Each month we ask clients to spend a few minutes reading through our newsletter with the goal of raising their investor IQ. March's edition of Timely Topics focuses on theme of AI disruption. Various sectors and overarching macroeconomic trends have been threatened with being upended by AI as the technology improves. We also discuss gold vs. stocks and provided a step-by-step guide to access your tax statements from Schwab.

- SaaSmageddon

- Employment bifurcation

- Electricity

- Safe haven or long-term investment?

- Tax season & 1099s

- Where will the stock market go next?

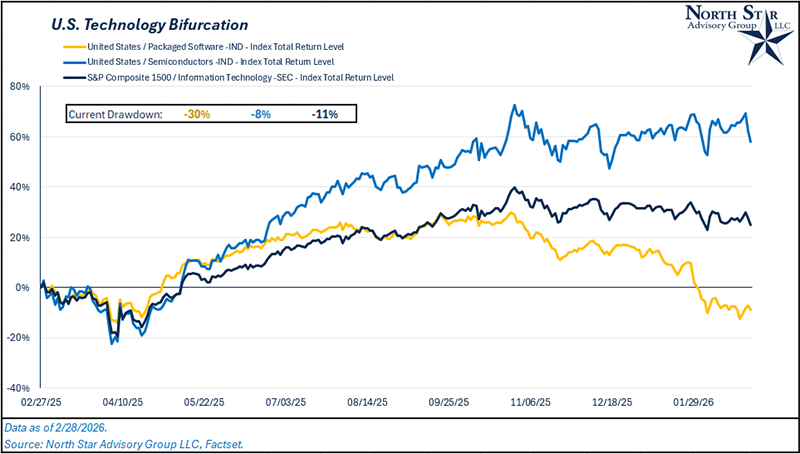

SaaSmageddon

In January 2026, Anthropic, a major AI company, released a suite of new tools and capabilities for its Claude platform. Some of these new tools included plugins for legal, finance, sales, and coding workloads. Users quickly began to recognize the effectiveness of these agentic tools, as they were able to execute multi-step tasks autonomously. One example included a legal plugin that could reportedly automate large portions of routine contract and compliance work. This product rollout marked a major shift in how quickly the AI industry could move from a chatbot to a “digital coworker,” representing the emergence of a true agentic layer.

This realization sparked a sharp selloff in SaaS (Software as a Service) stocks. U.S. software stocks are now down ~30% from from their peak level reached in October 2025. As agentic AI capabilities continue to advance, the market is shifting its stance from “AI will enhance software” to “AI will replace software.” Companies with subscription or seat-based business models are increasingly seen as being under threat from the very technology that was once expected to help them. Over this same period, the semiconductor industry, often described as the hardware or AI “picks and shovels,” has continued to maintain relative strength.

Despite the past few months of negative price action for the software industry, we do not believe the industry’s obituary should be written just yet.

On one hand…

- Many simple logic-based SaaS products will become commoditized by AI agents

- Professional-services automation will continue to accelerate

On the other hand…

- AI is only as good as the data the models are trained on

- Workflow infrastructure is still needed for agents to work through their automation process

- Proprietary data will likely become even more valuable for AI generated insights

Software categories that appear most exposed include knowledge-workflow platforms such as legal research, compliance tools, contract analysis, and document processing systems. Business intelligence and dashboard software also faces pressure, since AI systems can increasingly query data and generate insights on demand rather than relying on prebuilt reports. Low-code and workflow automation tools may encounter similar challenges, as AI agents are now able to write scripts, integrate systems, and automate processes with less human configuration. Even parts of the customer support software market could be affected, particularly platforms focused on ticket triage and basic service interactions that AI can now handle with growing accuracy.

At the same time, not all software is equally vulnerable. Many companies provide foundational infrastructure that AI systems depend on rather than replace. Data infrastructure platforms, including data warehouses, ETL tools, and workflow pipelines, remain essential because AI agents are only as effective as the data they can access and process. Organizations still need systems to clean, store, govern, and secure their information, and those requirements tend to grow as AI adoption increases.

Cybersecurity is another area that may benefit from the rise of AI rather than suffer from it. As automation expands, so does the potential attack surface. AI can enable more sophisticated phishing attempts, automated intrusion methods, and new identity risks, all of which tend to increase demand for security tools. Core enterprise platforms such as ERP systems and certain CRM platforms also appear relatively resilient, since they function as systems of record and are deeply embedded in business operations. In addition, vertical software companies with proprietary datasets or highly specialized workflows often maintain strong competitive positions because switching costs are high and domain expertise is difficult to replicate.

Overall, the impact of AI on the software industry is unlikely to be uniform. Some companies will face meaningful disruption, while others may benefit from rising demand or new opportunities created by the technology. As these differences become clearer, broad sector exposure may become less effective, and careful company-level analysis is likely to play a larger role in investment decisions.

Employment Bifurcation

A subtle but important concern emerging in the labor market is a potential bifurcation between recent college graduates and more experienced workers. While overall unemployment remains relatively stable, younger graduates face the risk of unemployment and underemployment rates, in part because companies may begin hiring fewer entry-level workers and prioritizing candidates who can contribute immediately. Advances in AI and automation could play a role in this. Many of the tasks traditionally assigned to junior employees, such as research, reporting, and document preparation, are increasingly being handled by software and AI tools. This shift mirrors what we are seeing in the software sector itself, where automation is beginning to compress demand in areas built around repetitive knowledge work. In both cases, the early rungs of the ladder, whether entry-level jobs or certain categories of SaaS products, are becoming thinner, forcing workers and companies alike to adapt to a changing technological landscape.

This dynamic could lead to an intermediate period of increased structural unemployment as recent college graduates search for new career paths where demand is stronger or retool their skill sets to match a different mix of entry-level roles, particularly those that are less repetitive in nature. As routine analytical and administrative work becomes increasingly automated, the skills that remain in demand are shifting. Beyond technical proficiency, employers are placing greater value on soft skills such as communication, critical thinking, adaptability, and collaboration. Other areas that may become more important include problem framing, creativity, project management, client relationship skills, and the ability to interpret and apply insights rather than simply producing them. In many fields, knowing how to work alongside AI tools, validating outputs, and translating results into business decisions may become just as important as traditional entry-level tasks once were. Over time, this transition may reshape how early careers develop, with greater emphasis on judgment, interpersonal effectiveness, and applied expertise rather than purely repetitive work.

While the unemployment data does not yet show this trend, we have seen a 90-bps uptick in unemployment for people who are 25+ years old and have at least a bachelor’s degree, higher than the increase in overall unemployment over the past 12 months.

Electricity

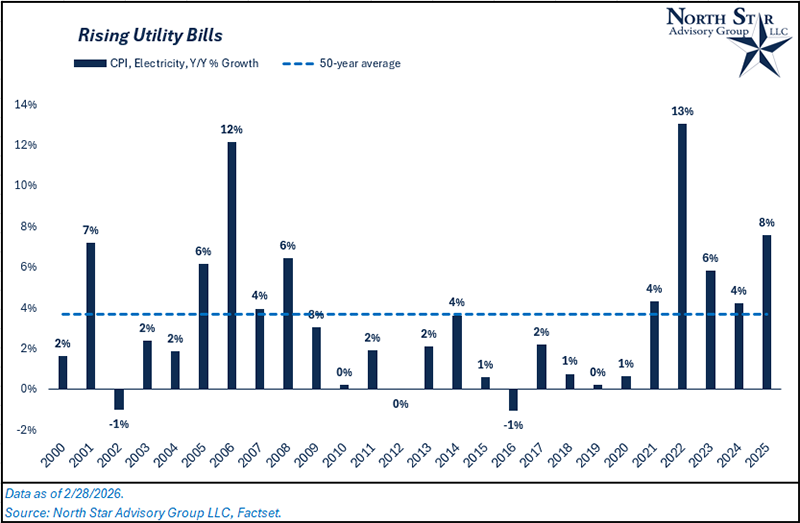

AI’s impact is not confined to software or the labor market. One of the most important second-order effects is emerging in electricity markets. Training and running large AI models requires enormous computing power, and hyperscale data centers are becoming one of the fastest-growing sources of electricity demand in certain regions. After years of flat demand, utilities and grid operators are now planning for a step-change in consumption. If this trend continues, the economic ripple effects could include higher regional power prices, increased infrastructure investment, and a renewed capital cycle in energy and grid modernization. In that sense, AI is beginning to influence not just digital industries but the physical backbone of the economy.

Broadly in the U.S., consumers have faced rapidly growing electricity prices across the board since early 2020 as the Covid pandemic accelerated the digitization of our economy. This consistent price growth in electricity has been akin to the first digital revolution in the early 2000s. Now, AI is putting continued upward pressure on this trend as the technology’s adoption continues to accelerate across households and more recently enterprises. Broad prices for electricity jumped 8% in 2025 compared to 2024, and this rate of increase is a reaccelerating following the disinflationary years of 2023 and 2024.

While prices were up 8% in 2025 broadly, there was some bifurcation regionally. The west coast and the south saw electricity prices increase by 2.5% and 5.5% respectively in 2025, lower than the national average. In the Northeast and Midwest, prices were up 10% and 11.4% respectively in 2025. In our view, we are starting to see a correlation between regional electricity prices and data center projects. Columbus, OH and Chicago, IL are two cities who have had some of the highest growth in data center projects over the past two years, explaining why midwestern electricity increases are above average. Northern Virginia (included in the Northeast numbers) has the highest concentration of data centers in the U.S.

While most consumers are facing higher electric bills, businesses are also feeling this effect, especially businesses operating in energy-intensive industries. A lot of these industries are within the materials sector; metals, building/cement products, chemicals, paper, etc. Fertilizer production, mining, semiconductor manufacturing, and food processing also require a large amount of electricity. These companies could face some sort of margin pressure from overall the adoption of AI.

Safe Haven or Long-term investment?

Gold has seen a notable resurgence in both price momentum and investor demand, driven largely by macro uncertainty, persistent inflation concerns, and a growing desire among global central banks and private investors to diversify reserves away from the U.S. dollar. Geopolitical tensions, elevated fiscal deficits, and questions around long-term currency stability have reinforced gold’s appeal as a neutral reserve asset that sits outside the traditional financial system. In periods where real interest rates are volatile and confidence in monetary policy wavers, gold often regains its role as a psychological and portfolio hedge. That said, while gold can serve as a short-to-intermediate term store of value during instability, history suggests that equities have been a more powerful long-term hedge against inflation and currency debasement. Comparing the two over multi-decade periods provides important perspective on when each asset class has historically delivered the most value to investors.

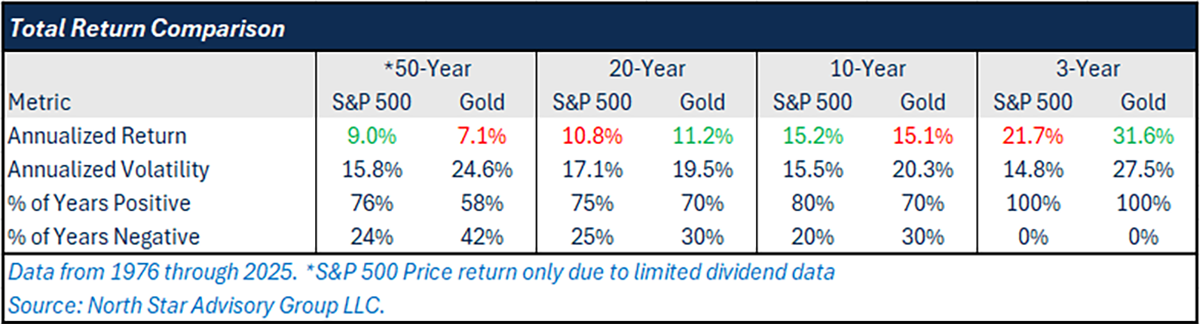

Over long time horizons, the performance gap between equities and gold has been substantial. Over the past 50 years, the S&P 500 has compounded at a meaningfully higher annual rate than gold. Gold has experienced powerful cyclical rallies, particularly during periods of monetary instability or crisis, but it has also endured extended stretches of flat or negative real returns. Equities, by contrast, represent ownership in productive assets that generate cash flow and benefit from innovation, population growth, and economic expansion. While gold can provide diversification and downside protection in certain macro environments, the historical data show that patient long-term capital has generally been rewarded more consistently in equities than in the precious metal.

In the table below, we summarize the annualized total return, volatility, and annual positive/negative rates for the S&P 500 and Gold. Gold has surged and been the winner over the past 3 years amid an inflation crisis, multiple global conflicts, and reduced confidence in the U.S. dollar. Despite the strong outperformance of gold over this time frame, you were still slightly better off by holding stocks over 10 years. For investors with a very long horizon, the 50 year number encapsulates the overall value proposition of stocks versus gold.

Gold had one of its worst days on record in January of this year following the announcement that Kevin Warsh would replace Federal Reserve chair Jerome Powell. In 2025, we saw continued shots thrown at Jerome Powell from Trump and his administration, which led to investor concern over Fed independence. This overall theme led to one of gold’s strongest years of price appreciation in 2025. Why did Warsh’s announcement spark a quick selloff in gold? Simply put, he was viewed as a candidate that will not bow to the influence of any administration be it Trump or anyone else. This restored some near-term confidence in the U.S. dollar, further showing how investor demand for gold has largely been driven by macro-uncertainty.

Tax Statements on Schwab

Desktop / Laptop (Schwab Website)

Step 1: Log in

- Go to schwab.com

- Click Log In

- Enter your credentials and complete any 2-factor authentication

- From the top menu, click Accounts

- Select Statements

- Click the Tax Forms tab (You may also see it labeled “1099 Dashboard” during tax season.)

- Use the dropdown to choose the tax year (e.g., 2025)

- You’ll see available forms such as:

- 1099 Composite

- 1099-DIV

- 1099-B

- 1099-INT

- 1099-R (for retirement accounts)

- 5498 (IRA contributions)

- Click the PDF icon next to each document

- Save the file to your computer

- Repeat for each account if you have multiple accounts

- Look for a “Combined 1099” or “Composite 1099” — this often includes everything in one PDF.

Step 1: Open the App

- Open the Schwab Mobile app

- Log in

- Tap Profile or More (three-line menu, depending on version)

- Select Statements

- Tap Tax Forms

- Select the tax year

- Tap the form you need

- Download or share the PDF (email, save to Files, etc.)

Where will the stock market go next?

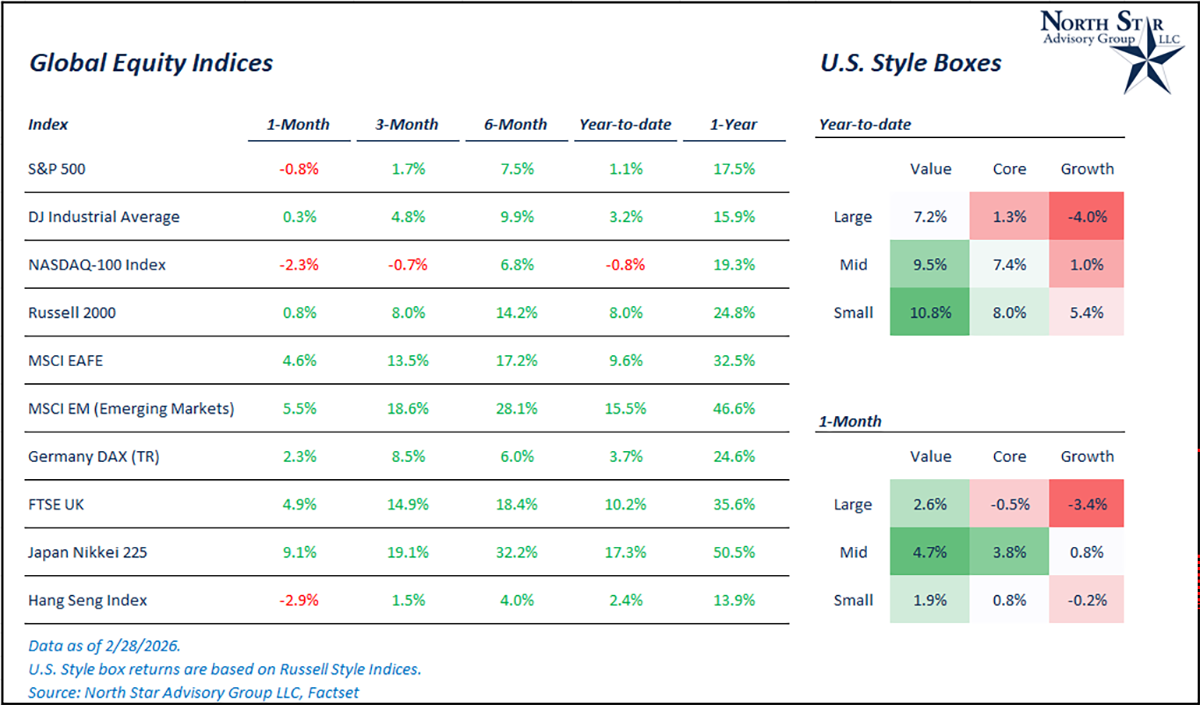

In February, The S&P 500 Index, representing U.S. large cap stocks, edged lower by 0.8% amid increased volatility. Breaking down the index’s performance in February, both the communication services and information technology sectors weighed most heavily on the index. Financial and healthcare sectors also posted negative results for the month. While the S&P 500 was down, small cap stocks and international stocks all posted positive returns for the month.

When it comes to the technology sector, AI is everything, and we’ve seen fears begin bubbling up within this mega-trend. On one hand, there are fears of software disruption by AI. On the other hand, investors are concerned that AI profitability is too thin in the near term to continue at the same pace of data center buildouts. In our view, these two fears conflict with one another. If AI is going to replace all software, then there should be muted profitability concerns around spending on data centers. In the near term, we expect continued choppiness over the next couple of quarters, especially in the technology sector, as investors reassess business models and try to separate the winners from the losers. As we wrap up 2026’s first quarterly earnings season, results were strong within technology. Of the 62 information technology companies inside the S&P 500 index that have reported earnings numbers this quarter, 94% of them beat the markets expectations for sales and EPS by a median value of 2.1% and 6.2%, respectively.

More broadly, short term volatility emerged from continued tariff confusion and the ongoing conflict between the U.S., Israel, and Iran.

The Russell 2000 Index (U.S. small cap) was up 0.8%, the MSCI EAFE Index (non-U.S. developed) was up 4.6%, and the MSCI EM Index (emerging markets) was up 5.5%. As technology jitters persist, investors’ dollars continue to rotate into other sectors such as real estate, industrials, and commodities.

We are passionately devoted to our clients' families and portfolios. Contact us if you know somebody who would benefit from discovering the North Star difference, or if you just need a few minutes to talk. As a small business, our staff appreciates your continued trust and support.

Keep sending your questions for a chance to be featured in next month’s Timely Topics.

Best regards,

Mark Kangas, CFP®

CEO, Investment Advisor Representative

Brian Duffield, CFA®

Co-Portfolio Manager & Market Strategist