Each month we ask clients to spend a few minutes reading through our newsletter with the goal of raising their investor IQ. January’s Timely Topics commentary wraps with Wall Street’s outlook for 2024, as well as an analysis of different market segments across the globe.

- Markets at an all-time high?

- S&P 500 2024 targets

- Important changes in 2024

- 401(k) changes in 2024

- New Year’s resolution

- Where will the equity markets go next?

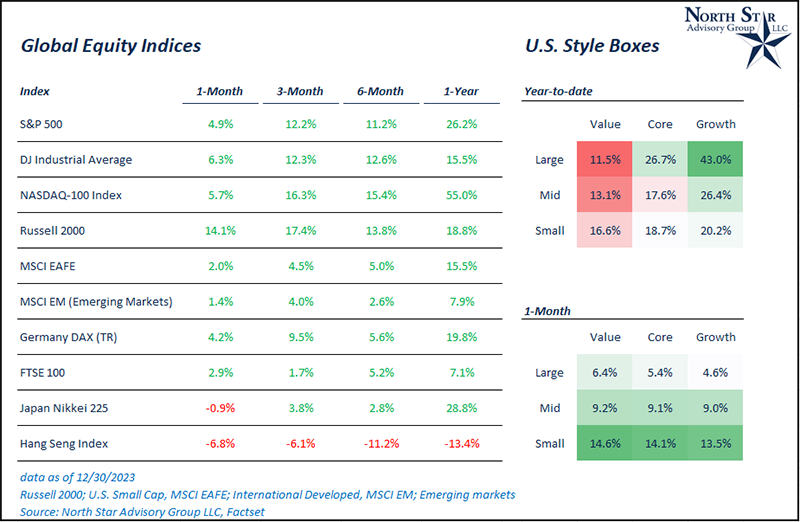

Markets back to an all-time high?

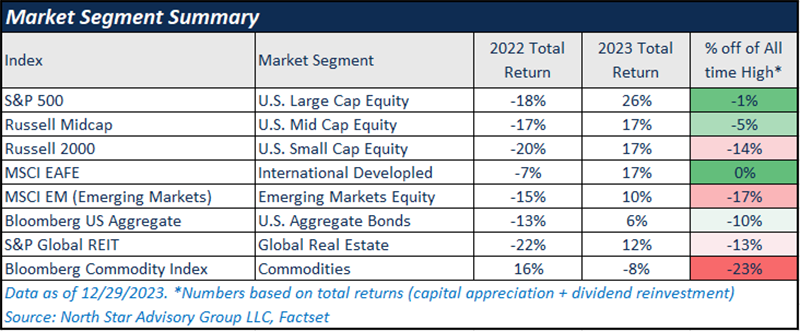

Many clients have asked why their portfolio values may not be back to all-time highs yet, given the fact that the S&P 500 has made a full recovery of its 2022 losses. While the S&P 500 is right near all-time highs, not all segments of the market across the globe have experienced the same level of recovery.

U.S. large cap equity (S&P 500) and international developed equity (MSCI EAFE Index) are the only two major market segments that are at or near all-time highs based on index total returns. U.S. small cap, U.S. mid cap, emerging market equity, global real estate, U.S. bonds, and commodities are all yet to reach new all-time highs based on total returns.

In the case of small cap equities, real estate, U.S. aggregate bonds, and emerging markets, these segments had begun falling from all-time highs in the second half of 2021. For emerging markets, Chinese equities have had the largest negative impact on returns. For small cap equity, a large portion of this market has unprofitable “junky” businesses within the index (Russell 2000), and these names have struggled to recover losses under a restrictive monetary policy time period. Although, small cap equities have greatly outperformed large cap equities over the past 1-2 months, as the Federal Reserve has signaled an end of rate hikes (and multiple potential rate cuts in 2024). NSAG continues to favor small cap equity (with a focus on quality: lower leverage and high profitability), as well as emerging markets (without an overconcentration into select areas and names in China).

The most prominent reason for portfolio values failing to reach new highs would be due to potential bond allocations. Investors who purchased and held aggregate bond funds/ETFs in 2022 experienced the worst returns for aggregate bonds on record (Bloomberg US Aggregate Index). NSAG has continued to recommend high-quality short-duration individual bonds, which have not experienced the same returns as the Bloomberg US Aggregate in both 2022 and 2023.

S&P 500 2024 Targets

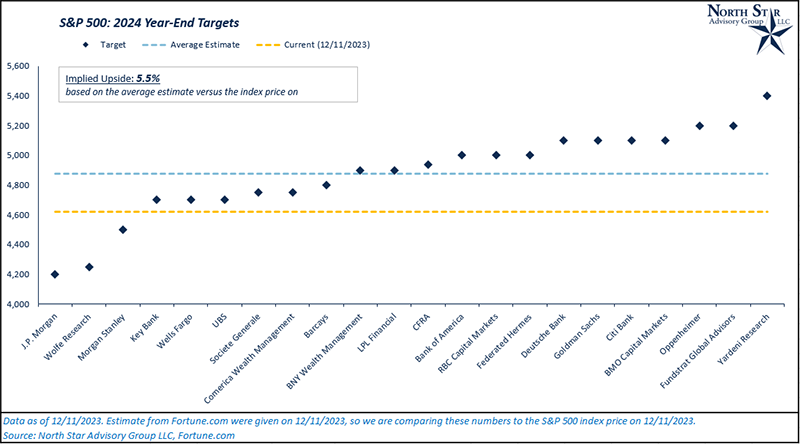

An end of the year tradition continues to involve reading through major investment banks, research firms, and asset managers’ market outlooks for the upcoming year. In the chart below, we’ve summarized multiple year-end 2024 estimates for the S&P 500.

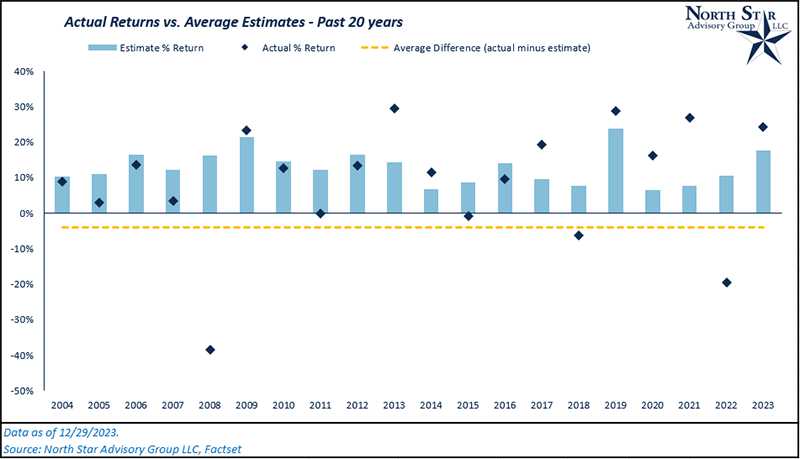

Based on each firm’s estimate from 12/11/2023, the average year-end 2024 target price for the S&P 500 is 4,877. This implies a 5.5% upside potential for the index price. While positive, these estimates are lower than the average price return for the S&P 500 over the past 20 years (9%) and lower than the average estimate return over the past 20 years (~13%).

As you may recall, NSAG has pointed to the fact that S&P 500 estimates on average are rarely accurate. Over the past 20 years, Wall Street (on average) has never forecasted a down year for the S&P 500. Going into 2024, this fact remains true based on the target price of 4,877. Additionally, estimates tend to be overestimated by ~4% on average over the past 20 years, but this is dragged down by outlier years, such as 2008 and 2022.

From a statistical point of view, we want to analyze the volatility of estimates. The past 20 years of estimates versus actual data have a volatility of 16% and a standard error of ~4%. With that being said, we can say that there is a 95% probability that S&P 500 estimates will either be overestimated by ~11% or underestimated ~4% (a 15% range).

For this reason, NSAG does not put a large focus on tracking this data consistently, and we would tell clients to take these estimates with a grain of salt.

Important Changes in 2024

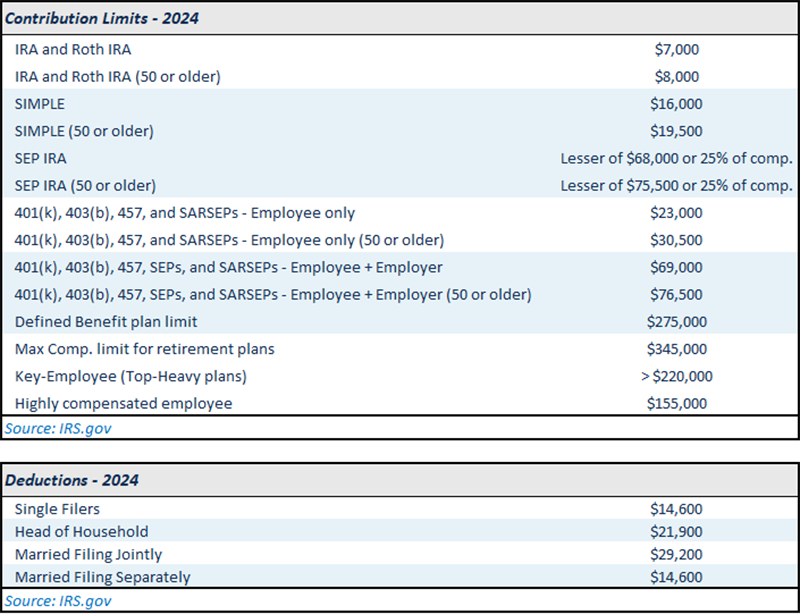

As we enter the new year, it’s important to remind clients of updates to the tax code.

For 2024, we’ve outlined a few key changes below. To see the full NSAG 2024 Tax Guide, click HERE.

Regarding social security, payments for 2024 are receiving a 3.2% boost in comparison to 2023. (Much lower than last year’s year-over-year increase of 8.7%. Additionally, standard monthly Medicare premiums are rising by $9.80/month to $174.70/month in 2024, representing a 5.9% increase in comparison to 2023 premiums.

401(k) changes in 2024

SECURE Act 2.0 is here, and this law adds more than 90 new provisions to help Americans save through employer-sponsored plans. NSAG is here to help you learn about the ins and outs of SECURE 2.0 and how businesses can take advantage of increased tax incentives. The following are a few of the key changes that impact employees and businesses today.

Tax incentives to offer a new 401(k)- We covered this topic in depth in our February 2023 Timely Topics. Click HERE to read more.

Long-term, part-time employee eligibility

- Long-term, part-time employees will now become eligible sooner under the SECURE 2.0 Act, enabling them to begin saving for their future earlier and putting them in a better position to achieve their retirement goals.

- The original SECURE Act (1.0) required that long-term, part-employees (those who worked between 500 and 999 hours for three consecutive years) be eligible to participate in their company's retirement plan. Under the new law, that requirement will be reduced to two years starting in 2025.

- Under this act, employers aren't required to match contributions for these employees.

- Important: If an employee shouldn't receive a match, make sure you select “exclude” this employee from the company match checkbox when adding a retirement plan. Only employers offering a match will see this checkbox. Confirm plan rules with your retirement provider.

Required minimum distributions

- The age requirement to begin taking RMDs will increase from age 72 to 73 in 2023 and then age 75 in 2033. The penalty for not taking an RMD is now reduced from 50% to 25%, and in some cases to 10%. Beginning in 2024, the RMD requirement for Roth 401(k) accounts during a participant's lifetime will be eliminated.

Student loan matching contributions

- Beginning in 2024, student loan payments could count as retirement contributions for the purpose of qualifying for matching contributions in a workplace retirement account. Employers will also be able to make contributions to their company retirement plan on behalf of employees paying student loans instead of saving for retirement.

- The matching contributions for student loan payments must vest under the same schedule as other matching contributions. Additionally, employees must be eligible for a match in order to receive the student loan matching contribution.

Do not hesitate to reach out to NSAG if you have any questions regarding your company plan and recent changes due to the SECURE Acts.

For those who are curious… The Setting Every Community Up for Retirement Enhancement (SECURE) Act is a 2019 law designed to help more Americans save for retirement. It was part of a more comprehensive spending and tax extension bill that was signed into law by former President Donald Trump on Dec. 20, 2019. SECURE 2.0 was signed into law by President Joseph Biden on Dec. 29, 2022 as part of the Consolidated Appropriations Act (CAA) of 2023.

New Year’s resolution

It’s easy to fall into the trap of overspending on food delivery services, especially when you’re busy and don’t have the time to cook. However, this habit can quickly add up and put a dent in your finances. NSAG has been sounding the alarm to clients on the rising costs of eating out for the past 10 years. Recently, NSAG has seen a significant increase in percentage of discretionary spending going towards eating out and food delivery services.

According to recent research1, the average American spends a lot of money on food delivery. Each order for one person costs $34 which equates to an average spend of $153 per month and $1,850 per year. This includes the food, the delivery fee, the service fee, the tip, and the taxes. These fees may differ depending on the restaurant, the app, and the location, but they can make a big difference over time. For comparison, the average cost per meal for a prepared meal service is $7, and the average cost per meal for cooking at home is $4.30. Therefore, food delivery services are not the most cost-effective way to get food, especially for regular users. NSAG’s concern grows as you expand these projected costs from one person to a family and once a week to multiple times a week. While the spend seems small, the annual cost is significant and we are seeing it show up in client spending.

If you’re looking to cut back on your spending in 2024, making a resolution to use any of the combination of the following is a great place to start:

- Cook at home more regularly

- Pack 4-5 lunches a week for those who work in an office. A savings of $10 per lunch four days a week can add up to almost $2,000 per person per year!

- Order less takeout. Even without food delivery charges, takeout food can cost 2-4 times the cost of preparing a meal at home.

- Pick up your order instead of using food delivery services.

- On average, each American spends $13 per order on service fees, delivery fees, and tip expenses. For those who order once a week this adds up to approximately $655 annually!

- Restaurants may also benefit by keeping a larger portion of sale.

Here are some tips to help you get started:

- Ask your family what they would like to have for the week. Getting the family to provide their input increases the chances they will follow the plan.

- Plan your meals: Take some time to plan out your meals for the week. This will help you avoid the temptation to order takeout when you’re feeling too tired or busy to cook. Some families have had success in providing a calendar and voting what they would like each day.

- Cook in bulk: Save time and money by cooking meals in bulk and freezing them. This way, you’ll always have a healthy meal on hand when you’re short on time.

- Shop smart: Look for deals and discounts on groceries. You can also save money by buying generic brands instead of name brands.

- Try new recipes: Cooking can be fun and exciting, especially when you’re trying out new recipes. Look for inspiration online or in cookbooks to keep things interesting.

Remember, making a resolution to cook more and order less takeout is a great way to save money, curb inflation and eat healthier in 2024.

Throughout this year, NSAG will provide a few simple and quick recipes to encourage clients to add ways to build on this new resolution for 2024.

Good luck!

1) Source: https://getcircuit.com/teams/blog/hidden-cost-of-delivery

Where will the equity markets go next?

At the close of 2023, the S&P 500 hovers right around its all-time high levels after a 5% return in December. Historically, Q4 has been a seasonally strong part of the year for equities, and 2023 has been no different, driven by strong returns over the past two months. Notably, small cap equities (Russell 2000 Index) were up 12.6% in December as interest rate levels continued to lower, with longer term yields decreasing faster than shorter term yields. This was the index’s third best month in the past 20 years. Broadly, many areas of the market are flashing short-term overbought signals following strong back-to-back months for equities. Although, underneath the hood, we continue to see strong market breadth as the rally has continued to broaden and not be solely driven by the “magnificent 7” companies. The advance/decline line saw an increase of ~1,800 in December (Net advancing stocks +1,800 is in the top 7% of monthly changes over the last 20 years). At the end of December, 89% of S&P 500 constituents sit above their respective 50-day moving averages. The outperformance in small cap equity is also evidence of strengthening equity market internals.

We are passionately devoted to our clients' families and portfolios. Contact us if you know somebody who would benefit from discovering the North Star difference, or if you just need a few minutes to talk. As a small business, our staff appreciates your continued trust and support.

Please continue to send in your questions and see if yours get featured in next month’s Timely Topics.

Best regards,

Mark Kangas, CFP®

CEO, Investment Advisor Representative