Each month we ask clients to spend a few minutes reading through our newsletter with the goal of raising their investor IQ. This month we focus on our best gifts for the holidays.

- Gratitude

- Perspective on Omicron

- Strong Economy

- Time in the market

- NSAG Rewind

- Where will the equity markets go next?

Gratitude

The last few weeks and months have had a lot of stress and uncertainty.

So, instead of starting off writing about politics, or the economy, or the supply chain, I figured I'd change the script and write about something completely different. Let's talk about gratitude.

Is gratitude a practice for you? In my many roles as a husband, father, friend, business owner, mentor and financial professional, I'll tell you that it should be.

Why? Gratitude reminds you of what really matters. Not the lines at the store. Not the traffic. Not what happens on Capitol Hill or Wall Street. But, what really, truly matters.

I am deeply, abundantly grateful today. For the food in my fridge. For the roof over my head. For my health. For my circle of family and friends who love me. For my community that has given me a home. For my amazing clients and partners who have helped build a thriving practice that can provide for many families. I'm grateful for you.

By taking inventory of all the things we are grateful for allows us to get through the minor irritations and helps us reset when something major happens. Gratitude calms when things get stressful and overwhelming.

It can be extremely satisfying repay your gratitude via donations of time, resources or financial support to the areas in your life in which you are grateful.

Personally and professionally, we have continued to repay our gratitude throughout 2021 and we are developing additional ways to expand our gratitude in 2022. We encourage many families to sit down over the holiday season to do the same. Please let us know if you have any questions or if NSAG can help guide your family’s gratitude repayment.

Perspective on Omicron

Let’s talk about omicron. No, not the Transformer toy on my son’s Christmas list, the new COVID variant.

Since the first known cases of COVID-19 were detected in China, we've seen a number of notable mutations as the virus moved across the world. Some, like beta and gamma, didn’t end up being a huge deal. Others, like delta, spread rapidly and caused new waves of infection.

Now we have another variant on our hands: Omicron. And it could be a serious one. Unsurprisingly, markets reacted badly to the news on Friday, November 26, and gave us our worst market day for the year. Why? The short trading day and lack of overall volume over the holiday break gave the selling pressure greater impact on the market than it might have had under normal conditions.

We’ve seen that pattern before and it’s worth remembering that bad news over a holiday often leads to outsized market reactions.

Is Omicron dangerous?

Well, we don't know yet. And we won't know for several weeks until scientists can determine how the variant will respond to current vaccines and treatments. If it's more virulent, it could have delta-level impacts on travel, hospitality, and other parts of the economy. It could also turn out to be a tiny bump in the road. We just don’t know yet. The market is laser-focused on Omicron news so we can expect rocky times until the uncertainty clears (or something else takes over the chatter).

Vaccine manufacturers have stated that they can produce modified vaccines in roughly 100 days to address new variants when/if needed. Therefore, those in search for new vaccine protection will need only need to wait a short time. Those who are not concerned about vaccine protection will continue to go about their business as usual.

So, what can we do?

Rather than try to predict the unknowable or speculate wildly without enough information, let's do something else instead. Let's take a deep breath, step back, and focus on some ground truths: everyone is tired of this pandemic and ready to move on. But the pandemic's not done yet. COVID has never left and we will continue to see COVID variants. Most will fade into the background. Some will be more serious. New vaccines and treatments are continually being developed and released. We have been adapting to the virus for nearly two years and we'll continue to get better at it.

Strong economy

While we can’t predict exogenous shocks like COVID, it seems reasonable to forecast either slowly or slightly faster declines in unemployment over the next couple of years. Strong employment means any further pullback in consumer confidence is likely to be driven by inflation continuing to accelerate.

The good news is that further major increases in headline Consumer Price Index (CPI) are going to require a major new advance in commodity price indices that are trading at roughly the same level as April (for agriculture) and June (for energy). If prices stay at their current level for the next year, headline inflation rates year-over-year would likely crater. Falling CPI would allow the Federal Reserve to increase rates at the lower end of their anticipated speed of increases. Stable or falling CPI makes a recovery in consumer confidence over the coming several quarters likely, and suggests consumer confidence declines are not an indication of a slowing economy.

The data from ISM for the first week of December showed that growth is not the problem for the US economy at the moment, even if there are other challenges. Two important indices (prices and delivery times) within manufacturing and services did not make a new high, suggesting there’s some room for optimism that the supply chain mess and price pressures are in the process of peaking.

Lower unemployment, slowing inflation, recovering consumer confidence and a growing economy all set the stage for an economy that can offset measured rate increases from the Federal Reserve.

Time in the market

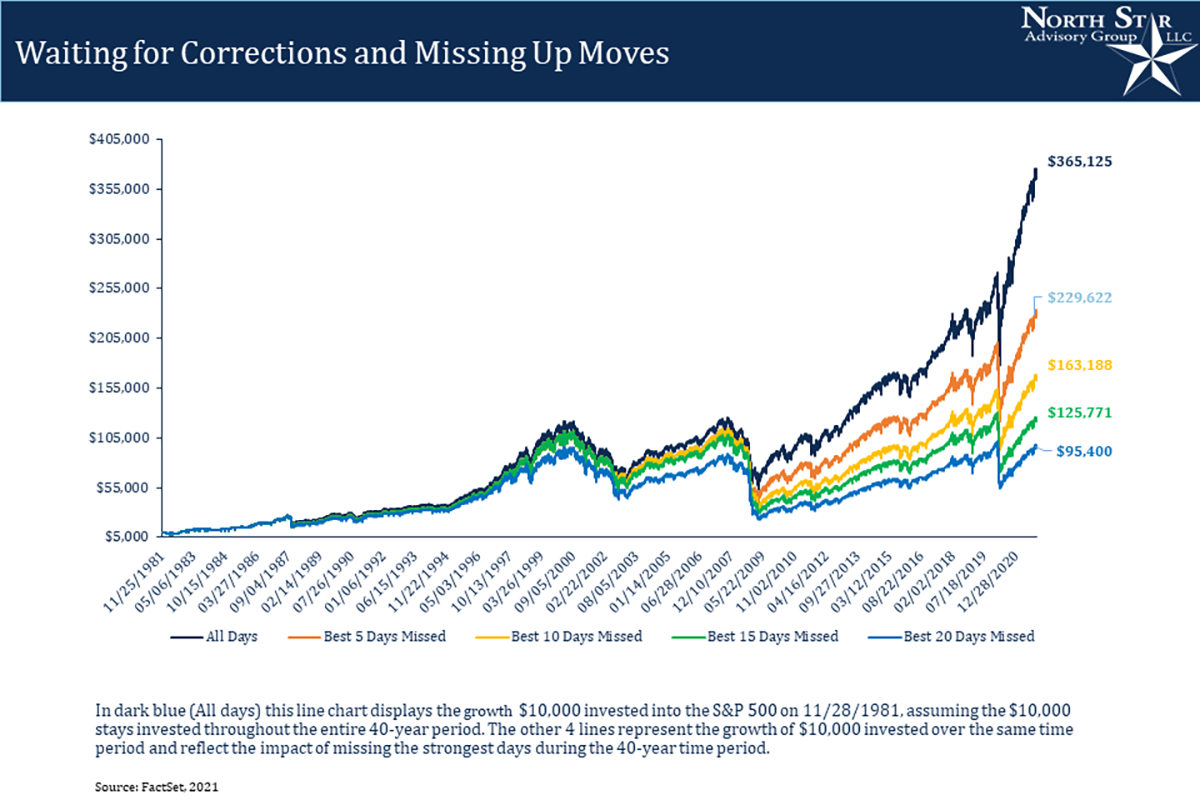

Clients are asking more frequently than ever if “it is time to get out of the market” or “should we raise cash since there will be a correction?” Our research continues to support that ‘time in the market’ is much more valuable than ‘timing the market.’ While the market won’t have positive returns every single year, historically, there are more positive months and years than negative ones. Timing the market perfectly on a consistent basis is virtually impossible, and when attempting to do it, you are most likely missing out on some of the best days in the market and the 8th wonder of the world… compounding returns. This month we provide a few different perspectives on how impactful it is to miss a few of the best days.

This first chart below illustrates the damage that can be caused by attempting to time the market. $10,000 dollars invested in the S&P 500 40 years ago (and never touched) would now be worth over $365,000. If you miss 5 of the best days while waiting for a correction, your account value would be worth 37% less or ~$135,000. As you continue to miss 10, 15, and 20 of the best days, your account’s value would be worth even less.

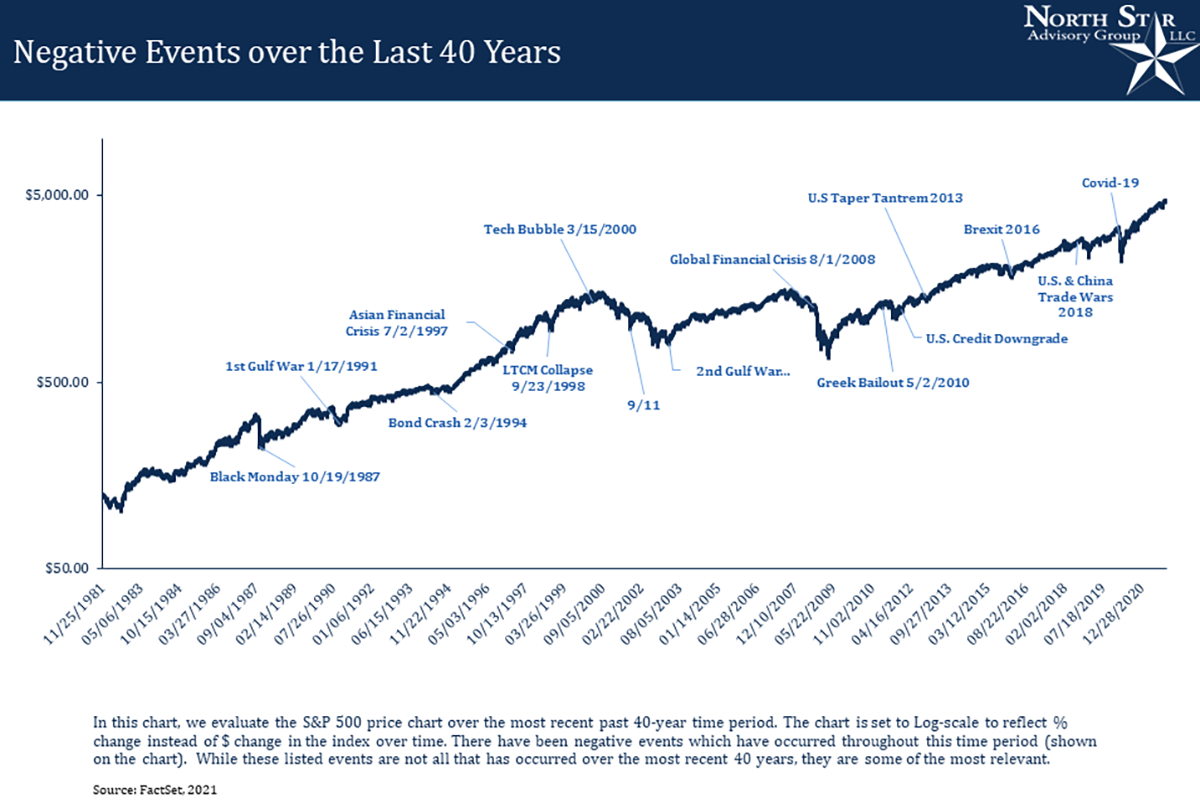

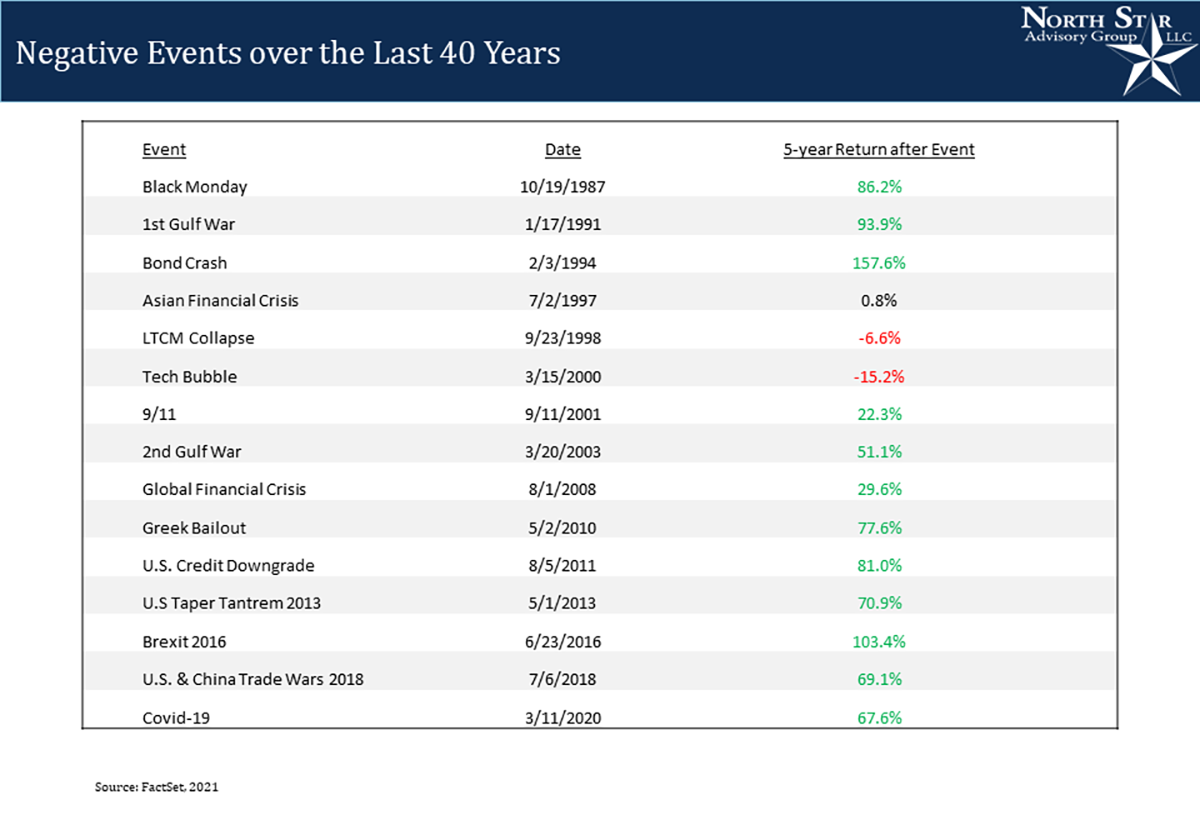

Over the same 40-year period, we’ve experienced many negative events that have impacted the markets and worried investors. While these events have caused short-term market volatility, long-term strength prevails almost every time.

Generally, we build our client’s portfolios so they can take at least 3-5 years of withdrawals from non-stock positions. In the following table below, we display the 5-year return after each of these events. You can see that even if you had the unfortunate timing of buying before the date of each of these major events, the S&P 500 was positive 13 of the 15 periods.

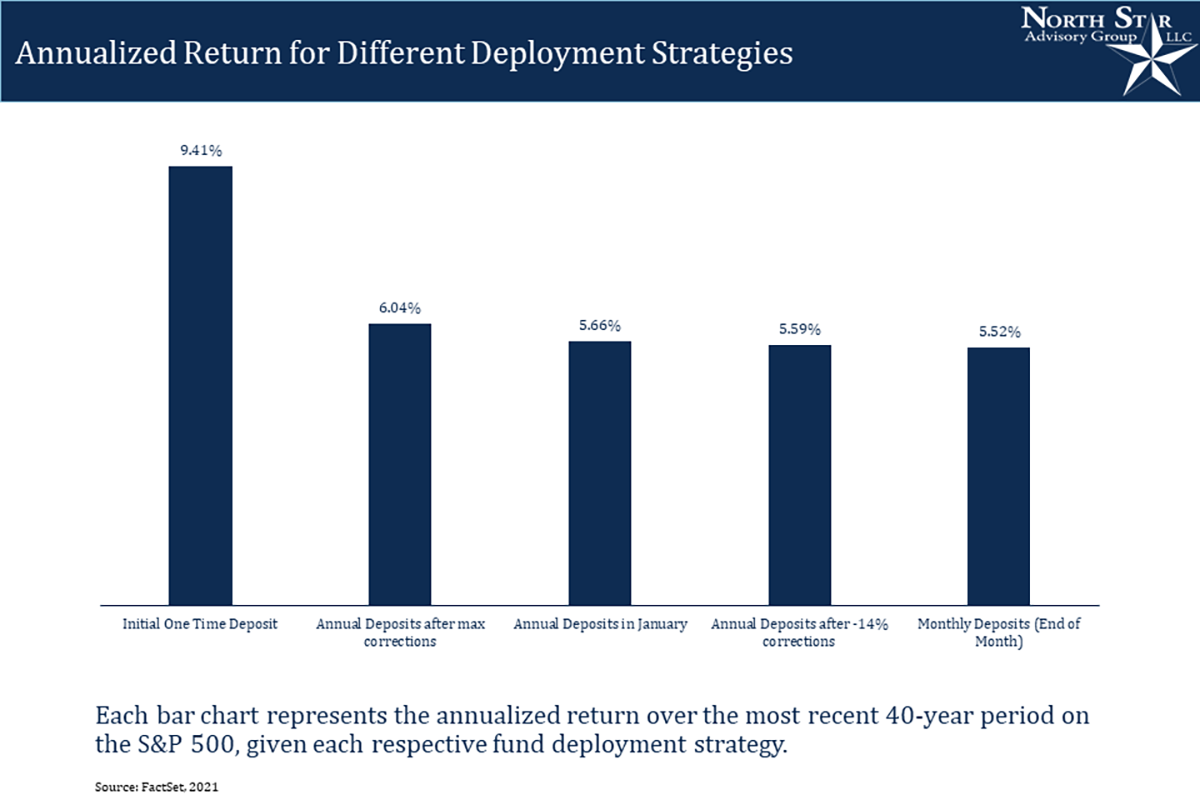

While it may seem simple, there is a reason that Dollar Cost Averaging helps to remove the emotion from investing. In the chart below, we’ve modeled out various scenarios in which an investor might deploy their money into the S&P 500. After modeling these scenarios, we’ve calculated each deployment strategy’s annualized return.

The first bar illustrates a 9.41% annualized return for investing $240,000 into the S&P 500 40 years ago and riding the emotional roller coaster. The second bar of 6.04% is produced by impossibly making annual deposits of $6,000 over 40 years straight years exactly the day after the worst decline in each year. Third best return of 5.66% is produced by making annual deposits each January. The fourth best return is produced by making virtually 40 consecutive impossible annual deposits after either a 14% drawdown each year or catching the day after the worst annual drawdown if the annual decline was less than 14%. Finally, we evaluate making monthly deposits of $500 for 40 years.

One-time upfront returns do better over time versus annual deposits due to additional time in the market. Annual deposits produced a greater return compared to monthly deposits due to additional time in the market. Not only is trying to time the market virtually impossible and extremely stressful, even 100% perfect timing did not produce significantly better returns.

NSAG Rewind

The first week of December scared many investors into thinking another larger crash was coming. In July, we wrote that investors should Expect more days like July 19, 2021 and that is exactly what December brought us. Short-term irrational trading brought out rational fear and helped to balance fear and greed in the markets. Let’s take a look at where we stand year-to-date compared to what we should be seeing with average downside volatility days. The following data is available in NSAG’s November 2021’s Raising your Investor IQ on page 35.

| S&P 500 | Average | 2021 |

| -1 to -1.5% | 14 | 10 |

| -1.5 to -2% | 8 | 4 |

| -2% to -2.5% | 4 | 4 |

| -2.5% to -3% | 2 | 1 |

| < -3% | 2 | 0 |

Where will the equity markets go next?

The US consumer remains strong yet struggles to complete many of the purchases they desire. This strength should limit any potential pullbacks into focused areas of speculation and those impacted the most by rising interest rates. The continued rotation from growth to value is likely to continue for at least the next year and should pick up steam as interest rates rise in connection with either COVID variants slowing down or rising inflation.

There continues to be virtually zero risk of a double-dip recession and the Federal Reserve is prepared to speed up or slow down when necessary. We still believe we are in a secular bull market, which started in 2010 and typically lasts around 15-20 years. However, this secular market is likely to last longer due to a slow start in 2010-2013.

We are passionately devoted to our clients' families and portfolios. Let us know if you know somebody who would benefit from discovering the North Star difference, or if you just need a few minutes to talk. As a small business, our staff appreciates your continued trust and support.

Please continue to send in your questions and see if yours gets featured in next month’s Timely Topics.

Best regards,

Mark Kangas, CFP®

CEO, Investment Advisor Representative