Each month we ask clients to spend a few minutes reading through our newsletter with the goal of raising their investor IQ. May, recognized as college savings month, serves as a timely reminder for families to explore ways to save for education and maximize the benefits of 529 college savings plans to “SECURE” their children’s educational and financial future.

We continue to encourage clients to read May 2023’s Timely Topics, which covers a few additional topics not covered this month and includes the offer for a FREE activity book for children ages 8-12.

- College tuition inflation

- Average cost of schools

- Accounts to save for college

- Rollover a 529 into a Roth IRA

- NSAG new hires

- Where will the stock market go next?

College tuition inflation

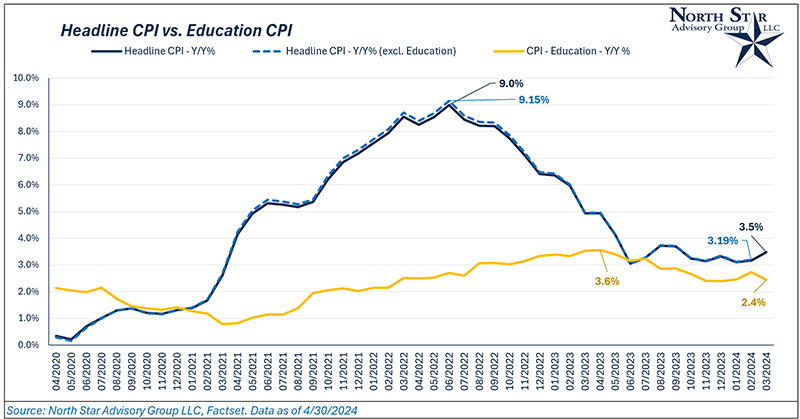

While inflation continues to be a key focus within our economy this year and May is recognized as college savings month, we felt now would be a good time to give an update on how education prices have changed in recent years relative to the change in all consumer prices.

When we consider the general amount of inflation our economy has experienced in recent years, education prices are one area that hasn’t had a comparable large rapid rise. The year-over-year (Y/Y) change in education prices peaked at 3.6% in April of 2023, while headline CPI had a peak Y/Y change of 9% in June 2022. Since education’s peak, prices have started to experience disinflation (prices are still increasing but at a slower rate). Education has a small weighting in the overall CPI index, consistently falling from a 3.5% to 2.5% weight over the past five years. So, its impact has been minimal. In March, education prices rose 2.4% on a Y/Y basis.

If we zoom out and look past the most recent years, inflation in education has been higher than average. Over the past 20-year period, education prices have more than doubled (+108%) or 3.7% per year. Overall inflation is +66.7% or 2.6% per year over the same 20-year period.

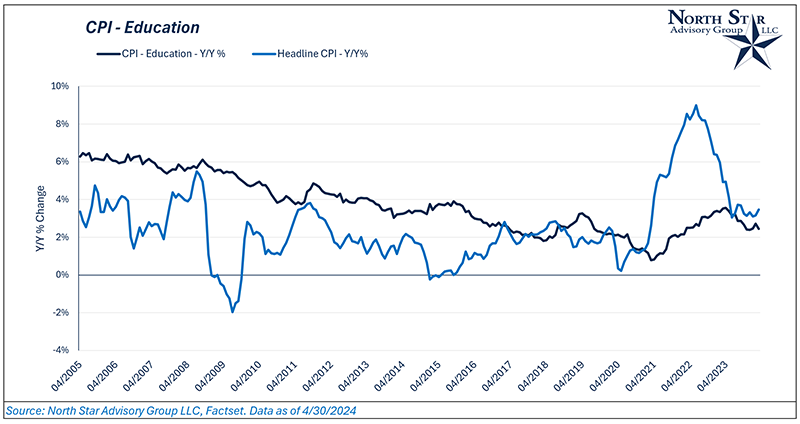

As you can see, education has been experiencing consistent disinflation from 2005 through 2021. Since 2021, price inflation has begun re-accelerating, but at a much slower pace than the overall economy. Why is this the case? An obvious reason would be the emergence of online education during the age of digitization.

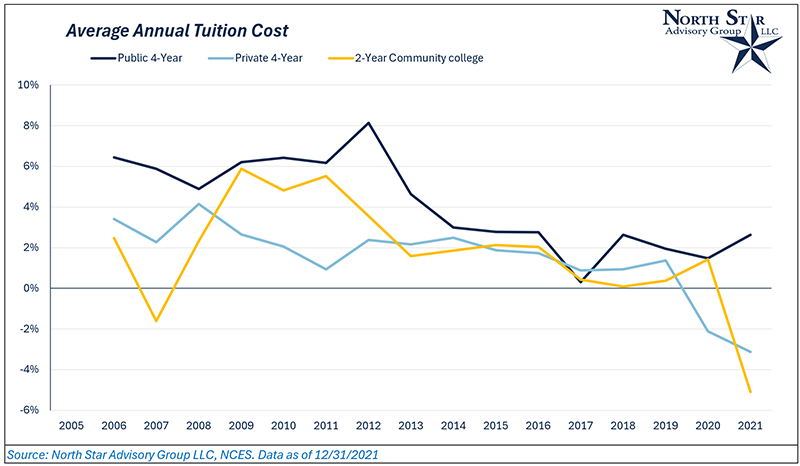

With that said, we’ll take things further and analyze the change in prices by school type (public, private, community college). Based on data from the NCES (National Center for Educational Statistics), the cost at each of these types of higher education has had a similar trend to CPI’s Education index through 2021 (Especially for public 4-year universities). The cost of online courses at these three types of institutions are included in the Y/Y % change in average tuition costs. While not every institution charges a lower rate for online versus in-person learning, online courses have definitely had a disinflationary impact on costs over time.

Having a better understanding of the potential tuition inflation rates over time allows NSAG to assist families more accurately in estimating their college savings rates.

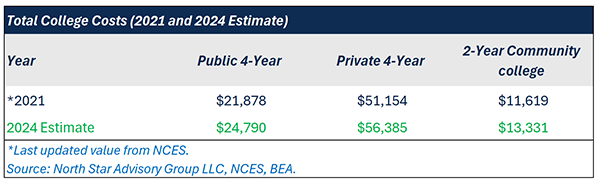

Average cost of schools

Now that we have a better grasp of the growth trends for tuition, we also need to understand the current total cost for each of these institutions, which includes room and board. In the table below, we’ve laid out the average annual cost (Tuition + room and board) for each.

Historically, room and board at college institutions have been cheaper than living off campus (renting). Although, as college dorms are aging, they require more maintenance and potential replacement which would require new financing. So, while it’s still cheaper than living off-campus, room and board is expected to grow at higher rates versus historical data. For our 2024 estimate, we separated tuition and room and board costs for each institution type in 2021, growing tuition at the current education CPI inflation rate and growing room and board by the current rate of CPI rental inflation in the U.S. The blended inflation rate amounts to ~4%.

NSAG provides a free software tool for clients that can help to estimate the average annual cost and projected total cost on a college-specific basis. This also includes a potential scholarship/grant analysis that takes ACT/SAT scores, GPA, major choice, etc. into account. Many families are amazed to see how much potential aid is available at various universities. Failing to look at net cost after aid could cause students not to apply to universities with a higher tuition rate that otherwise could have a similar net cost after potential aid.

Accounts to save for college

Saving for college is an important financial goal, and choosing the account can make a difference. The following is a sample list of account options to consider: Bank checking and savings accounts are a type of deposit account held at a financial institution, such as a bank or credit union.

- Positives:

- It’s one of the most liquid types of accounts, meaning you have easy access to your money. You can quickly deposit and withdraw funds as needed.

- Money held is insured by the Federal Deposit Insurance Corporation (FDIC) or National Credit Union Administration (NCUA).

- Negatives:

- Checking and savings accounts are designed for short-term use.

- Generally speaking, these accounts provide a lower potential rate of return when compared to long-term rates provided by the following account options.

- Many checking accounts charge monthly fees (up to $15). You can often waive this fee by maintaining a minimum balance or setting up direct deposit. However, the low interest rate earned often does not justify the fee waiver.

A brokerage account is an investment account held at a licensed brokerage firm.

- Positives:

- You can buy and sell a larger pool of investments such as stocks, CDs, bonds, mutual funds, and exchange-traded funds (ETFs).

- It’s a liquid account, meaning you can easily deposit and withdraw funds. Generally speaking, the funds are available within 5 business days.

- Unlike 529s and Roth IRAs, there are no annual contribution limits.

- Unlike Roth IRAs, there are no income requirements to contribute to a brokerage account.

- Because the funds are not specifically earmarked for education expenses, they can be used for anything.

- Typically, the funds are held in the parent or grandparent’s name. This provides greater control over when the child may be able to use the funds.

- If held in the parent’s name, for financial aid calculations on the FAFSA form, these funds are only calculated as a 5% resource, which increases any potential financial aid, versus 20% inclusion for a Uniform Transfers to Minors Act (UTMA) brokerage account.

- The funds are generally insured by The Securities Investor Protection Corporation (SIPC). The purpose of the SIPC is to expedite the recovery and return of missing customer cash and assets during the liquidation of a failed investment firm.

- Negatives:

- Because the savings are generally invested to achieve a higher long-term rate of return, there can be a risk of loss of principle.

A UTMA brokerage account is a type of custodial account designed to hold and protect assets for a minor until they reach the age of majority.

- Positives:

- Almost all the same noted above for brokerage accounts. Except for a few negatives noted below.

- The funds are generally insured by The Securities Investor Protection Corporation (SIPC). The purpose of the SIPC is to expedite the recovery and return of missing customer cash and assets during the liquidation of a failed investment firm.

- Negatives:

- All the same noted above for brokerage accounts.

- For financial aid calculations on the FAFSA form, these funds are calculated as a 20% resource, which may decrease any potential financial aid (versus brokerage accounts in the parent’s name).

- Each state that has adopted the Uniform Transfers to Minors Act (UTMA) has determined the oldest age at which a young person can receive property under the act. This age ranges from 18 to 25, depending on the state. Some states allow you to choose within a range or between two ages, while other states have a set age that you cannot vary. These hard lined ages reduce the control over when the beneficiary can take the dollars for whatever resource they would like.

- Because the savings are generally invested to achieve a higher long-term rate of return, there can be a risk of loss of principle.

A Roth IRA is primarily a retirement savings account, but it can also be used to fund higher education expenses.

- Positives:

- Contributions made with after-tax dollars and can be withdrawn tax and penalty-free at any time.

- The 10% early withdrawal penalty is waived if the funds are used for tuition, fees, books, supplies, and room and board for students enrolled at least half-time.

- Negatives:

- Contributions are limited based on annual contribution limits, which may be below your annual savings goals.

- Contributions may be limited or precluded based on your Adjusted Gross Income (AGI).

A 529 plan is a tax-advantaged savings account designed to help individuals save for current and future education expenses from kindergarten through graduate school.

- Positives:

- Some states offer state tax breaks for contributions.

- Unlike other savings plans, 529 plans have no annual contribution limits. Maximum aggregate limits vary by state, ranging from $235,000 to more than $500,000.

- These allow for tax-deferred growth of investments, and withdrawals are tax-free when used for qualified education expenses, including college tuition, fees, books, supplies, and some room and board costs.

- The account remains under the control of the donor, who is typically a parent or grandparent.

- 529 plan assets are considered parental assets for financial aid purposes, resulting in a lower impact on aid eligibility. Therefore, for financial aid calculations on the FAFSA form, these funds are only calculated as a 5% resource which increases any potential financial aid, versus 20% inclusion for UTMAs.

- NSAG does not charge an advisory fee to our clients for 529 accounts. It is one of the many ways that we help give back to our clients and students.

- Starting in 2024, beneficiaries can also roll over up to $35,000 tax-free to a Roth IRA in their names, subject to certain limitations. We discuss this new feature in greater detail in another section below.

- Negatives:

- 529 accounts cannot be held at a brokerage firm. They have to be held directly with the state sponsored mutual fund company.

- Virtually all 529 plans require physical paperwork and do not accept electronic paperwork like DocuSign.

- Each state limits the investment choices to a small number of mutual funds.

- Determined on a state-by-state basis, the tax deduction may be limited to a small amount or not available.

- Withdrawals must be used for qualified education expenses to avoid a 10% penalty and ordinary income taxes being applied to the earnings.

Remember that individual circumstances may vary, so it’s essential to work with NSAG to compare these options based on your specific needs, preferences, education expenses and tax advantages. When we talk, we can discuss a more exhaustive list of positives and negatives for each of the various accounts noted above. We can even discuss how the final savings plan may include a combination of several different accounts.

Rollover a 529 into a Roth IRA

When discussing funding 529 plans for children, a common concern among clients is the uncertainty of their child(ren) attending college. However, recent changes brought about by the SECURE 2.0 Act remove a common concern of what to do with unused 529 funds by allowing them to be rolled into a Roth IRA!

The SECURE 2.0 Act introduced a game-changing opportunity: transferring funds from an established 529 account to a Roth IRA for the same beneficiary. This move allows unused educational funds to kickstart a beneficiary’s Roth IRA savings. However, this transformation comes with its own set of rules and limitations.

We encourage clients to get assistance in navigating the rollover process. To make the most of this opportunity, it's crucial to understand the limitations. Here are some bullet points you should know:

- The 529 to Roth IRA rollovers are treated as a contribution.

- For example, the 2024 IRA/Roth contribution limit is $7,000. If the beneficiary made any IRA contributions, the rollover amount must be reduced by those contributions. Therefore, if the beneficiary contributed $2,000 to any IRA/Roth, the amount available for rollover is $5,000.

- Consequently, getting to the $35,000 lifetime limit may take more than five years.

- The rollover must be a plan-to-plan or trustee-to-trustee rollover. This means you cannot take a check from the 529 plan to deposit into the Roth IRA.

- The beneficiary is not subject to income limitations to contribute to a Roth IRA. For example, even if the beneficiary's income is more than $153,000 adjusted gross income limit for single filers in 2024, the beneficiary can make a rollover from the 529 plan to the Roth IRA.

- The beneficiary must have earned income, and the amount that can be rolled over is the lesser of earned income or the IRA contribution limit. Therefore, if the beneficiary is not working, no rollover is available because there is no earned income.

Case Study: Sarah's Scenario Let’s delve into a hypothetical example to illustrate the potential benefits. Meet Sarah, a 22-year-old with $30,000 in a 529 plan, opting not to pursue college. Faced with potential taxes and penalties on the unused funds, Sarah's parents explore the SECURE 2.0 strategy.

Executing the SECURE 2.0 strategy, Sarah's parents can convert up to $35,000 tax-free into Sarah's Roth IRA. Due to annual contribution limits, this strategic move is spread over multiple years to fully transfer the remaining 529 plan assets.

- 2024: $7,000 to Roth IRA, $23,000 remaining in 529

- 2025: $7,000 to Roth IRA, $16,000 remaining in 529

- 2026: $7,000 to Roth IRA, $9,000 remaining in 529

- 2027: $7,000 to Roth IRA, $2,000 remaining in 529

- 2028: $2,000 to Roth IRA, $0 remaining in 529

Assuming a 7% average annual return and no additional contributions from Sarah, the $30,000 could grow to an impressive $449,234 by Sarah's retirement age of 67. Since these amounts are within the Roth IRA, these dollars are tax free after 59 1/2! Disclaimer: It's essential to note that this example is purely illustrative and doesn’t account for actual investments, taxes, fees, expenses, or inflation. Individual results may vary, and past performance does not guarantee future results.

Leveraging SECURE 2.0 to better utilize unused 529 plan funds presents a compelling strategy for building generational wealth. Funding Roth IRAs at a young age can be immensely valuable for several reasons, potential benefits include:

- Tax-free growth: The significant advantage here is that any earnings and growth within the Roth IRA are tax-free. This becomes particularly powerful over time as you can potentially benefit from compounding interest.

- Time as a powerful ally: Time is a critical factor when it comes to compounding. By contributing to a Roth IRA early in life, you harness the power of time to your advantage. The more years your money grows, the more significant the compounding effect becomes. Starting early allows you to make the most of the potential exponential growth that comes with compounding.

- Exponential Growth Through Compounding:

Compound interest is often referred to as the "eighth wonder of the world," because of its ability to create exponential growth. When you contribute to a Roth IRA, your initial investment earns returns. In subsequent periods, these returns are not only earned on the original contribution but also on the previously earned returns. This compounding effect accelerates the growth of your investments over time.

NSAG new hires

To maintain our high level of service, NSAG’s staff is growing with three new additions coming on board Monday May 13th.

Hugo S. Souza

Financial Advisor

Hugo joins North Star Advisory Group in May 2024 as a Financial Advisor. His primary role will be to assist with high-net-worth clients and new 401(k) plans. Prior to joining NSAG, Hugo gained extensive experience working at two financial planning firms: one in Cleveland, Ohio and one family office in Boston, Massachusetts. Outside of work, he enjoys working out, running, golfing, and attending sporting events. He played D1 NCAA football at University of New Hampshire where he earned his Bachelor of Arts in Political Science with a Business Minor. Hugo lives in University Heights, Ohio with his two boys, who attend University School.

Click HERE to read Hugo’s full bio.

Rachel M. Smylie

Paraplanner

Rachel joins North Star Advisory Group in May 2024 as a paraplanner. Prior to joining NSAG, Rachel was a sales operations coordinator for a Financial Planning company in downtown Cleveland, Ohio. She also spent five years as the assistant director of education and as a lead preschool teacher at local Temples. Rachel lives in Solon, Ohio with her husband Jordan, and their two children Liz and Kyrian.

Click HERE to read Rachel full bio.

Nick I. Stern

Intern – Summer 2024

Nick will enter his senior year at Bowling Green State University in the fall of 2024 with a Bachelor of Science in Business Administration and a major in finance. Nick is the President of BGSU’s Financial Management Society (FMS), a position that both Mark Kangas and Forrest Kuchling have previously held.

Originally from the suburbs of Columbus, Ohio, Nick enjoys golfing in the summertime, attending various sporting events, such as Ohio State Basketball and Columbus Blue Jackets Hockey (although he enjoys watching the Detroit Red Wings more), and any other ways he can enjoy sunshine and the company of others.

Where will the stock market go next?

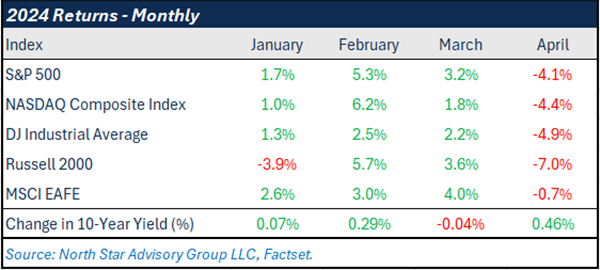

Over the past two months, we have written to clients about the potential for near-term volatility in the equity markets. (Click to read March or April’s Timely topics). In April, we saw a bit of this volatility creep into the equity markets as investors increasingly revised and reduced their rate cut expectations for 2024. At April’s lows, we saw the most pain in the technology sector and small cap stocks as they are most rate sensitive. Although, technology stocks (Nasdaq) recovered some of those deeper losses in the final week of April, despite no big down move for interest rates. This leads us to believe that there could still be some further valuation pressure for some technology stocks in the short term.

For the month, the U.S. 10 Year yield has risen 48 bps from 4.20% to 4.68%. The S&P 500 fell 4.1%, the Nasdaq 100 fell 4.4%, the Dow Jones fell 4.9% and the Russell 2000 (small cap) fell 7%. The S&P was up 3.2% in March and although we’ve given up those gains in April, the index is still positive for 2024 (+6%).

April’s down move in equities represents the market digesting the change in rate sentiment experienced over the first 4 months of 2024, as shown by the change in the U.S. 10 year yield.

The CBOE Volatility Index (VIX), which tracks the expected volatility for the S&P 500 over a 3-month period, was up 2.6 points from 13 to 15.6. Showing investors’ expectations for increased volatility in the near term.

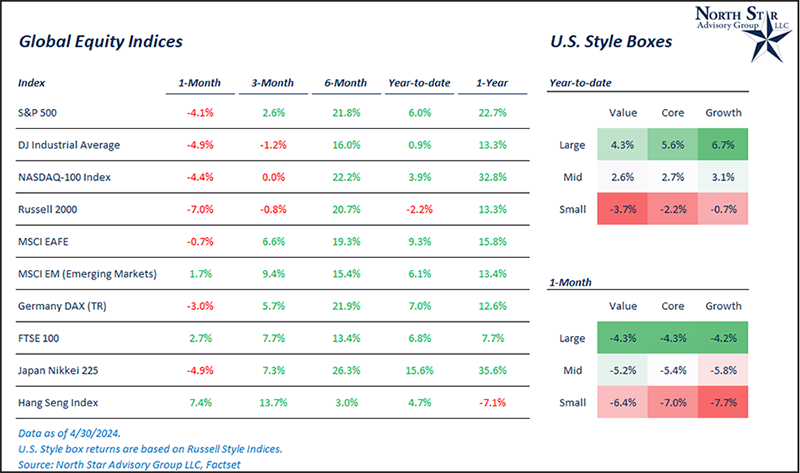

International developed stocks are now performing better than the U.S. markets for 2024. The MSCI EAFE Index (International Developed) is up 9.3% in 2024 after being down 0.7% in April. Japan, Italy, France, and Germany are the best performing developed countries so far this year.

We are passionately devoted to our clients' families and portfolios. Contact us if you know somebody who would benefit from discovering the North Star difference, or if you just need a few minutes to talk. As a small business, our staff appreciates your continued trust and support.

Please continue to send in your questions and see if yours get featured in next month’s Timely Topics.

Best regards,

Mark Kangas, CFP®

CEO, Investment Advisor Representative