Each month we ask clients to spend a few minutes reading through our newsletter with the goal of raising their investor IQ. Since May is college planning month, we are focusing on kids big and small from ages 0-100.

- 529s for ages 0-100

- Investing for kids 8-12s

- Roth IRAs for ages 14-18

- College selection & financial aid

- Where will the equity markets go next?

529s for ages 0-100

Many families are still not fully aware of the benefits of 529 plans. 529 plans are education investment accounts with special rules and tax benefits that help families save for K-12 tuition, qualified higher education expenses, vocational school, apprenticeship fees or expenses. These plans come in multiple forms: a prepaid tuition plan or a savings plan that allows after-tax contributions toward investments in mutual funds and exchange traded funds. NSAG is a strong believer in the importance of higher education and giving back to the next generation. For this reason, NSAG does not charge a fee on any 529 accounts. 529 plans offer several benefits, including but not limited to:

- Federal tax breaks and flexibility of use. You won’t pay taxes on 529 plan earnings, provided you use the money for K-12 tuition, qualified higher education expenses, vocational school, apprenticeship fees or expenses.

- State tax breaks. Some states offer tax deductions or credits for contributions to a 529 plan.

- A variety of flexible investment options that can be changed including: ETFs, Mutual Funds, actively managed and passively managed.

- Contributions are not limited or restricted based on the donor’s income.

- Assets held in a 529 are outside of the donor’s estate.

- Multiple people can contribute to the same 529 account.

- The account owner retains control of the 529 and can even change the beneficiary.

Contact us today to discuss additional details or questions you have regarding 529 plans.

Investing for kids ages 8-12

To help the next phase of the learning process, we focus on children ages 8-12. NSAG is provide inquiring clients with a free activity book. Simply call or email to let us know who the book is for and we will mail out your free copy. There is no catch, we just found a great resource that we would like to share with our clients. The book provides kids with 65 engaging activities about saving, investing, and growing their money.

Through educational and engaging exercises, they’ll learn how to track their spending, make good investments, and so much more.

- Build a financial vocabulary. Your kid will sound like a finance pro as they learn all sorts of important financial terms like mutual funds, debit vs. credit, and simple interest vs. compound interest.

- Explore engaging activities. They’ll develop their money management smarts through 65 awesome exercises like figuring out what type of spender they are and determining their saving goals.

- Discover shrewd tips. Help your kid find advice on the best ways to handle their personal finances, from the benefits of setting a budget to the importance of diversifying their investments.

This is the perfect age to engage with a child who is either interested about invested or begin the process of raising their Investor IQ. Here are some tips on how to get started:

- Explore investing as a family to teach the keys to long-term wealth. The free activity book NSAG is providing starts the interactive dialog among the family.

- Work with kids to pick stocks of companies whose products and services they understand and use or a product or service that they care about.

- Teach them that investing is about the long term.

- Start small and learn from mistakes. Some of the best investors have learned from their mistakes and learned how to minimize the impact of their mistakes.

- Make it a habit. Repetitive investing creates healthy habits financially. There is no short cut to investing and wealth creation.

- Finally, encourage your child to learn more about investing vs online gambling.

It’s important that your child understand why investing is so powerful in the first place. Compound interest is one of the most important concepts for kids to learn about investing. Once your child has a grasp on spending and saving fundamentals, you can introduce them to basic investing concepts, such as “what is a stock” or “what is a bond.” Keep the discussions simple and easy for your child to understand.

Let us know as their interest grows, their questions become more difficult or you believe the child will benefit from a conversation with our team. We are looking forward to sending out a lot of books this summer!

Roth IRAs for ages 14-18

A minor Roth IRA can be a great way to give your child a head-start on their retirement savings and teach them about financial literacy. Here are some benefits of a minor Roth IRA:

- Minor or Custodial Roth IRAs give your child a head-start on retirement savings. By contributing to their retirement savings early on, your child will benefit from decades of tax-free, compounding growth.

- Like adult IRAs, minors can contribute up to $6,500 per year in Roth IRA contributions, but no more than they earn.

- Teaching your child about retirement funds early on gives them a head start in financial literacy.

- Saving for retirement will become natural for your child as they enter adulthood.

- There are not any age restrictions on a child's earned income. So as long as your child has taxable earned income, they can open and contribute to a Roth IRA. Allowance, unreported income (babysitting, tips…) does not count.

- Minors can withdraw contributions (not earnings) at any time after five years without penalty.

- Since a child can earn up to $13,850 without paying income tax, the long-term benefits and flexibility of a Roth IRA tend to be larger than a Traditional IRA.

There are a few things to consider before opening a minor Roth IRA:

- A parent or guardian must open the minor Roth IRA for a child under the age of 18.

- All investing involves risk. Therefore, it is important to help guide and educate the child on investing.

NSAG clients have had great success in encouraging minors to contribute to a Roth IRA when the parents match their contributions. While the total combined contribution is still limited to the lesser of their earned income of $6,500, NSAG has seen an increased participation rate by minors. The parent’s match contribution encourages minor participation in a very similar manner as employer match contributions do for work retirement plans. The minor match contribution also teaches the child early on of the benefits of the company match.

Contact NSAG if you would like to learn more and possibly get the get the process started.

College selection & financial aid

Choosing a college can be a daunting task, but there are some steps you can take to make it easier. This month, we provide a list of tips that might help make the process easier and less expensive.Years before a student even starts the process, it is helpful to visit various universities to get a better understanding of the look and feel of their environment. It maybe helpful to add these quick visits either into an existing vacation or as a day trip on the weekend.

- Make a list of your academic interests and preferences.

- Discover what specific qualities you want in a college.

- Net cost and fees: It is important to look past the posted tuition and expected net tuition after expected financial aid and scholarships.

- Size: campus and class

- Location: City vs rural

- Campus life: Types of housing options, fraternities, sororities, social clubs

- Distance from home or family

- Safety

- Majors & Minors: variety of programs they offer which may allow you greater ability to switch if necessary and remain at the same institution

- Their national ranking in your preferred program(s)

- Access to and requirements for internships and study abroad

- Average wage after college

- Job placement percentage

- Perspective: how the school makes you feel. Will you be able to grow and develop personally and academically?

- Create an initial list of colleges that match this criteria.

- Research your chances of getting into each of these colleges and organize your school list by “reach,” “maybe,” and “likely.”

- Narrow down your results into your final list of colleges.

- Talk to North Star as NSAG provides another free resource and service to our clients. NSAG has access to a tool that helps families reduce the probability of student’s getting over their head with student debt.

- Instantly sort colleges based on your admission preferences and find which of these will provide the most in financial aid and scholarship discounts.

- Find instant, accurate cost projections for every college in the country. Financial aid, scholarship, admission, and salary data all in one place. For every college.

- Apply & start visiting campuses

- It is time to rerank the schools after acceptance letters and financial aid packages are provide.

The financial aid process continues once the student is on campus. Financial aid counselors, faculty advisors, department chairs, peers and student groups are great resources to find and get access to additional scholarships, grants, work studies and internships available after the student’s first semester.

Finally, for parents that need additional help, there are professionals that help walk students through the entire process.

Two ways the global economy has impacted universities:

- Due to COVID, many schools have modified or dropped their testing requirements for admittance. Many scholarships have a minimum testing requirement to become eligible for their support. A lower number of students taking tests may provide a greater probability of receiving scholarships with testing requirements.

- Due to a lower birth rate stemming from the global financial crisis in 2008, universities are expecting a smaller number of student applications starting in 2026. The large state institutions will likely maintain their enrollment numbers as they pull students from the smaller state schools. Smaller state schools will simultaneously struggle financially and have less students applying for existing scholarships.

Please do not hesitate to reach out if you have any questions or if you would like our assistance in helping guide your conversations.

Where will the equity markets go next?

We believe that the equity markets will continue to be hyper focused on corporate earnings and margins over the coming quarters. Inflation and monetary policy were the forefront concern for investors in 2022. 2023’s investor focus has shifted to a greater emphasis on corporate earnings and margins. Corporate earnings, margins and inflation help show the impact of the Federal Reserves policies over the past 12-15 months.

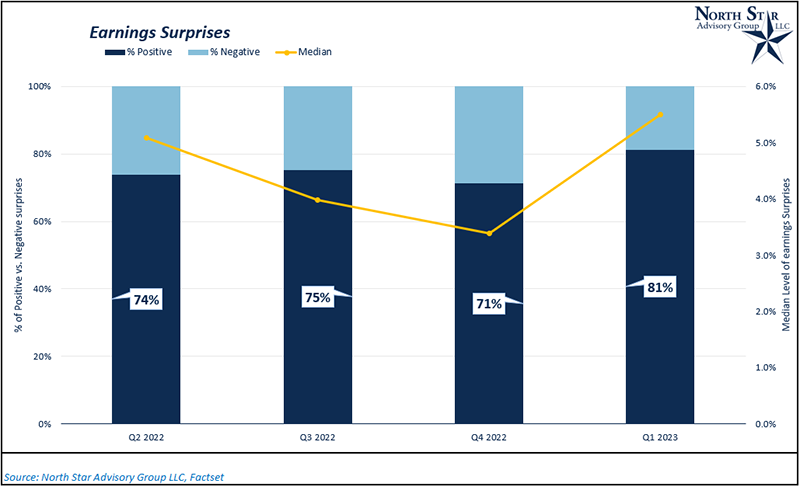

As earnings season is just getting through its busiest week, as of 4/26/2023, 218 of S&P 500 companies have reported their Q1 2023 earnings. Of those 218 companies, 81.2% (177 out of 218) of companies had positive earnings surprises relative to the street’s consensus estimates. The median surprise through Q1 2023, including both positive and negative surprises, was +5.5%. Over the past 4 quarters, we’ve seen a steady increase in the number of positive surprises.

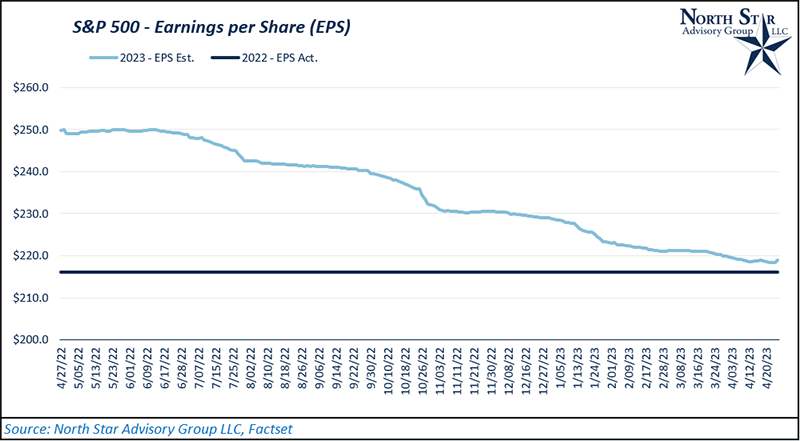

While companies continue to beat current expectations, generally, they have been guiding lower on EPS over the past year. Most companies give investors guidance on future earnings (usually 12 months out), which heavily influences forward-looking analyst estimates. Over the past 12 months, the S&P 500’s calendar year 2023 EPS estimate has decreased from ~$250/share to ~$219/share, down ~13%. Although the 2023 estimate has decreased to $219/share, that estimate is still higher than 2022’s actual EPS results ($216/share).

Earnings estimates have come down, however we are not forecasting an earnings collapse. While it’s not a collapse, we could see a continued deceleration in the earnings growth rate due to the lagged effects of monetary policy, tighter credit conditions and inventory reductions. Additionally, as companies have guided lower, they continue to subsequently beat those guidance numbers in the following quarters. This could be a sign that management teams are giving themselves room for error in their guidance. On 4/27/2023, preliminary real GDP grew at an annualized rate of 1.1% for Q1 2023. This was less than the 1.9% rate expected by forecasters. While still positive, economic growth was at slower pace compared to 2022 and Q1 2023 forecasts.

The current economic slowdown has been widely expected and we are likely in the middle of the two worst quarters for the slow down. We expect Q2 2023 to be the hardest part of the slowdown. Many companies that we have talked to expect their inventory to hit desired levels this summer, which will in turn begin to drive up production needs. Programs quickly put in place by the Federal Reserve have helped concerns over a global financial contagion slowly fade and refocus on the potential impacts of slower lending by regional banks. To ease the potential pressures of less lending, the Fed is already discussing a reduction or elimination of future rate hikes after May’s anticipated 0.25% increase.

We continue to encourage clients to stay properly diversified as market volatility can be swift in both directions.

We are passionately devoted to our clients' families and portfolios. Contact us if you know somebody who would benefit from discovering the North Star difference, or if you just need a few minutes to talk. As a small business, our staff appreciates your continued trust and support.

Please continue to send in your questions and see if yours gets featured in next month’s Timely Topics.

Best regards,

Mark Kangas, CFP®

CEO, Investment Advisor Representative