Each month we ask clients to spend a few minutes reading through our newsletter with the goal of raising their investor IQ. May's edition of Timely Topics touches on recent concerns within the private credit space and focuses on trending themes in the capital markets that are blurring the lines between investing, speculating, and gambling.

- Credit concerns

- Sports gambling

- Gambling on IPOs

- Prediction markets

- 529 Month

- Where will the stock market go next?

Credit concerns

In the wake of 2008’s housing and global financial crisis, the Dodd-Frank Act (2010) was implemented across the banking sector. This act forced banks to tighten their capital requirements, restricted a lot of proprietary trading, and held higher quality assets on their balance sheets. These new regulations forced banks to pull back much of their private lending, leaving a gap in the market for many private middle market companies that needed capital. In recent years, large asset managers such as Blackstone, KKR, and Apollo, to name a few, have stepped in to fill this lending gap.

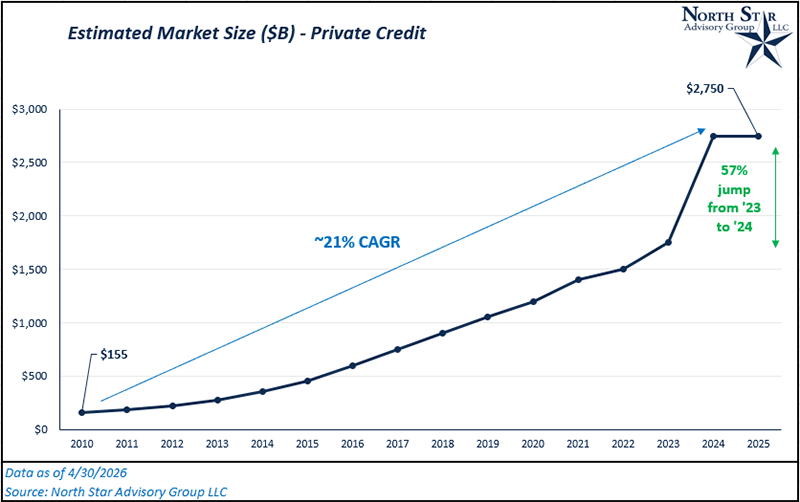

From 2010 through 2025, it is estimated that the private credit increased 17-fold in size. This is an annual growth rate of ~21% per year, making it one of the fastest growing segments in capital markets over that time frame. Note that the market size is an estimate as different firms classify “private credit” differently, so there is some nuance in the range of numbers. We used the mid-point for simplicity.

Private credit refers to loans made directly by non-bank lenders to companies, typically outside of the public bond or syndicated loan markets. These loans are often extended to middle-market businesses and are structured with floating interest rates and higher yields to compensate for lower liquidity and higher risk.

Recent worries about private credit focus on weakening underwriting standards due to increasing capital inflows. With large asset managers under pressure to deploy capital, lenders have increasingly extended credit to weaker, more highly leveraged borrowers, often with looser covenants and a growing reliance on structures like payment-in-kind interest. At the same time, some portfolios have become heavily concentrated in software and IT services companies, which tend to have recurring revenue but can be vulnerable to valuation resets and slower growth, particularly if they are vulnerable to AI disruption. Because these loans are privately held and subject to less regulatory oversight than public markets, they are also not marked-to-market in real time. This can delay the recognition of losses and create a smoother, but potentially misleading, picture of performance. While many of these products have generated ~10-12% annually in recent years, those return profiles may not be sustainable going forward, especially if capital growth slows or even declines.

If these products experience net outflows, asset managers may need to sell holdings to raise cash, leading to price discovery. For instance, a fund that lent $100 to an IT firm now facing AI disruption might only find buyers at a steep discount due to higher default risk. To manage withdrawal risk, private funds usually cap quarterly withdrawals at 5% of assets. This limits mass liquidation but doesn’t change the underlying loans’ intrinsic value.

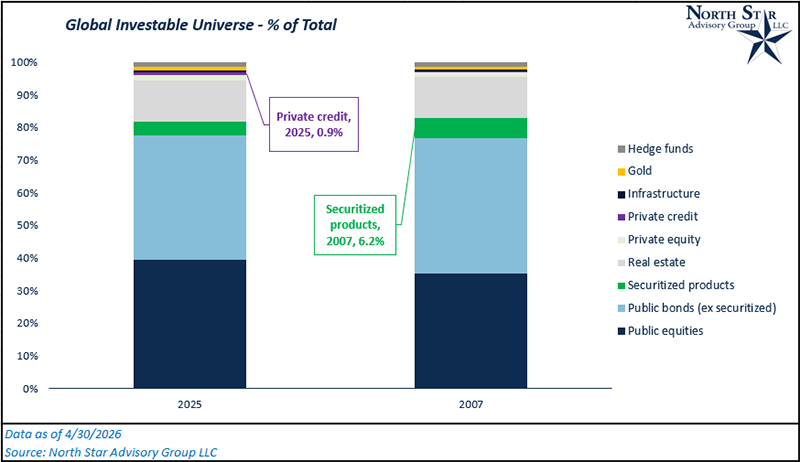

If private credit loans have intrinsic value issues, how much could this affect broader capital markets? Given its smaller size compared to other asset classes, it likely isn't a systemic risk as of now. As of 2025, private credit is less than 1% of the global investable market. In 2007, securitized products (which had major intrinsic value issues), were ~6.2% of the global investable universe.

Sports gambling

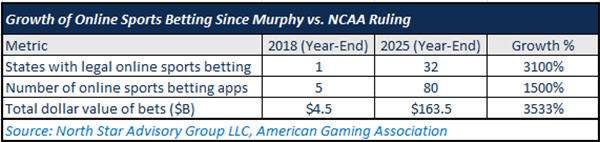

To analyze the impact that online sports betting is having on the broader economy in 2026, we need to rewind the clock to 2018 and provide context behind how large this space has grown to in the U.S. On May 14th, 2018, the Murphy vs. NCAA supreme court decision struck down a federal law prohibiting most states from authorizing sports gambling. The ruling reshaped the legal landscape of sports betting and reaffirmed constitutional limits on federal control over state policymaking.

As you can see from the table above, the online sports betting market has exploded since this ruling struck down federal control over state policymaking in regard to sports betting. Early adopters of legalization from the state perspective were banking on economic growth from legalization. In reality, the impact on consumer spending is more than outweighing any new job creations from the industry. Based on publicly reported data from state regulators and aggregated by the American Gaming Association, sportsbooks retain roughly 5% to 10% of all wagers nationally. In practical terms, that means the average bettor receives back about $90 to $95 for every $100 wagered in the long run. If you apply the midpoint of this loss rate to the total dollar value of bets, that equates to a $12.3 billion loss to consumer purchasing power in aggregate in 2025 (7.5% x $163.5 billion)[MK2.1].

In the context of the broader U.S. economy, that lost purchasing power would only equate to ~0.06% of total consumption annually. Consumption represents ~68% of annual GDP in the U.S and totaled $20.6 trillion in 2025. In the context of the broader economy the lost dollar amount is not very large, but we should still consider that $163 billion (~1% of consumption) is going through these apps (whether winning or losing) and likely staying inside these online ecosystems instead of being spent in more productive areas of the economy.

Most online sports bettors are young men; Statista reports around 70% are male, with about 60% aged 18–34. The annual loss of $12.3 billion is minimal compared to all U.S. consumer spending, but it highlights which group is most affected. This demographic spends more on bars, restaurants, and gaming, so changes in these areas may be worth monitoring in the coming years.

What are the primary benefits of the growth in this industry? While the gaming industry often highlights job creation as a key benefit, data from the American Gaming Association suggests that employment gains tied specifically to sports betting are relatively modest within the broader industry. The AGA reports that the entire U.S. gaming ecosystem supports roughly 1.8 million jobs across casinos, suppliers, and related activities, but this figure is heavily driven by traditional, labor-intensive casino operations rather than digital sportsbooks. Given that online sports betting is highly scalable and requires significantly fewer workers, the incremental job creation from its rapid growth has been limited relative to its economic footprint, reinforcing the view that much of the activity reflects a shift in consumer spending rather than a major new source of employment.

Lastly, and likely most importantly, demographic data shows that sports betting participation is concentrated among younger adults, particularly men, with studies cited by the American Gaming Association indicating that a growing share of bettors fall within the 21–44 age range and engage primarily through mobile platforms. Research in behavioral economics and public health literature further suggests that frequent sports betting is associated with increased risk of impulsive decision-making, higher rates of problem gambling, and elevated stress and anxiety over time. These effects are especially pronounced among high-frequency bettors, where repeated exposure to losses and near-miss outcomes can reinforce harmful behavioral patterns, creating longer-term financial and psychological consequences that extend beyond the initial wager.

Gambling on IPOs

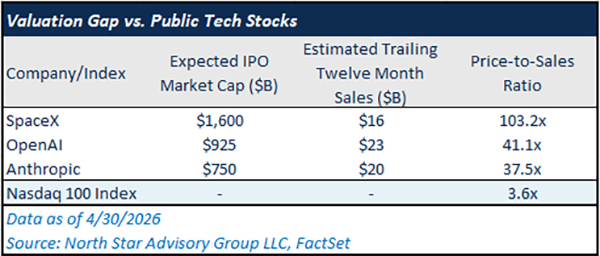

As speculative behavior becomes more embedded in everyday financial activity, it is increasingly showing up beyond traditional gambling platforms and into capital markets themselves. Periods of heightened excitement around new investment opportunities often mirror the same dynamics seen in sports betting, where narratives, momentum, and fear of missing out can outweigh disciplined decision making. With several high-profile companies such as SpaceX, OpenAI, and Anthropic widely expected to draw significant attention if and when they go public, the IPO market is poised to become another arena where speculation can dominate fundamentals. The next section explores how these “lottery ticket” moments have historically played out, particularly for high-valuation technology IPOs.

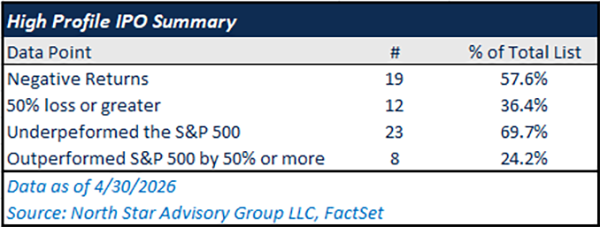

To begin this analysis, we compiled a list of 33 high-profile technology IPOs from 2019-2025 and looked at the buy-and-hold performance from their IPO date through 4/30/2026. A few on this list names include Palantir, Uber, Coinbase, Snowflake, Airbnb, CoreWeave, Rivian, Robinhood, and Reddit, to name a few. Around 75% of the names IPO’d in 2021 or earlier as peak IPO issuance occurred during Covid-era speculation. Lastly, to closely replicate the retail experience with IPOs, we began the performance calculation using each company’s closing price on the day they first began trading.

More than half of these names have had negative returns since they closed on their IPO date, ~70% of the names have underperformed the S&P 500 since their IPOs, and 12 out of 33 have had losses greater than 50%. That being said, 8 out of the 33 names outperformed the S&P 500 by more than 50%. So, while the data shows that chasing these hyped-up names tend to skew towards negative outcomes, you can still find some winners in the IPO market. Strong up-front due diligence is essential, as relying on reputation and hype doesn’t guarantee strong long-term stock returns.

High-profile IPOs often debut with high valuations, making growth and execution crucial for stock performance. Their price-to-sales ratios far exceed those of the Nasdaq 100 Index, justifying higher multiples due to their potential. However, these companies must execute well and achieve profitability to support their valuations and deliver strong returns.

Prediction markets

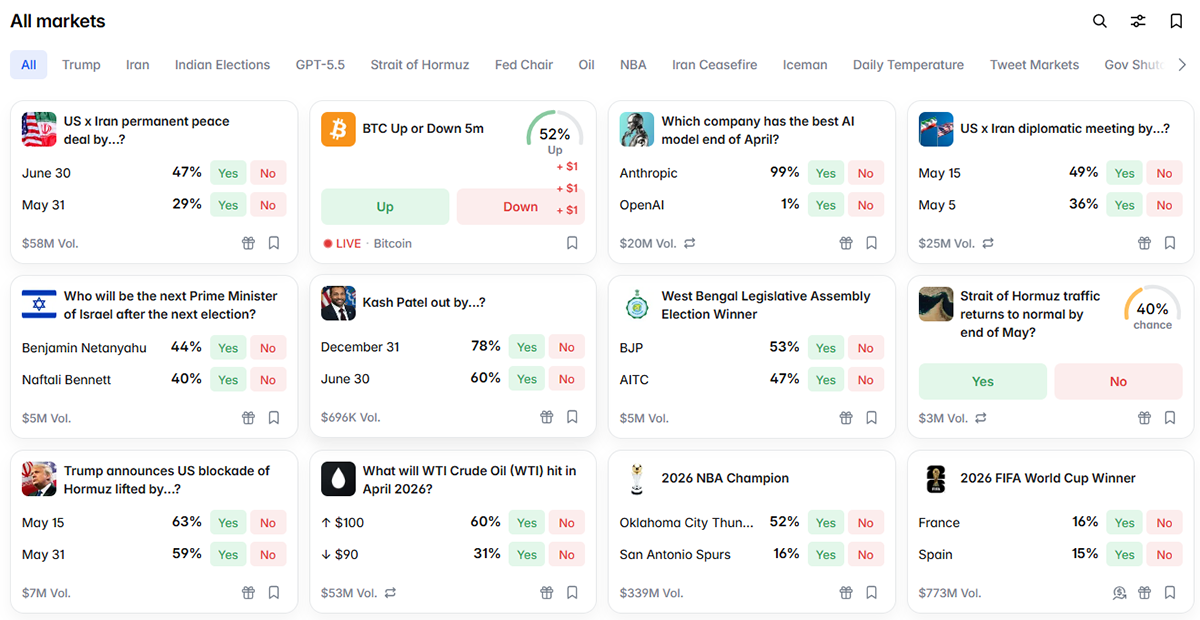

While our previous discussions focused on sports gambling and investing in high-priced blockbuster IPOs, a new type of speculation has emerged, prediction markets, which increasingly challenge the distinction between gambling and investing. These markets have gained widespread acceptance, particularly through platforms such as Kalshi and Polymarket. So, what is a prediction market?

Prediction markets are platforms where participants trade contracts tied to the outcome of future events, with prices reflecting the crowd’s implied probability of those outcomes. For example, a contract that pays $1 if an event occurs might trade at $0.60, implying a 60% perceived likelihood. Platforms like Kalshi and Polymarket have expanded access to these markets, covering everything from elections to economic data releases. While they can aggregate information efficiently (aka; what probability do the masses assign to an event?), they also introduce speculative dynamics that can blur the line between forecasting and betting.

In a real-life example, Brian Duffield recently visited Charleston, SC in March 2026 for a college friend's wedding. Although sports betting is illegal in South Carolina, guests used prediction market apps to place March Madness bets on teams and players. From what he saw, there was virtually no distinction between the two forms of speculation.

The screenshot below shows a popular prediction market platform, where users can speculate on outcomes related to elections, sports, war album release dates, etc. It’s intriguing to see public opinions on these events’ outcomes, but it raises questions about whether users are simply guessing, are making informed decisions on research or have inside information backing their prediction.

Whether you are someone who trades stocks, bets on sporting events, or wants to predict an election in West Bengal, we’d ask the question, “what is your thesis or reasoning behind why your predicted outcome will be correct, or are you just guessing?” Consistently asking yourself this question could help to reduce the blurred line between gambling and investing.

Polymarket.com, 4/27/2026 12:30 AM EST

Recent headlines have brought increasing scrutiny to insider trading risks within prediction markets, highlighting how quickly these platforms are intersecting with traditional regulatory concerns. In one of the most prominent cases, a U.S. Army soldier was charged with fraud after allegedly using classified information about a military operation to place bets on Polymarket, generating over $400,000 in profits in what prosecutors described as the first insider trading case tied to a prediction market. Similar concerns have surfaced across both regulated and unregulated platforms, with reports of political candidates betting on their own elections on Kalshi and regulators warning that individuals with privileged information may be able to exploit these markets.

More broadly, regulators and lawmakers are beginning to treat prediction markets less like novelty platforms and more like financial exchanges, raising questions around enforcement, disclosure, and market integrity. Several states have already moved to restrict participation by government employees, while federal agencies have issued advisories and are evaluating enforcement actions as the market grows. The emerging pattern is clear: as prediction markets scale and integrate into mainstream finance, they are increasingly exposed to the same risks that have long existed in public markets, including insider trading, manipulation, and uneven access to information.

529 Month

529 plans remain one of the most effective tools for college savings, offering tax deferred growth and tax-free withdrawals when used for qualified education expenses. For clients balancing long term financial goals with rising education costs, these plans provide flexibility, control, and potential state tax benefits depending on residency. In addition to traditional college expenses, 529 funds can also be used for K-12 tuition, certain apprenticeship programs, and student loan repayment within limits, making them a more versatile planning vehicle than many realize.

Recent updates under the OBBB have further enhanced the appeal of 529 plans by expanding flexibility around unused funds. Most notably, beneficiaries can now roll over up to $35,000 from a 529 plan into a Roth IRA over time, subject to annual contribution limits and account requirements. This change helps address a common concern about overfunding by allowing excess savings to be repurposed for retirement without penalties or taxes. As a result, clients may feel more confident contributing aggressively, knowing the funds can still support long term financial security even if education costs come in lower than expected.

As part of a broader financial plan, 529 strategies should be aligned with each client’s goals, time horizon, and cash flow needs. Regular reviews, thoughtful contribution strategies, and coordination with other savings vehicles can help maximize outcomes. With continued legislative support and increased flexibility, 529 plans remain a cornerstone of education planning and an important opportunity to create multigenerational financial impact.

Where will the stock market go next?

On April 7th, the U.S. and Iran announced a two-week ceasefire that would allow both parties to negotiate a more permanent end to their war. While negotiations failed over this two-week span, the U.S. announced that it would extend the ceasefire on April 22nd so that negotiations could continue. Despite the ceasefire, control over the Strait of Hormuz remains in question. While the U.S. had claimed a “fully open Strait” was a part of the original ceasefire, Iran rebutted this claim and continued to fire on cargo ships and tankers. On April 13th, the U.S. responded to these developments by blockading Iranian ports within the Strait in an attempt to restrict their oil export ability. Despite the continued volatility in this region, we continue to see signs of deescalation and a path towards continued peace despite the language and talking points coming from Iranian state media.

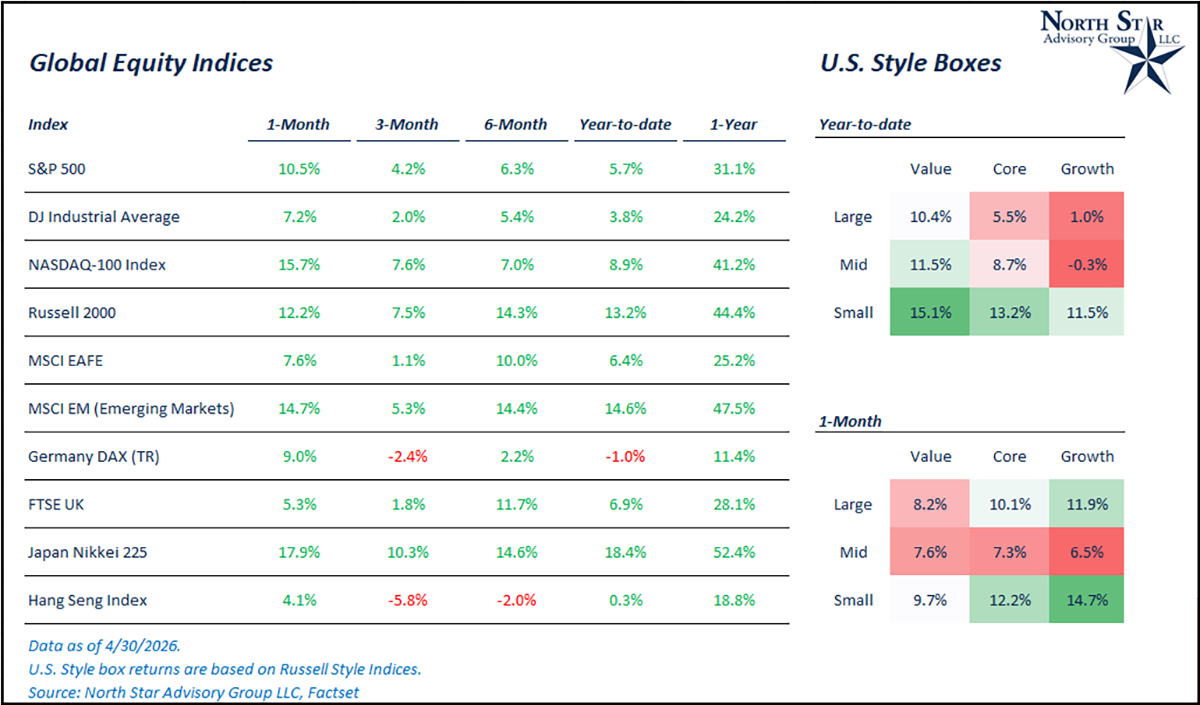

The S&P 500 bottomed on 3/30/2026 and rallied 13.7% to reach new all-time high levels, bringing the index’s year-to-date return to 5.7%. Crude oil prices are still near their highs for the year as the standoff in the Strait of Hormuz continues to limit tanker traffic for the time being. Non-US developed and emerging market stocks had positive months of 7.6% and 14.7%, respectively. Within the broader economy, the semiconductor industry saw extreme levels of strength in April. The PHLX Semiconductor Index was up 38.4% in April. We continue to be constructive, but selective, on the AI infrastructure trade.

In the last week of April, many of the mega-cap technology companies reported their Q1 financial results with mostly positive top and bottom-line results. Additionally, all of the hyperscalers increased their guidance for 2026 capital expenditures related to data center build outs. Increasing guidance on a quarter over quarter basis has been consistent since 2023, and we expect this spend to continue to be a leading indicator for the AI-infrastructure trade.

We are passionately devoted to our clients' families and portfolios. Contact us if you know somebody who would benefit from discovering the North Star difference, or if you just need a few minutes to talk. As a small business, our staff appreciates your continued trust and support.

Keep sending your questions for a chance to be featured in next month’s Timely Topics.

Best regards,

Mark Kangas, CFP®

CEO, Investment Advisor Representative

Brian Duffield, CFA®

Co-Portfolio Manager & Market Strategist