Each month we ask clients to spend a few minutes reading through our newsletter with the goal of raising their investor IQ. In honor of 529s, this month we focus on is college savings and planning.

- 9 amazing advantages of 529 plans

- Student loan payment pause extended to Aug. 31

- Unlocking scholarships with the ACT

- Fresh start for student loan defaults

- GDP Reading 401

- Where will the equity markets go next?

9 amazing advantages of 529 plans

Many families don’t realize that saving for college and not utilizing a 529 plan as part of the planning could be a very costly mistake. A 529 plan is a tax-advantaged savings plan designed to encourage saving for future education costs. All fifty states and the District of Columbia sponsor at least one type of 529 plan. Even though 529s have been around for 26 years, many families are not aware of the following 9 amazing advantages of 529 plans.

- College savings grow tax-free.

- Long-term compounded growth is something investment people get excited about. It basically means the money you made is making even more. In short, you’re crushing it. And when that growth is tax-free, you aren’t giving a chunk of it back every year. Even better.

- Withdraw your savings tax-free for “qualified expenses.”

- When it’s time to use the money in your 529 Plan, it stays tax-free as long as you use it on qualified educational expenses. Don’t worry, it’s all the big stuff: tuition, fees, room and board, books, supplies, computers, and more.

- A 529 account can be used for whatever comes after high school, including four-year universities, community colleges, trade, technical, or vocational schools, certificate programs and apprenticeships.

- As of 2018, $10,000 per year can be used towards tuition expenses at elementary or secondary public, private or parochial schools.

- Potential state tax deduction.

- Some states offer an incentive for savers to use their instate plan. For example, if you’re an Ohio taxpayer who contributes to Ohio’s 529 plan, you’re eligible for a state tax deduction every year you contribute. The current deduction is $4,000 per child, per year. Yes, you can put in way more than that to get tax-free growth and then take the state deduction in $4,000 chunks in future years. Occasionally it makes sense to make contributions to other state’s 529 plans. While those contributions are not deductible on your state return, the deductions can be recaptured when you roll the assets into your respective state plan.

- Dozens of low-cost investment options from leading financial firms.

- Each state sponsors different investment options for their respective 529 plan. Some options have extremely low-cost options, while other options have high internal expense to compensate advisors. Each state offers options for every comfort level when it comes to risk, occasionally FDIC-insured tax-free bank accounts maybe available.

- NSAG does not charge a fee or receive compensation for assisting with 529 plans. It is one of the many ways that we give back to our clients.

- $25 minimum deposit, no annoying fees.

- The idea is to make this a plan for all, so it only takes $25 to start or add to a 529 Plan. Beyond that, most plans don’t charge annoying fees — like so-called “low balance fees” – that penalize people for trying to do the right thing.

- Don’t worry about hurting your child’s chances for future scholarships or grants.

- 529 Plans are intended to be part of the big picture of covering higher education, which typically includes savings, financial aid, and student loans. When kids are nearing the end of high school and you start calculating what’s called “Expected Family Contribution,” you’ll be happy you saved in a 529 Plan because if parents own the account, only 5.64% of the account value is considered in that calculation. So yes, this is how you save and max-out student aid.

- In contrast, if you saved money in the child’s name in a bank account, savings bonds or UTMA, 20% of these accounts are considered in the financial aid calculation.

- Flexible options if your child doesn’t need or use the money.

- A parent typically owns the account. A child is the beneficiary. That means you call all the shots. If one child doesn’t need or use the 529 account, simply transfer your savings to another eligible family member, use it for your own education, hold it for future use, or withdraw the money. With this last option, you would be taxed on the earnings and the IRS would assess a 10% penalty on the earnings of the plan.

- No age or income restrictions.

- You can start a 529 Plan for any aged child. You can start one for your own continuing education. You can be a parent, grandparent, or another family member. Your income can be at any level.

- 529 Plan is easy for grandparents, aunts, uncles, cousins, even friends to use.

- We hear it a lot — “I want to be a positive part of my grandchild’s life … I want to give opportunities, not just toys.” a 529 Plan can be an important part of your plans, whether you want to make an occasional gift or own the account and build a substantial 529 plan.

- NSAG even has gift certificates that we can provide for various occasions so you can let them know of your generous gift.

Student loan payment pause extended to Aug. 31

Like clockwork, Federal student loan payments have been paused again and will not resume until at least August 31, 2022. With the new deadline just a few months before the November mid-term elections, we are likely to see yet another extension announced later this year. With politicians only in session a few days at yearend, a further extension would likely push the next restart date into early 2023.

Borrowers on an income-based repayment program are benefitting the most from these delays. For these plans, a payment in forbearance is considered as a payment made. With most repayment programs on a 10-year repayment plan, many of these borrowers have already seen approximately 20% of their payments forgiven.

Borrowers not on an income-based repayment program are receiving an interest free period to use the payments for other purposes or pay down student loans faster.

Washington is continuing to review and address loans of concern. The additional payment delays are providing Washington the necessary time to address loans that need to be fixed. At the end of April 2022, Washington announced another 40,000 loans would be eligible for discharge under the Public Service Loan Forgiveness program and 3.6 million more will move closer towards forgiveness due to student loan servicers who pushed borrowers into unnecessary interest-accruing forbearance. This is just one of many significant announcements to address student loans in the last few months.

The last few days of April 2022, President Biden announced that he is starting to look at student loan forgiveness. He hinted that he will not be going as high as $50,000 in forgiveness and will likely stay closer to his original campaign goal of forgiving $10,000 of federally backed student loans. We also heard for the first time that eligibility may be limited to those under certain income thresholds. The situation remains fluid and we will wait for definitive forgiveness plans from Washington.

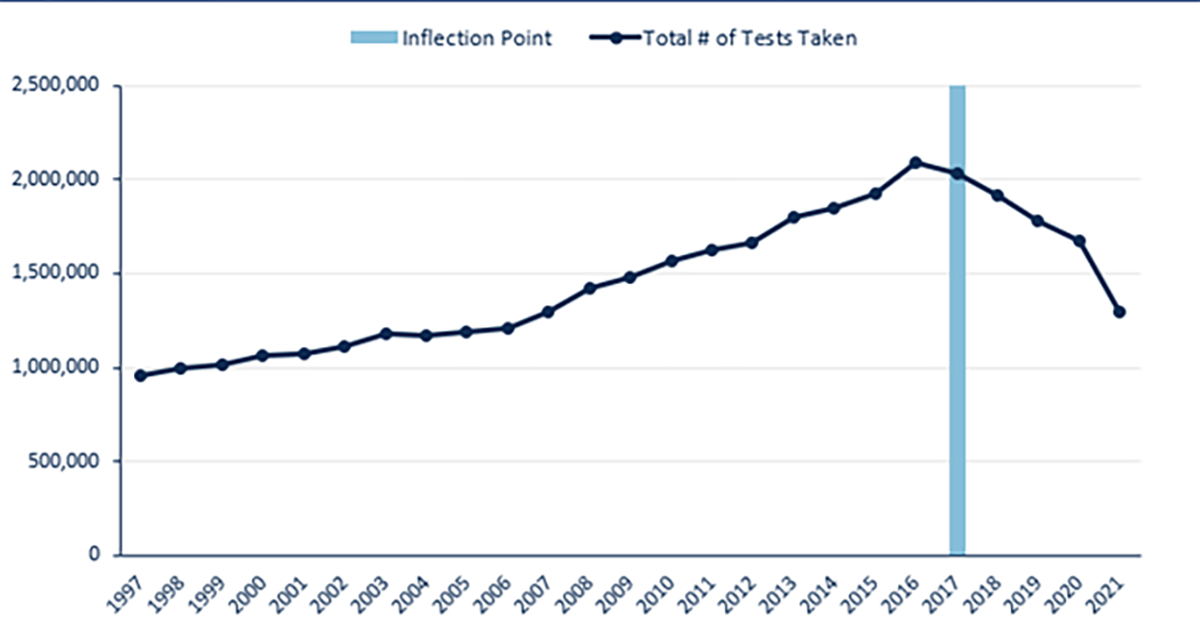

Unlocking scholarships with the ACT

Many universities are struggling to maintain attendance and have dropped the ACT and SAT scores from their admissions requirement. In response, students are electing to not take the ACT and SAT and it may be reducing their eligibility for merit scholarships. From our initial conversations, many families are not aware that universities have merit scholarships that have an ACT and/or SAT score requirement. Therefore, skipping these tests may immediately reduce the amount of potential aid that a student could be eligible for. Ironically, the odds of getting aid are actually climbing for those who do well on the tests for three reasons:

- Compared to 2017, there has been a 2% population decline for 15–24-year-olds.

- Compared to 2017, when more than 2 million students took the ACT, the 2021 number represents a 36% cumulative decrease, equal to 735,000 fewer students taking the test. 32% of the ACT-tested graduating class took the standardized exam more than once in 2021, compared to 41% for the 2020 cohort.

- The students who took the test in 2021 also got worse scores compared to 2020.

In 2021, NSAG invested in a database that allows us to easily search and compare which of the 3,500 US colleges will offer your family the most financial aid and scholarships. This tool also unlocks personalized estimates for colleges on your list and provides support for negotiating offers so you can maximize the aid you get and minimize student debt. Even if a college has been selected, the tool can help to uncover scholarships that students were unaware of. As part of our NSAG Cares program, we offer this resource at no cost to our clients.

.png)

.png)

Fresh start for student loan defaults

Roughly 25% of student loan borrowers or 10 million people are estimated to be in delinquency or default. In April, the Education Department said these borrowers will be granted, “a fresh start on repayment by eliminating the impact of delinquency and default and allowing them to reenter repayment in good standing.”

GDP Reading 401

On April 28, 2022 the US Gross Domestic Product (GDP) for Q1-2022 was released with a quarter-over-quarter decline of 1.4% compared to forecasts of a 1% increase. While initial reaction to the headline number should cause concern, we investigate the details of the GDP to show the underlying strength in the economy.

- Inventory reductions deducted 0.84% after adding 5.32% points last quarter. This line-item alone accounts for a 6.16% reduction in GPD quarter-over-quarter. Businesses do not have a problem of too much inventory, they still have a problem of getting inventory. This problem is being pressured further by China’s city-wide lockdowns. China currently has almost as many citizens under lockdown as the entire population the United States.

- Trade exports declined by 0.68% after a 2.24% increase in Q4-2021. This deficit heavily dragged down the GDP number by 2.92%. This impact is likely temporarily influenced by disruption in Europe due to the Russia/Ukraine war and the zero tolerance lock down policies in China. China’s lockdowns have caused backlogs in shipping at their ports that dwarf prior delays off California’s coast.

- As for other important economically cyclical parts of output, autos and fixed investments (particularly non-residential through equipment) both saw notable improvements.

- As we expected, consumer demand grew 1.83% vs 1.76% in Q4-2021 showing a much healthier picture in spite of higher commodity prices. Services contributed 1.86% up from 1.48% in Q4-2021 to counteract weaker non-durables. Durable weakness was mostly a story of gasoline and energy weakness surging prices tamping down demand.

Russia, China and The Fed are putting pressure on the markets and the global economy. An improvement in any one of these could end the current downturns. China may be the first to get resolved. Even with a removal of the lockdowns in China coming soon, president Xi Jinping may not be able preserve another reelection.

Chinese state media reported details on Friday April 29, 2022, that the country is promising policy changes that are more supportive of the economic growth. This change may lead to a shift of a zero-tolerance policy to one of greater flexibility. While Chinese equities rebounded significantly on the news, more time will tell of the country follows through.

As we primarily touched on just Q1-2022’s GDP numbers, we plan on diving much deeper into GDP, businesses cycles, recessions, and much more in June’s addition of Timely Topics.

Where will the equity markets go next?

April was a brutal month and may lead to a strong May. It is likely that various markets have over corrected in the short-term. Before we look forward, lets recap where the year is so far.

.PNG)

We continue to see significant pullbacks focused in areas of speculation and those impacted the most by rising interest rates. The continued rotation from growth to value is likely to continue for at least the next year and is picking up steam as interest rates rise in connection with either COVID variants slowing down, rising inflation, or both.

Even with the risk of Ukraine and rising sanctions, there continues to be a small risk of a recession in the next 18 months. As discussed above, we could technically experience a light recession will still having a strong consumer. The Federal Reserve is prepared to speed up or slow down rate hikes when necessary, and consumers currently have strong balance sheets. Current trend is for The Fed to speed up. As a reminder, a recession is approximately six months of negative GDP. Even with The Fed speeding up rate increases, a few economists are starting to forecast a recession.

We still believe we are in a secular bull market, which started in 2010 and typically lasts around 15-20 years. However, this secular market is likely to last longer due to a slow start in 2010-2013.

Jamie Dimon, JP Morgan’s CEO provided the following commentary during the company’s Q1-2022 earnings call on 4/13/2022:

We are passionately devoted to our clients' families and portfolios. Let us know if there’s somebody who would benefit from discovering the North Star difference, or if you just need a few minutes to talk. As a small business, our staff appreciates your continued trust and support.

Please continue to send in your questions and see if yours gets featured in next month’s Timely Topics.

Best regards,

Mark Kangas, CFP®

CEO, Investment Advisor Representative