Each month we ask clients to spend a few minutes reading through our newsletter with the goal of raising their investor IQ. We are focusing February’s Timely Topics on developments within the AI theme, tariffs, and two fun topics, one including the College Football National Championship game.

- College football national championship

- Tariffs or casino chips

- Project Stargate

- DeepSeek or DeepFake?

- Love/hate relationship

- Where will the stock market go next

College football national championship

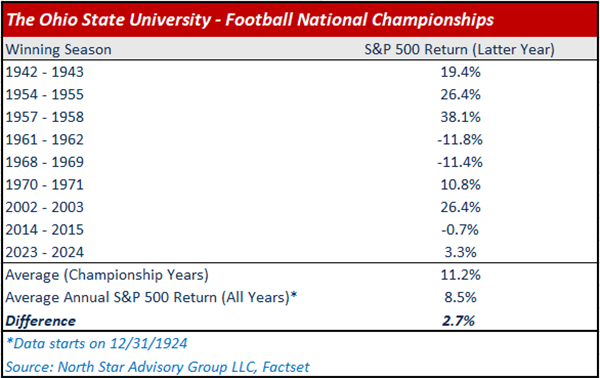

At North Star, we know that correlation does not equal causation. However, with the Buckeyes securing their ninth football national championship, we thought it would be interesting to review how the U.S. market performed after each winning season.

The table below summarizes the calendar year returns for the year following each of the Buckeyes' national championship winning seasons. Six out of nine years had positive returns for the S&P 500 after the Buckeyes won a college football national championship (including 2025's performance through January). On average, the annual return was 11.2%, which is approximately 2.8% higher than the average for all years, beginning with the 1925 calendar year for the S&P 500. This data may be of interest to those who consider coincidences as a key driver in market performance.

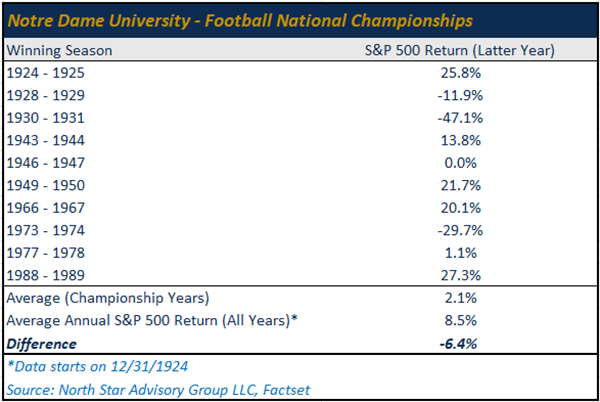

Notre Dame has won 10 national championships, but their timing hasn't always been fortunate. Six of these wins coincided with positive returns for the S&P 500, while four did not, occurring during tough economic periods like the Great Depression and the Arab oil embargo of 1974. These years brought Notre Dame’s average annual return down to 2.1%, below the historical average by 6.4%. Thankfully, the Buckeyes delivered in their 2025 championship game.

Tariffs or casino chips

During the Trump Administration's immigration crackdown, some countries resisted compliance. Colombia, for example, initially refused to accept deported immigrants from the U.S. Almost immediately, the Trump Administration announced a 25% tariff on Colombian exports to the U.S. along with a slew of various sanctions citing national security as the driver. The 25% tariff would further increase to 50% if Colombia didn’t comply. Within a day, the Colombian government accepted all terms relating to U.S. immigration policy and allowed flights to resume.

Without getting into the debate on whether this is the correct approach or not, it further validates our view from December 2024 that tariffs will mostly be used as a “bargaining chip” for the Trump Administration to accelerate their geopolitical goals. A quote from December’s issue, “In our opinion, NSAG believes tariffs will mainly be used as a “bargaining chip” by the Trump administration to tackle geopolitical issues that indirectly involve China. It’s highly likely that the U.S. will use tariffs as a negotiating tactic to bring down China’s oil imports from both Iran and Russia. If successful, this would put additional pressure on both Iran and Russia to come to the negotiating table in both of their respective conflicts.” While we cited specific concerns related to China, the underlying theme remains.

What would a potential trade war with Colombia look like? For U.S. consumers, the impact would’ve been limited. Coffee and oil/petroleum products are Colombia’s primary exports as a country. The U.S. imports ~$2.5B worth of coffee from Colombia annually, representing ~33% of the United States’ $7.5B annual imports of coffee. Additionally, the U.S. imports $2.2B worth of oil/petroleum products on an annual basis from Colombia. This represents a slim 1.46% of the United States’ $150B annual imports of oil/petroleum products. We don’t expect these tariff-driven negotiating tactics to stop anytime soon, whether they’re in regard to solving current geopolitical goals or issues that pop up over the next four years.

On January 27, President Trump also announced plans for sweeping tariffs on semiconductors, steel, and pharmaceuticals. These comments set the stage for his next tariff-driven match which China. Taiwan is the global leader in semiconductor exports via Taiwan Semiconductor, followed by South Korea’s Samsung Electronics and SK Hynix. Additionally, China is the global leader in steel exports. These negotiations likely won’t be debated and resolved as quickly as the Colombian dispute, and investors should expect increased volatility surrounding these developments.

Hours before publishing this month’s Timely Topics, the Trump Administration paused tariffs on Mexico for one month after the Mexican government agreed to send 10,000 troops to the border. We now have Colombia and Mexico as proven examples of the “bargaining chip” theory. We also believe that Canada will come to the negotiating table soon. Canada’s annual exports to the U.S., ~$500B in 2023, make up ~60% of their total exports. Assume a 25% tariff caused a decrease in demand of 20% (~100B less exports from Canada), Canada’s GDP would take a hit of roughly -4.6%, plunging Canada into recession.

Project Stargate

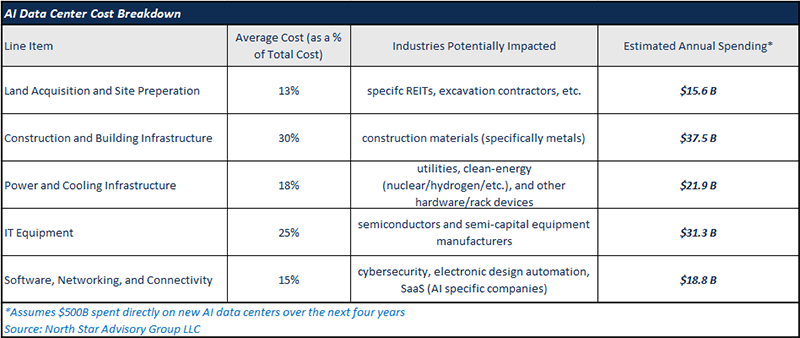

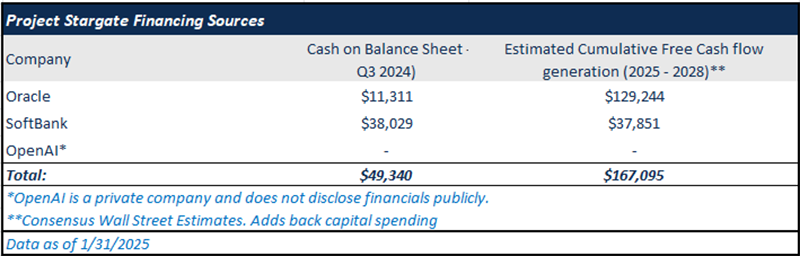

On Donald Trump’s second day in office, he announced Project Stargate, a private sector financed spending plan to construct new data centers within the U.S. The target spending amount for this project is ~$500B over four years or $125B per year if we assume linearity. Before we get into the likelihood of $500B being deployed over the next four years, let’s assume that it will happen, and track specific areas in which these dollars would hypothetically be spent.

While this type of spending will provide a boost to the top-line growth for many businesses in the data center supply chain, it’s hard to imagine that Project Stargate delivers on their goal of $500B spent. As of January, this project is being backed by SoftBank, Oracle, and OpenAI and is fully financed through the private sector (no government spending). If Oracle and SoftBank were to invest every last dollar of cash on their balance sheet, including their next four years of cumulative free cash flow generation (estimated) into Project Stargate, there would still be a funding gap of ~$284B! Although OpenAI is a private company that does not disclose financials publicly, their latest valuation was ~$157B, meaning they are nowhere near the level cash flow generation needed to fill this funding gap. It is likely that other technology companies will be stapled onto this project and the dollars they had already planned towards spending will be viewed as within the scope of the project. There is also a significant threat to overall AI-driven capital spending plans sparked by developments within a Chinese AI company, DeepSeek. (See the next section for an in-depth analysis).

DeepSeek or DeepFake?

While we were in the middle of finishing our section on Project Stargate, January 27 happened. The day the U.S. Technology sector was rocked by a Chinese AI startup, DeepSeek, a competitor to large language models (LLMs) developed in the U.S. by companies like OpenAI (ChatGPT) and Meta (LLaMA), etc. DeepSeek gained traction over the preceding weekend, rocketing to #1 on the Apple App Store.

DeepSeek claimed to have trained its LLM with a cost of $5.6 million while benchmarking well (or even better) than the some of the newest LLMs developed in the U.S. by the aforementioned companies. Two days later, Alibaba, the Chinese e-commerce giant, released their LLM, the “Qwen” model, claiming it also outperformed DeepSeek’s V-3, OpenAI’s GPT-4o, etc. The U.S. Technology sector did not take the DeepSeek development well and on January 27, the Nasdaq 100 Index fell by more than 3%. Although, if you dig one level deeper, you’ll notice that the bulk of the pain came to the “picks and shovels” names within the Nasdaq 100 such as semiconductor designers and semi-cap equipment manufacturers. On January 27, the PHLX Semiconductor Index fell by ~9%, while the S&P Software & Services Select Index fell by only 1.3%. The next day, semiconductors modestly recovered (+1%) while software and services rallied harder (+2.8%). Clearly, based on this price action, the market’s concern was centered around DeepSeek’s $5.6 million budget claim, not the fact that they created a comparable model. This claim forced the market to question the hundreds of billions of dollars that have been invested into high-performance GPUs and data centers over the past two years and spooked the market’s expectations of continued investment going forward.

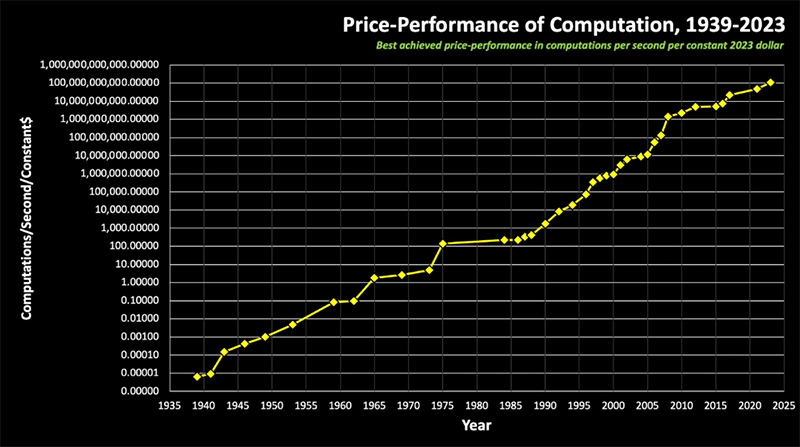

Before we get into reasons that the $5.6 million dollar claim should be questioned, let’s operate under the assumption that the claims are true. The “shoot first and ask questions later” reaction by the market is likely overdone, but a compute efficiency innovation does change the way that we should be thinking about the “AI Trade” moving forward. First and foremost, machine learning innovations are not new to our world. The cost for compute power has been declining for decades as innovations within the technology sector take place and is the reason for technology being a “deflationary force.” In the chart below, we display the “Price-Performance of Computation” over time, reinforcing the consistent innovations and efficiency gains realized over time. To help understand this chart, the vertical axis displays the number of computations achieved for $1 spent and increases exponentially.

Source: https://www.bvp.com/atlas/ai-escape-velocity-a-conversation-with-ray-kurzweil

Long-term benefits and productivity gains from AI were always going to come from what we’ll call “AI-products.” An “AI-Product” could be a self-driving car, cybersecurity software, warehouse robotics, etc. The fuel behind the ability to make these products is the LLMs that are being developed. Currently, the “AI-Products” that these LLMs are primarily fueling are the chat bots we use daily (Chat GPT, Google Gemini, etc.) In our view, if we have had another breakthrough in machine learning efficiency, demand for processing power and data centers could increase as new competitors enter the LLM market and current players find ways to improve their own versions. This would increase the “AI product” development rate and as these products are adopted across enterprises and the public, there is additional processing power demand to keep them running quickly and efficiently. Effectively, this could “spread the wealth” of the AI theme more broadly in the markets, and less concentrated portfolios should benefit. In 2023 and 2024, the overwhelming demand for GPUs was driven by the need for training LLMs, and this may shift towards inferencing demand (“inferencing” GPUs are required for applying these models in real world applications). Think about the market’s reaction to this potential breakthrough as software companies weathered the storm and actually rallied broadly over the two-day period. This is a realization that they may be able to access processing power more efficiently as they develop and deploy their AI products.

Lastly, we mentioned in an earlier paragraph that DeepSeek’s claim of $5.6 million may not be totally truthful. Over the past four years, the Biden Administration continuously tightened export restrictions of high-powered chips from the U.S. to China in an effort to curb their AI developments. So, if Chinese companies have been able to access the newest GPU design from companies like Nvidia through black markets/third-party country loopholes (which would’ve been used to train the DeepSeek model), they definitely would not admit to it. They are also unlikely to be able to scale Nvidia device acquisition. Some industry leaders such as Elon Musk and Alex Wang have inferred that DeepSeek had ~50k H100 GPUs (Nvidia’s latest GPU in mass production). Regardless, we believe two things can be true at once. China may not be truthful in their disclosures, but a breakthrough in processing power efficiency is inevitable if not already occurring.

Love/hate relationship

In one of Trumps initial press conferences post-inauguration, he demanded that interest rate levels come down. When a reporter asked him, “Do you think the Fed will listen?” he simply replied after a long pause, “Yeah.” This will likely set the stage for a once again strained relationship between Trump and Federal Reserve (Fed) Chairman Jerome Powell. This saga continues after their public disagreements during Trump’s first term. As we know, the Fed is tasked with being independent, meaning that their actions are not subject to federal approval. Regardless of their independence, there is no doubt that Trump will continue to publicly pressure the Federal Reserve in an attempt to get his way. In reality, the Fed has been cutting interest rates since September, but as we’ve discussed in the past, longer-term yields (i.e. 10-Year Yield) are driven by economic growth and inflation more than it is by Fed decisions (cuts or hikes).

For fun, we prompted ChatGPT to write a short story about the love/hate relationship between Donald Trump and Jerome Powell during Trump’s first term… This section has not been edited for grammar, to preserve AI’s story.:

Once upon a time in the whirlwind world of tweets, interest rates, and the economics, Donald Trump and Jerome Powell found themselves in an unexpected, often strained, but occasionally warm relationship.

It all started in early 2018 when Trump sent out a tweet praising Powell: “Just had a great meeting with Jerome Powell, the new Fed Chairman. He’s doing a fantastic job!” Trump tweeted, probably imagining Powell as a nice, pliable asset. Powell, cool and collected as ever, didn’t exactly return the fire with flamboyant compliments. In fact, he barely responded at all. But soon, things started to get a little bumpy.

Throughout 2018, Trump was frustrated with Powell’s interest rate hikes. He didn’t hold back, tweeting: “The Fed is going loco; they are making a mistake!” It wasn’t just the tweets. Trump would regularly express his displeasure with Powell’s “hawkish” stance, once calling him “a dangerous man,” and telling reporters, “I don’t like that Jerome Powell is raising rates, but that’s just me. He’s been doing it too fast.”

Powell, not known for getting ruffled, stuck to his guns. “We’re focused on getting inflation under control,” he said at a press conference, while trying his best to ignore Trump’s public admonishments. He added, "The economy is in a good place, and we are taking appropriate steps."

But Trump, being Trump, wouldn’t let it slide. In 2019, he tweeted again: “I think the Fed should be cutting rates, but Jerome Powell just doesn’t get it!”

Powell, for his part, kept his poker face on. Even when things got more personal. Trump tweeted: “Jerome Powell and the Federal Reserve have no clue; they don’t know what they’re doing! How could they mess up something so easy?”

Powell’s retort? A quiet, measured response, not to Trump directly, but in the form of policy. Interest rates were eventually cut, just as Trump wanted. He said in a statement, “We’re being data-driven, and that’s what we have to do in these times.” And yet, the saga continued. Trump would often tweet about Powell’s actions, one time writing: “We need to make America’s economy great again, and Jerome Powell needs to stop being so stubborn!”

Despite their ups and downs, there were moments where the two seemed to connect. Trump tweeted in 2020: “Jerome Powell, while I don’t always agree with you, I think you’re doing the best job possible in these difficult times. Keep it up!” Powell, ever the professional, didn’t tweet back—he just kept adjusting interest rates, making economic moves, and keeping his eye on the bigger picture.

So, there they were—one, the self-proclaimed dealmaker, the other, the unflappable economist. Each with their own agenda. Yet somehow, despite the occasional public spat, they made it work… in that chaotic, economic rollercoaster kind of way. After all, as Trump might say: “It’s just the art of the deal.”

Where will the stock market go next?

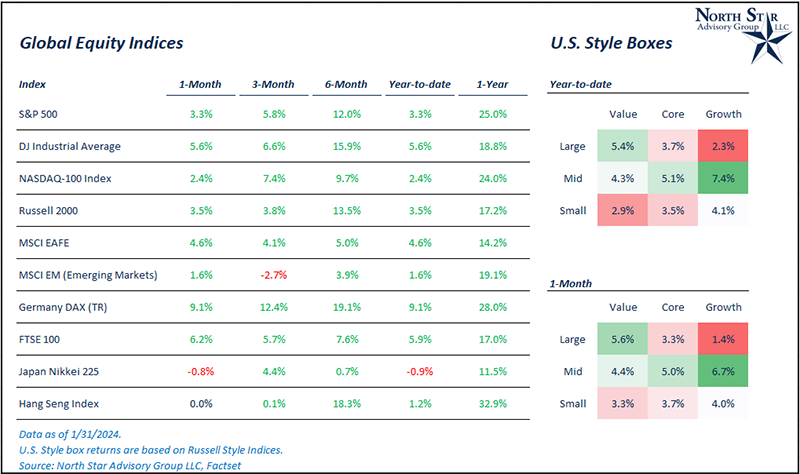

January was full of volatility as markets focused on multiple moving pieces, including the Federal Open Market Committee (FOMC) meeting, DeepSeek (and other Chinese AI developments), and tariff implications. For the month of January, the S&P 500 moved up by 3.3%, while U.S. small cap moved up 3.5%, and international developed markets rebounded by 4.6%. U.S. value stocks led relative to growth and European stocks led the rebound in international markets. The U.S. dollar fell during the month, helping to boost returns within international markets as interest rates decreased. This move is an unwind of the trend we saw from election day through the end of the 2024 calendar year. For those who remember, in Trump’s first term, international stocks fell from election day through inauguration day (January 2017) and proceeded to outperform U.S. markets over the remainder of 2017.

On January 29, the Federal Reserve left their policy rate unchanged at a range of 4.25% - 4.50%, a move that was widely expected by the market. During the meeting, Jerome Powell noted that they believe this range is meaningfully above the current neutral rate (current rates are still restrictive in their view). Concerns over inflation caused by tariffs are likely driving the Federal Reserve to maintain this stance, although, we believe tariffs will not cause massive inflation shocks, given that Trump appears to be using them as a negotiating tactic (not as a promise but as a threat). We think this was the correct move by the Federal Reserve. Historically, the Fed tends to telegraph their moves, and a hold was what was telegraphed since cutting rates by 0.25% in December. This leaves room for further cuts in 2025 if our thesis on tariffs proves to be correct and could lead to more upside for stocks, particularly smaller companies who rely more heavily on variable rate financing.

Within the technology sector, hardware companies such as semiconductor designers and manufacturers will continue to see some short-term volatility as hyperscalers provide further clarity on their spending plans during the earnings season. From what we’ve gathered, we’re not yet seeing a slowdown in data center investments, although the composition of those data centers is likely to shift over time and there will be some choppiness in the spend over the years (see section on DeepSeek).

Overall, we continue to have a positive view of global equity markets and encourage diversification in client’s stock portfolios during this time. With that positive view, we also expect higher volatility in 2025 than experienced in 2024. Over the past 40 years, the S&P 500 has had an average peak-to-valley drawdown of ~10% each year. In 2024, this threshold was not breached despite political volatility and the unwinding of the yen carry trade in August.

We are passionately devoted to our clients' families and portfolios. Contact us if you know somebody who would benefit from discovering the North Star difference, or if you just need a few minutes to talk. As a small business, our staff appreciates your continued trust and support.

Please continue to send in your questions and see if yours get featured in next month’s Timely Topics.

Best regards,

Mark Kangas, CFP®

CEO, Investment Advisor Representative