Each month we ask clients to spend a few minutes reading through our newsletter with the goal of raising their investor IQ. This month we break down one of the largest overhauls to retirement plans in more than 20 years and how it impacts all companies, savers and retirees.

- Retirement plan overhaul

- Incentives to offer a new 401(k)

- Benefits for current savers

- RMD changes for retirees

- Cost of waiting

- Where will the equity markets go next?

Retirement plan overhaul

Washington just passed one of the largest overhauls to retirement plans. The changes impact companies, employees and retirees. The SECURE 2.0 Act was included in the Consolidated Appropriations Act of 2023 that was signed into law on 12/29/22. The SECURE 2.0 Act has 92 provision changes to retirement plans that are almost universally good, with “good” being defined as “helpful to the cause of promoting retirement security.”

The following selections outline in a bit more detail about what we consider to be the most relevant provisions for employees, small and medium-sized employers who maintain a retirement savings plan or are considering doing so, and retirees.

Before we get into the larger changes to retirement plans, we will cover two brief sections on retirement plans for smaller businesses who are not ready to offer a 401(k) or 403(b).

“Starter” 401(k) and 403(b) plans

- Starting in 2024, employers that do not already offer a retirement plan can offer a “Starter” 401(k) or 403(b) plan, whereby:

- employees must be automatically enrolled at a default salary deferral contribution rate of between 3% and 15% (but can choose to opt out),

- the annual salary deferral contribution limit is the same as IRA contribution limits, and

- employer contributions are neither required nor permitted.

- These basic “Starter” plans can be adopted at an employer’s discretion and are very similar to programs that have been mandated by several states for employers that don’t already offer a retirement savings plan.

SIMPLE IRAs

- Starting in 2023, employers sponsoring a SIMPLE IRA can allow employees to make contributions on a Roth basis.

- Starting in 2024, SIMPLE IRA plan sponsors may make an additional employer contribution of up to 10% of employee wages (capped at $5,000).

- Also starting in 2024, a SIMPLE IRA plan sponsor can change to a safe harbor 401(k) plan mid-year (whereas currently the change can only take place as of the next January 1).

Incentives to offer a new 401(k)

The cost for plan administrative costs and employer contributions to employees has long been the #1 reason why employers have been reluctant to start a work retirement plan. Starting in 2023, the SECURE Act 2.0 provides for tax CREDITS for each of these expenses!

Startup plan tax credit – PLAN EXPENSES- Effective in 2023: for employers with 50 or fewer employees, the Startup Plan Tax Credit amount has been increased from 50% of the startup and ongoing service fees that are paid by the employer to 100% of the startup and ongoing service fees that are paid by the employer for each of the plan’s first three years (but capped at $250 times the number of eligible non-highly compensated employees). Service fees that are deducted from employee accounts are not considered when calculating the tax credit amount. An employer is only eligible for the tax credit for the first three years during which it maintains any type of retirement plan. For example, if an employer sponsors a SIMPLE IRA plan for two years and then replaces it with a 401(k) plan, the three-year eligibility period would not start over in the year the 401(k) plan is adopted.

- For most employers with 50 or fewer employees, this provision is significant because:

- The Startup Plan Tax Credit should cover 100% of the plan’s service fees for each of the plan’s first three years, so there will be no cost to the employer for each of those first three years,

- It will incentivize employers to pay service fees that they otherwise might have chosen to have deducted from employee accounts when the tax credit was previously capped at 50%,

- It will incentivize employers to select optional add-on services (e.g., 3(16) fiduciary services and payroll integration services) to reduce their fiduciary responsibility and ease their administrative burden, and

- Employers inclined to select the lowest-cost provider might now consider other providers because the tax credit will cover 100% of their plan expenses for each of the plan’s first three years regardless.

- For employers with 51 to 100 employees, the maximum tax credit amount remains 50% of the startup and ongoing service fees that are paid by the employer for each of the plan’s first three years.

- For all employers with 100 or fewer employees, the additional tax credit amount of $500 for startup plans with an automatic enrollment provision still applies.

- Legal guidance has suggested to NSAG that plans started prior to 1/1/2023 are eligible for the revised start up plan tax credit for plan expenses described above. Please consult with your tax professional on their interpretation.

Startup plan tax credit – EMPLOYER CONTRIBUTIONS

- Starting in 2023, employers with 50 or fewer employees will get a tax credit based on employer contributions (nonelective and/or match) that are made to employees during a new plan’s first five years. This tax credit is separate from – and in addition to – the Startup Plan Tax Credit on plan expenses (described above). The tax credit on employer contributions will apply as follows:

- The amount will be based on the employer contributions that were made to employees with gross wages below $100,000 during the year,

- The tax credit amount will be calculated as follows:

- Year 1 (i.e., the year the plan is effective) – 100% of the employer contribution amount (capped at $1,000 per employee)

- Year 2 – 100% of the employer contribution amount (capped at $1,000 per employee)

- Year 3 – 75% of the employer contribution amount (capped at $1,000 per employee)

- Year 4 – 50% of the employer contribution amount (capped at $1,000 per employee)

- Year 5 – 25% of the employer contribution amount (capped at $1,000 per employee)

- Employers with 51 to 100 employees are also eligible for the employer contribution tax credit, although at a reduced rate based on a separate (and more complex) formula.

- Legal guidance has suggested to NSAG that plans started prior to 1/1/2023 are NOT eligible for the revised start up plan tax credit for employer contributions described above. Please consult with your tax professional on their interpretation.

Mandatory automatic enrollment in startup 401(k) plans

- Employers who establish a new 401(k) plan in 2025 or later will be required to automatically enroll employees at a rate of between 3% and 10%, and with “automatic escalation” causing the rate to increase until leveling off at something between 10% to 15%. Employers with ten or fewer employees are exempt from this requirement. 401(k) plans established prior to 2025 will be grandfathered and will not be required to automatically enroll employees.

Benefits for current savers

The SECURE Act 2.0 boosted the amount that can be saved into retirement accounts and surprisingly now allows for employees to elect for employer contributions to be made as an after-tax Roth.

IRA & Roth contribution limits were increased for 2023.

- The contribution limit for individuals under age 50 was increased from $6,000 to $6,500.

- The contribution limit for individuals aged 50 or older was increased from $7,000 to $7,500.

- As a reminder, IRA and Roth contributions for 2022 can be made through April 18, 2023.

401(k), 403(b) and 457 employEE contribution limits were increased for 2023.

- The contribution limit for individuals under age 50 was increased from $20,500 to $22,500.

- The contribution limit for individuals aged 50 or older was increased from $27,000 to $30,000.

- Starting in 2024, any owner or employee who had gross wages/earned income in excess of $145,000 (indexed) in the prior year must designate any age-50 catch-up salary deferral contributions as Roth rather than pre-tax.

- Starting in 2025, the catch-up salary deferral contribution limit will be increased to $10,000 for any participant who was aged 60, 61, 62, or 63 for the entire year (i.e., someone who started the year age 59 or finished the year age 64 would not be eligible for the higher catch-up limit for that year).

- As a reminder, employee contributions need to be made through payroll deferrals.

Roth treatment of employer contributions

- Technically effective starting in 2023, employers may allow employees to have employer contributions designated as Roth. For practical purposes, however, this provision will be difficult for employers and service providers to implement, so further guidance is expected.

- This announcement should put to rest the concerns that the US Government is looking to minimize savings in Roths. After all, the utilization of Roths accelerate the taxation of retirement dollars and helps to fix the national budget sooner than later.

RMD changes for retirees

The US Government is addressing longer life expectancies by pushing back required minimum distributions known as “RMDs.” RMDs previously started at age 70.5 and will now slowly change to age 75 in 2033.

Required minimum distribution (RMD) beginning age:

- Starting in 2023, the RMD beginning age is increased to 73.

- Starting in 2033, the RMD beginning age will be increased to 75.

This deferral of the starting age of RMDs does not preclude retirees from accessing their retirement. It does, however, afford clients greater ability to defer the start of their withdrawals or consider Roth IRA conversions in lieu of RMDs.

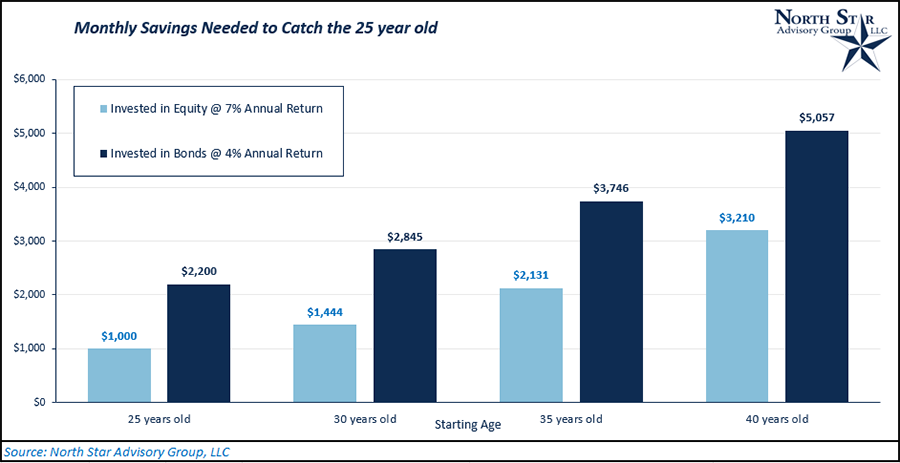

Cost of waiting

For savers, compounding interest has famously been coined the “8th wonder of the world.” Given a long-term investment horizon, the effects/importance of compounding are magnified. The earlier a person begins investing, the more they will benefit from compound interest. This month, we analyze the “cost of waiting” to save between those who start their investing journey early in their career, to someone who delays their savings.

To illustrate the cost of waiting, we begin with a 25-year-old who invests $1,000/month for 40 years (ending at age 65) in all equity. Using an average annual return of 7% for equities, this person could hypothetically have $2.6 million at age 65. The $2.6 million figure is now the target for our other scenarios where we asked the question, “how much must you save monthly to reach $2.6 million dollars given a starting age of 30, 35, and 40 with an average annual return of 7%?” In the chart below, we can see the cost of waiting.

The market volatility of 2022 has caused many investors to consider avoiding the volatility of equities and investing 100% in bonds and CDs. For this group, we added a second scenario where people at each starting age invest solely in bonds at a hypothetical return of 4%.

What does this mean in totality, compared to the 25-year-old, assuming we are investing in all equity @ 7%?

- The 30-year-old ends up contributing $126,000 more than the 25-year-old over 35 years to reach $2.6 million.

- The 35-year-old ends up contributing $287,000 more than the 25-year-old over 30 years to reach $2.6 million.

- The 40-year-old ends up contributing $482,000 more than the 25-year-old over 25 years to reach $2.6 million.

Clearly, the cost of waiting significantly increases the amount that will be needed to be saved monthly to reach the intended goal. Savers also miss another important factor. If you were not able to create a savings pattern of a smaller figure in your younger years, it becomes even harder to create a larger savings pattern in the future. Oftentimes, the money that should have been going towards savings ends up being spent on lifestyle expenses that never go away.

Where will the equity markets go next?

To wrap up the month, we take a snapshot of major US index ETFs as of January 27. Tax loss harvesting temporarily pushed markets down at the end of 2022 and they have rebounded sharply to start of 2023. It's green across the board when it comes to 50 Daily Moving Average (DMA) spread, 5-day change, and YTD change. The Nasdaq 100 ETF (QQQ) is in the lead on a YTD basis with a gain of 10.1%, and it's also up the most over the last five days and the farthest above its 50-DMA. This is the opposite of what we saw in 2022 when QQQ lagged the rest of the market severely. Thirteen ETFs tracking different major US markets are now "overbought" based on short-term technical indicators with the exception of the Dow 30 ETF (DIA) coming close to joining this group as number 14.

Even though the S&P 500 is overbought, its 10-day advance/decline line is in neutral territory, which provides at least a little more breathing room for potential further gains in the very near term before we'd call this market over-extended.

While "growth" has gotten off to a hot start to 2023, this area of the market is still a long way away from prior highs. Value, on the other hand, is getting remarkably close to new highs after another push higher this week. The S&P 500 Growth ETF (IVW) is still 27% below all-time highs, but the S&P 500 Value ETF (IVE) is just 3% from a new all-time high.

It is important to remember that the U.S. equity market will continue to be driven by earnings growth/contraction. For 2023, growth stocks have moved the largest based on a combination of speculation and falling interest rates. Even if The Federal Reserve slows down their rate hikes, further stock prices appreciation from falling interest rates will likely not be a long-term driver of returns. Going forward, it will continue to be important to buy companies with strong cash flow and solid business models.

While we expect a bumpy market for the next few months as companies work through excess inventories, we do not expect that we will test the 2022 lows anytime soon. In fact, many of the larger bears on Wall Street and in the fund companies that we work with are starting to turn positive on the global economies. China is opening up, which may lead to a wave of Chinese travel and consumption. China’s reopening has led to a massive speculative rebound in their market, which has put China solidly into an over-extended valuation. Due to a warmer European winter and large shipments of fuel from the US, the energy crisis is not as severe in Europe. In fact, Germany has excess gas supplies right now.

We are passionately devoted to our clients' families and portfolios. Contact us if you know somebody who would benefit from discovering the North Star difference, or if you just need a few minutes to talk. As a small business, our staff appreciates your continued trust and support.

Please continue to send in your questions and see if yours gets featured in next month’s Timely Topics.

Best regards,

Mark Kangas, CFP®

CEO, Investment Advisor Representative