Each month we ask clients to spend a few minutes reading through our newsletter with the goal of raising their investor IQ. We are focusing December’s Timely Topics on the proposed Trump administration and what it may mean for the economy and client’s portfolios.

- A Unified Government Structure

- Tariffs

- Regulations and D.O.G.E

- Taxes

- Immigration and Deportation

- Where will the stock market go next

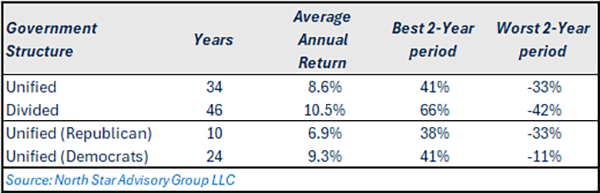

A Unified Government Structure

Some clients have expressed concerns about the stability of the economy and the stock market following Trump’s victory. It is worth noting that similar apprehensions were received from clients after Biden's victory in 2020. While the past three elections have been highly polarizing regarding policy and social views, much of this polarization can be attributed to the influence of social media and the transition to a digital economy. To provide a balanced perspective, NSAG analyzed the returns of the S&P 500 under different government structures, particularly as the U.S. will have a unified Republican government. Since World War II, there have been 17 instances of a unified government—5 under Republicans and 12 under Democrats—spanning a total of 34 years.

Historically, a divided government has been associated with stronger stock markets, as markets tend to prefer stability, which is less likely under unified control. Republican unified governments averaged 7% annual returns, while Democrat’s unified governments averaged 9.3% since WWII. Both parties had positive market returns on average during these periods. More recently, Biden's unified government (2021-2022) yielded a 2% S&P 500 return, while Trump's (2017-2018) achieved 12%. Under divided governments, Trump saw a 50% rise (2019-2020), and Biden experienced a 53% rise (2023-2024), further emphasizing the benefits of a divided government for stock markets.

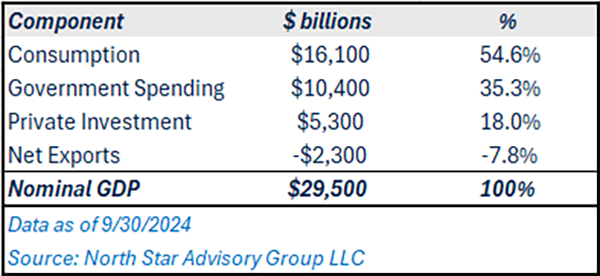

Turning to Trump specific policies, NSAG believes his agenda may have mixed effects on short-term economic growth and potential long-term benefits. These policies could also increase inflation in the short term. The following sections will examine each major policy's impact on GDP, assuming their implementation. NSAG breaks down each policy within the context of the following GDP formula.

Gross domestic product (GDP) = Consumption + Government Spending + Investment + Net Exports (Exports - Imports).

As of 9/30/2024, U.S. Nominal GDP was $29.5 trillion, and the components are broken out in the table below.

Tariffs

GDP = Consumption (C) + Government Spending (G) + Investment (I) + Net Exports (Exports - Imports).

Tariffs are a type of tax that imposes additional costs on imported goods. Protecting domestic industries and reducing a nation’s trade deficit are the two primary goals of tariff implementation. An added tax on imported goods comes with both pros and cons.

Pros:

The scope and details of potential tariffs from the Trump administration are still unknown. So, let’s operate under the assumption that a sweeping 10% Tariff is placed on all U.S. trading partners. Annually, the U.S. imports ~$3 trillion worth of products from foreign nations. Holding all else equal, this tariff strategy would result in a ~1% bump in inflation ($300 billion / $29.5 trillion). This additional $300b in costs for consumers is additional revenue for the federal government. Although, these additional costs could be offset partially by further personal and corporate tax rate cuts. Lower wage earners will feel the impact of tariffs the most considering they generally live paycheck-to-paycheck. The tariffs to this group could act as a de facto income tax (generating revenue for the federal government) from a group that normally pays little to no federal income tax traditionally.

In the long run, there is potential for GDP gains from falling import volumes and increased private investment in domestic industries as demand for imports decreases. This impact would not be felt as immediately as the inflationary pressures caused by sweeping tariffs.

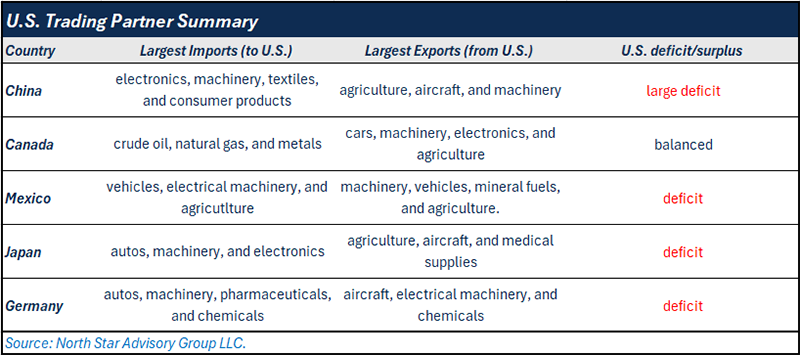

Taking this conversation one level deeper, our largest five trading partners are China, Canada, Mexico, Japan, and Germany (see the table below which summarizes each of these country’s trade relations with the U.S.).

Foreign companies within impacted industries listed above may have to lower their selling prices in order to reduce some of the tariff’s impact and maintain competitiveness as an importer versus domestic alternatives. This will likely reduce profit margins for these foreign companies. For domestic companies in these industries, they’ll likely experience pricing and volume gains as well as increased investment into their respective industries.

From 11/5/2024 through 11/22/2024, the MSCI China Index is down 8.6% and the MSCI Mexico Index is down 1.4%. Canada and Japan have had positive returns since election night. This price movement tells us that the market believes tariffs will be most targeted at China and possibly Mexico, which comes as no surprise to NSAG.

Common imported items from most of our top trading partners are machinery, electronics, and autos. From 11/5/2024 through 11/22/2024, the FactSet US Industrial Machinery Index rallied 3.3% and the FactSet US Electrical Component Index rallied 5.6%. Additionally, the FactSet US Motor Vehicle Index was sharply up by 35%, while the World ex US motor vehicle index was down 4.3% over that same time frame. A majority of the US Motor Vehicle performance came from Tesla as they are the largest constituent of the index.

In our opinion, NSAG believes tariffs will mainly be used as a “bargaining chip” by the Trump administration to tackle geopolitical issues that indirectly involve China. Its highly likely that the U.S. will use tariffs as a negotiating tactic to bring down China’s oil imports from both Iran and Russia. If successful, this would put additional pressure on both Iran and Russia to come to the negotiating table in both of their respective conflicts. OPEC currently has spare production capacity of ~5 million barrels per day, which could more than cover China’s shortfall if they completely stopped purchasing from Iran and Russia. Although, this adds complexity to the negotiations as OPEC nations would have to agree on filling the supply shortage. Over the long run, Trump would prefer that the U.S. backfill China’s oil supply, not OPEC. Although, the U.S. does not yet have this level of spare production capacity.

Regulations/D.O.G.E

GDP = Consumption (C) + Government Spending (G) + Investment (I) + Net Exports (Exports - Imports).

On the campaign trail, Trump discussed in his words “slashing regulations” and “cutting red tape” numerous times. A few industries and sub industries that have been discussed in the context of regulation cuts include;

Again, operating under the assumption that most regulatory cuts are made, you will likely see a sharp increase in private investment.

The newly founded Department of Government Efficiency, led by Elon Musk and Vivek Ramaswamy, will not only be a tool used to recommended cuts for “inefficient government spending,” but will also walk hand-in-hand with potential regulation cuts. The most important aspect of D.O.G.E is that it will not be an actual government department. So, Elon, Vivek, and their team will essentially act as an outsourced consulting firm for the Trump administration. Elon and Vivek have already claimed that they have identified ~$2 trillion in budget cuts (more than the $1.83 trillion Federal Deficit for FY 2024), but any proposed cuts will have to be approved by congress and would likely be met with legal retaliation from labor unions. With that said, NSAG believes that there is a low probability that $2 trillion worth of cuts will be implemented. If they were to accomplish this goal, there would be a 6.7% hit to GDP ($2 trillion / $29.5 trillion) coming from government spending, holding all else equal. While this would be a large hit to GDP, it likely wouldn’t be felt all at once. A large chunk of these dollars would likely be re-directed towards paying down the national debt, which would lower the nation’s default risk and therefore lower interest rates.

Taxes

GDP = Consumption (C) + Government Spending (G) + Investment (I) + Net Exports (Exports - Imports).

In 2017, the Tax Cuts and Jobs Act (TCJA) was passed, lowering the marginal tax rates for individuals and lowering the corporate tax rate to a flat rate of 21% along with adjustments to many other provisions (SALT Cap, Estate Taxes, etc.). These tax reforms are set to expire in 2025, and now that Republicans control the both the House and Senate, Trump will have a much easier, but not automatic, path to fully extending lower tax rates currently set to increase in 2026.

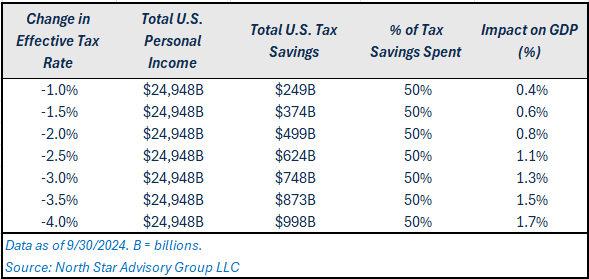

Trump made a variety of other promises relating to tax cuts on the campaign trail including no tax on tips, social security, and overtime. But for simplicity, let’s assume further cuts to personal income tax rates and only half of those additional tax benefits are spent into the economy. As of 9/30/2024, the average effective federal tax rate in the U.S. is 12.4%. In the table below, NSAG analyzed a few scenarios for GDP impact based on the potential decrease in federal income tax rates. While we are conservatively assuming that 50% of tax savings are consumed, that number would likely be higher as lower income households would spend closer to 100% of their tax savings.

Immigration and Deportation

GDP = Consumption (C) + Government Spending (G) + Investment (I) + Net Exports (Exports - Imports).

There are varying estimates of how many illegal immigrants currently reside in the U.S. High estimates typically come from right leaning sources while low estimates typically come from left leaning sources. For this discussion, NSAG uses the 11 million estimate made by the department of homeland security and analyzes this topic solely in the context of potential economic impact.

Overall, the majority of illegal immigrants work within industries that are labor-intensive, such as agriculture, construction, and hospitality. Companies are also typically able to pay these workers less than their legal resident counterparts. There are currently ~7.4M job openings within the U.S. as of 9/30/2024, and the ratio of Job openings to unemployed persons is ~1.1 (higher than the 22-year average of 0.75), indicating a tight labor market. So, deporting all 11 million illegal immigrants (of which ~8 million are working age), would add significant upward pressure on wages and in turn, inflation as companies attempt to protect their profit margins.

Turning to the GDP context, consumption would fall as a result of these deportations. Assuming all 8 million working age illegal immigrants make an average hourly salary of $15 and work 2,080 hours per year, there would be a hit to consumption of ~$250 billion (8 million x $15 x 2,080), assuming no taxes or savings. This would be a 0.8% ($250 billion / $29.5 trillion) decrease in GDP via consumption. This would also lower long-term growth expectations to some extent as the labor supply of a country is a major component for future growth.

Given the tight labor market, these jobs would partially need to be backfilled through continued technological advancement in robotics and automation, likely encouraging more private investment. In the end, you may find that Trump approaches deportation in a smaller and more targeted way.

Where will the stock market go next?

Trump's various policies simultaneously affect both GDP and inflation, often in multiple directions. They focus primarily on two key areas: government spending (~35% of GDP) and private investment (~18%). These policies aim to reduce reliance on government spending and boost private investment through less regulation, lower taxes, and technological innovation. NSAG believes private sector spending is more efficient and profit-focused, unlike government spending which does not come with an underlying fiduciary duty to shareholders.

Many policies could increase Consumer Prices (CPI), leading to higher interest rates from the Federal Reserve during the remainder of Jerome Powell's term. However, NSAG believes these inflationary effects will be temporary, as they are not caused by long-term fiscal deficits or extensive money printing. Policies such as mass deportation and trade tariffs can be seen as throwing a wrench into the current economy and the U.S. will rely on innovation and private investment to alleviate the pressures of theses “wrenches” and set the U.S. economy on a new path that favors the private sector versus the public sector.

NSAG believes that in aggregate, the U.S. economy still has strong underlying growth tailwinds, but the possibility for volatility in the near term is real, especially during Trump’s first two years as policies take form. This has been the case historically when experiencing a unified government structure. Although, returns are still likely to be positive.

From 11/5/2024 to 11/22/2024, the top three performing U.S. sectors have been Financials (+14.7%), Energy (+14.8%), and Information Technology (+17.5%). Consistent with the areas of probably regulation cuts discussed earlier in the article. On the flip side, healthcare stocks are down 2%. Healthcare is notably down due to increased regulatory pressures expected on the pharmaceutical and biotech industries after Trump’s nomination of Robert F. Kennedy Jr. as the head of the Department of Health and Human Services.

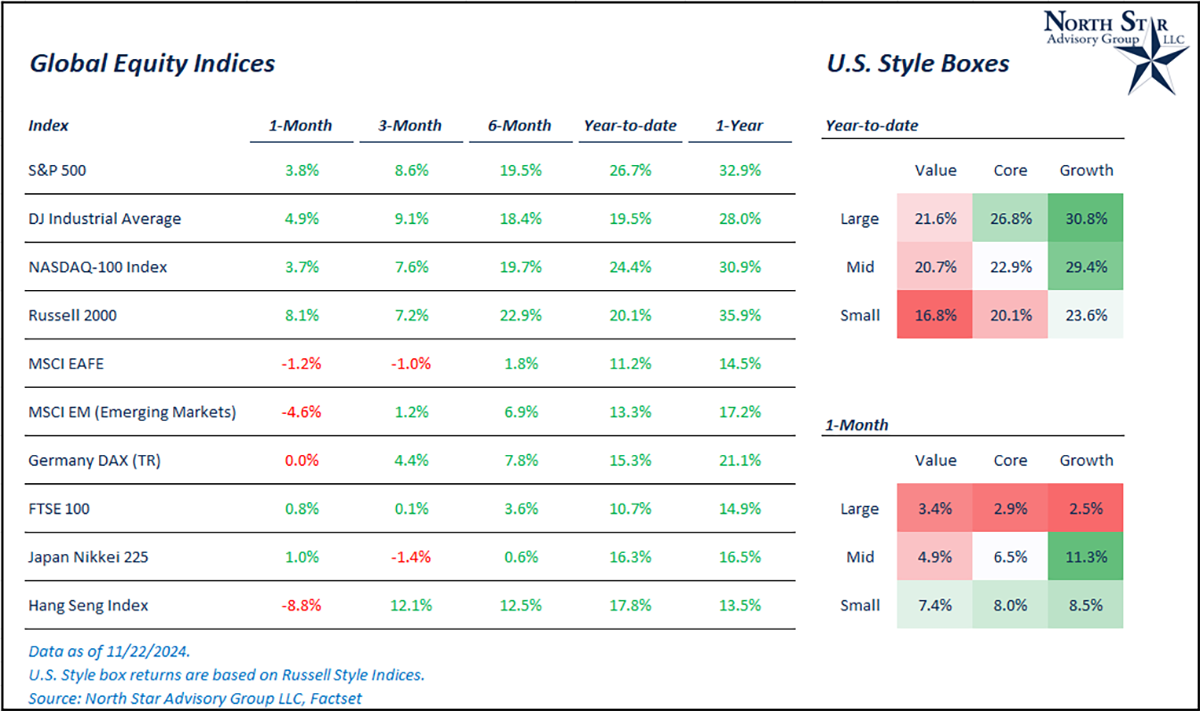

More broadly, the S&P 500 (U.S. Large Cap) is up 3.8%, the Russell 2000 (U.S. small cap) is up 6.5%, the MSCI EAFE (international developed) is up 0.15%, and the MSCI EM (emerging markets) is down 3.5% from 11/5/2024 to 11/22/2024.

We are passionately devoted to our clients' families and portfolios. Contact us if you know somebody who would benefit from discovering the North Star difference, or if you just need a few minutes to talk. As a small business, our staff appreciates your continued trust and support.

Please continue to send in your questions and see if yours get featured in next month’s Timely Topics.

Best regards,

Mark Kangas, CFP®

CEO, Investment Advisor Representative