regular financial check-ins to review progress and make thoughtful adjustments.

Where will the stock market go next?

Looking ahead, we believe the market environment in 2026 may continue to favor globally diversified portfolios over U.S.-only allocations, building on the relative performance seen in 2025. With a broader set of economic drivers and more balanced valuation profiles, global exposure may offer a more resilient return profile, particularly if leadership continues to rotate across regions and market segments. Diversification across geographies can also help reduce reliance on any single growth theme and may provide added stability during periods of market adjustment.

Within U.S. markets, small- and mid-cap companies may be positioned to benefit as the practical efficiencies of artificial intelligence are increasingly realized across a wider range of businesses. As these tools move beyond infrastructure investment and into everyday operations, productivity gains could support earnings growth outside of the largest companies. Combined with more reasonable valuations in many cases, this dynamic could contribute to broader participation in equity market returns over time.From a fixed income perspective, short-duration bonds continue to appear attractive given their current risk and return characteristics. While interest rate expectations and the shape of the yield curve remain important considerations, shorter-maturity bonds may offer a more balanced approach to income generation and interest rate sensitivity in a changing policy environment. As always, positioning remains subject to evolving market conditions and should be evaluated within the context of broader portfolio objectives.

We are passionately devoted to our clients' families and portfolios. Contact us if you know somebody who would benefit from discovering the North Star difference, or if you just need a few minutes to talk. As a small business, our staff appreciates your continued trust and support.

Keep sending your questions for a chance to be featured in next month’s Timely Topics.

Best regards,

Mark Kangas, CFP®

CEO, Investment Advisor Representative

Brian Duffield, CFA®

Co-Portfolio Manager & Market Strategist