Each month we ask clients to spend a few minutes reading through our newsletter with the goal of raising their investor IQ. September's addition of Timely Topics covers credit scores, IPO market trends, and July's job report under the Trump administration, highlighting factors driving changes in capital flows. NSAG also announces a partnership between BGSU’s Schmidthorst College of Business and Charles Schwab.

- Credit scores

- July’s jobs report

- Update on global markets

- IPO Revival

- NSAG News (BGSU)

- Where will the stock market go next?

Credit Scores

A strong credit score is one of the most important financial tools you can have. It impacts your ability to secure loans, qualify for favorable interest rates, and even influences opportunities such as renting an apartment or obtaining certain jobs. Lenders use your credit score to assess how likely you are to repay borrowed money, so a higher score signals financial reliability and can save you thousands of dollars over time. Whether you are preparing to buy a home, finance a vehicle, or simply want greater financial flexibility, maintaining a healthy credit score is essential for your long-term financial well-being.

Improving your credit score takes time and consistent effort, but the benefits are well worth it. Here are a few proven strategies to help raise your score:

- Pay bills on time: Payment history is the single largest factor in your score, so set reminders or automate payments to avoid late fees.

- Reduce credit card balances: Aim to use less than 30% of your available credit on each card, and ideally much less.

- Avoid opening too many new accounts at once: Multiple credit inquiries in a short period can lower your score.

- Check your credit report regularly: Review for errors or fraudulent accounts and dispute inaccuracies promptly.

- Keep older accounts open: A long credit history can positively influence your score, even if the card is rarely used.

- Diversify your credit mix: Having different types of credit (such as a credit card, car loan, or mortgage) can improve your score over time.

- Negotiate with creditors: If you’re struggling with payments, reach out to creditors to set up payment plans before accounts go delinquent.

- Pay more than the minimum: Reducing principal balances faster can improve your credit utilization ratio and overall score.

- Limit hard inquiries: Only apply for new credit when necessary to avoid unnecessary hits to your score.

By practicing these habits consistently, you can steadily improve your credit profile, increase your financial options, and position yourself for future success.

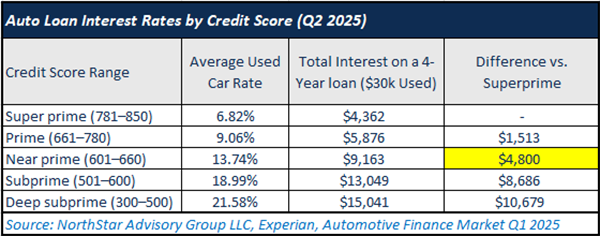

When writing a portion of last month's Timely Topics that discussed the new auto interest credit in the One Big Beautiful Bill, we noticed how wide the incremental changes in interest rates can be based on credit scores. In the table below, we’ve summarized different lending rates for new and used automobiles. Holding all else equal, a super prime borrower (781 – 850) will pay $4,800 less in interest on 4-year $30k used car loan versus a near prime borrower (601 – 660).

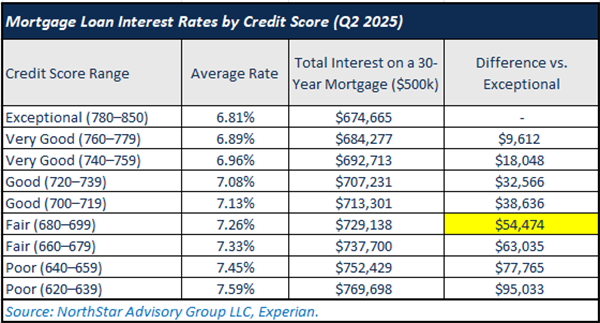

If you are looking to buy a home and planning on a 30-year mortgage for $500k, the same super prime borrower (780+), can save ~$54k over 30 years relative to prime borrower who has a credit score within the range of 680 – 699.

The examples given above further stress the importance of earning and maintaining a strong credit score when looking to achieve your long-term financial goals.

July’s Jobs Report

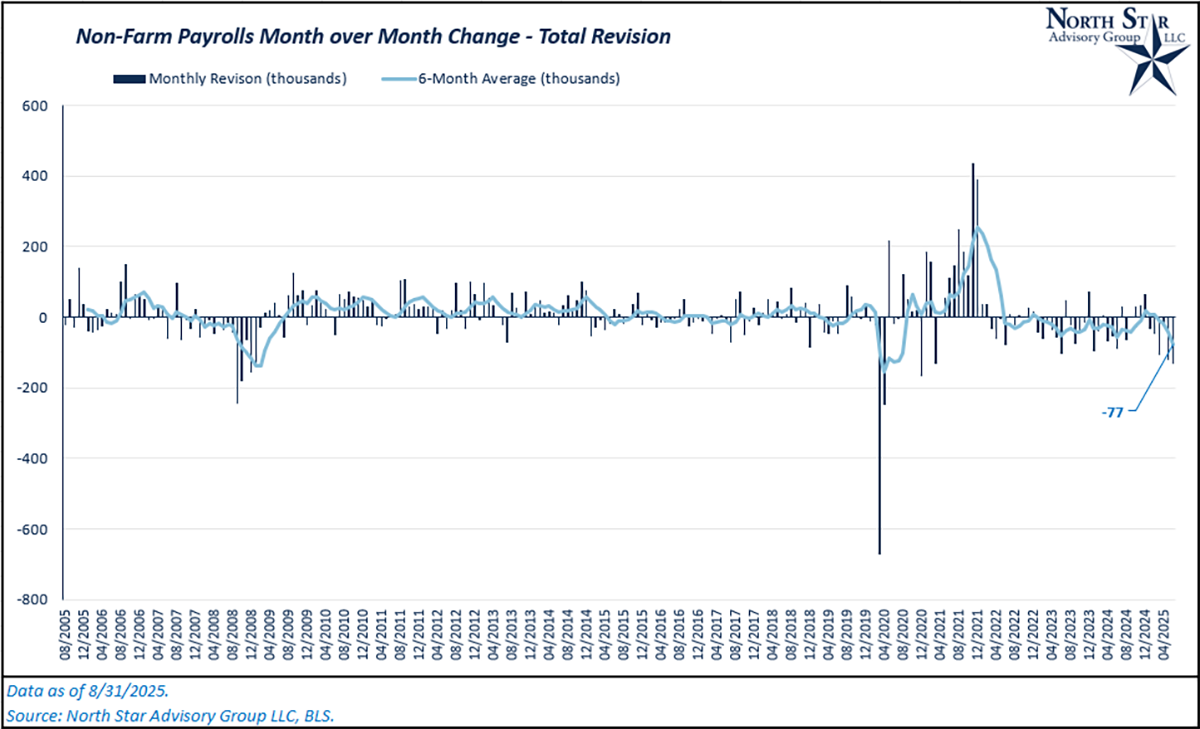

On August 1st, the Bureau of Labor Statistics (BLS) reported total non-farm payroll (NFP) gains of 73k relative to one month prior (June 2025). This number was well short of the +115k estimated my FactSet. On top of the miss for July, June and May’s reports were revised significantly lower. Originally, May and June’s numbers were estimated at +139k and +147k, respectively. In July, these were revised down to +19k and +14k, representing a total revision of -253k in aggregate between the two months, wiping out any job gains made in July and bringing job growth close to flat in recent months. U.S. equity markets broadly sold off while bond markets rallied on August 1st in response to this report as there is a fear that tariffs may be fueling some slowdown

Revisions have always been made to previous monthly reports for various reasons. Jobs report revisions typically occur because initial data is based on incomplete employer submissions and early survey responses. As more employers provide updated information and seasonal adjustments are refined, statisticians correct and improve the accuracy of previous estimates. Additionally, benchmarking against tax records and correcting reporting errors help ensure the data better reflects actual employment levels over time. Over the past 20 years, monthly revisions have typically been negative, between -18k and +4k on average, so these harsh revisions raised a red flag to market participants. The headlines were mostly dominated by the subsequent reaction of the Trump Administration when President Donald Trump dismissed the Bureau of Labor Statistics (BLS) Commissioner Erika McEntarfer, following the disappointing July jobs report. Trump accused McEntarfer of manipulating the data for political purposes. In our view, and the majority of the Street’s view, these revisions were in line with the historical revision processes.

This unprecedented action has led to investor skepticism regarding the objectivity of economic data, potentially undermining confidence in critical economic indicators. Analysts warn that the sudden removal of a BLS chief could erode trust in government statistics, which have traditionally been viewed as a global benchmark. In our view, politicizing economic data can create a slippery slope for confidence in the U.S. as the benchmark for global market integrity, which has been one of the drivers for U.S. equity markets commanding a premium valuation versus the rest of the world (“American Exceptionalism”). A similar concern can be made about other actions taken by the administration such as volatile trade policy and publicly pressuring the Federal Reserve’s interest rate policy. We’ve already seen signs of this concern creeping into markets in 2025 (see the next section “Update on global markets”).

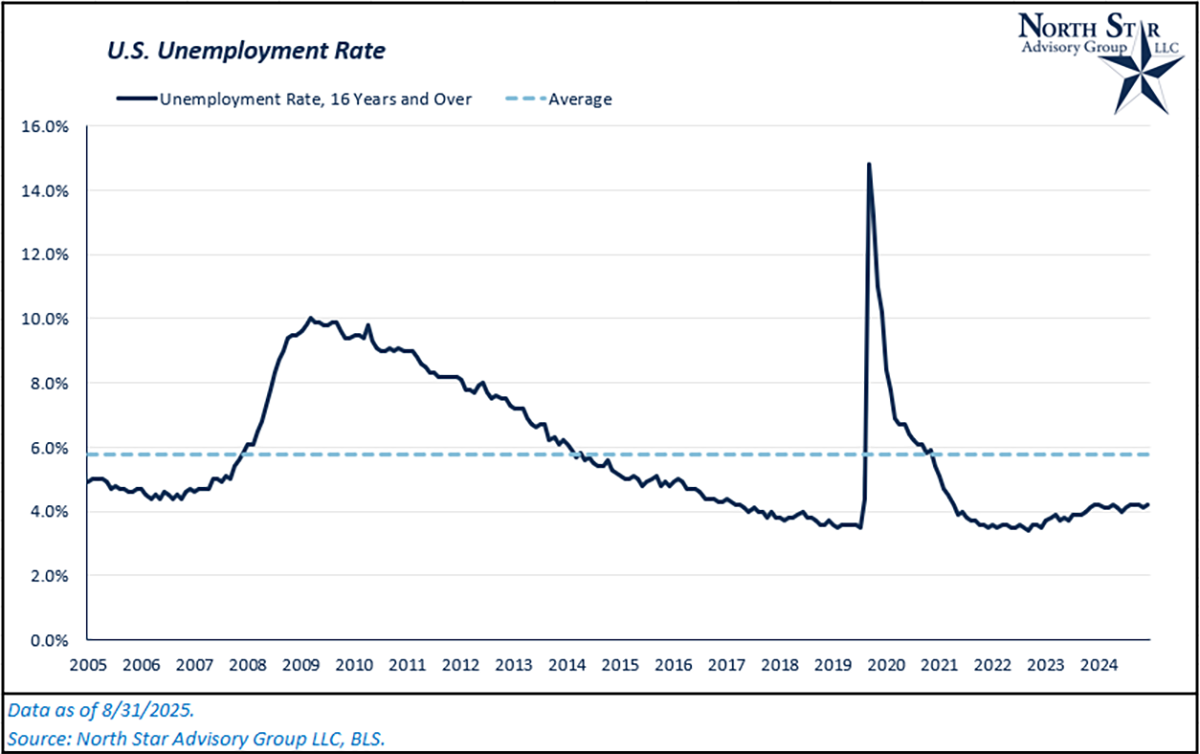

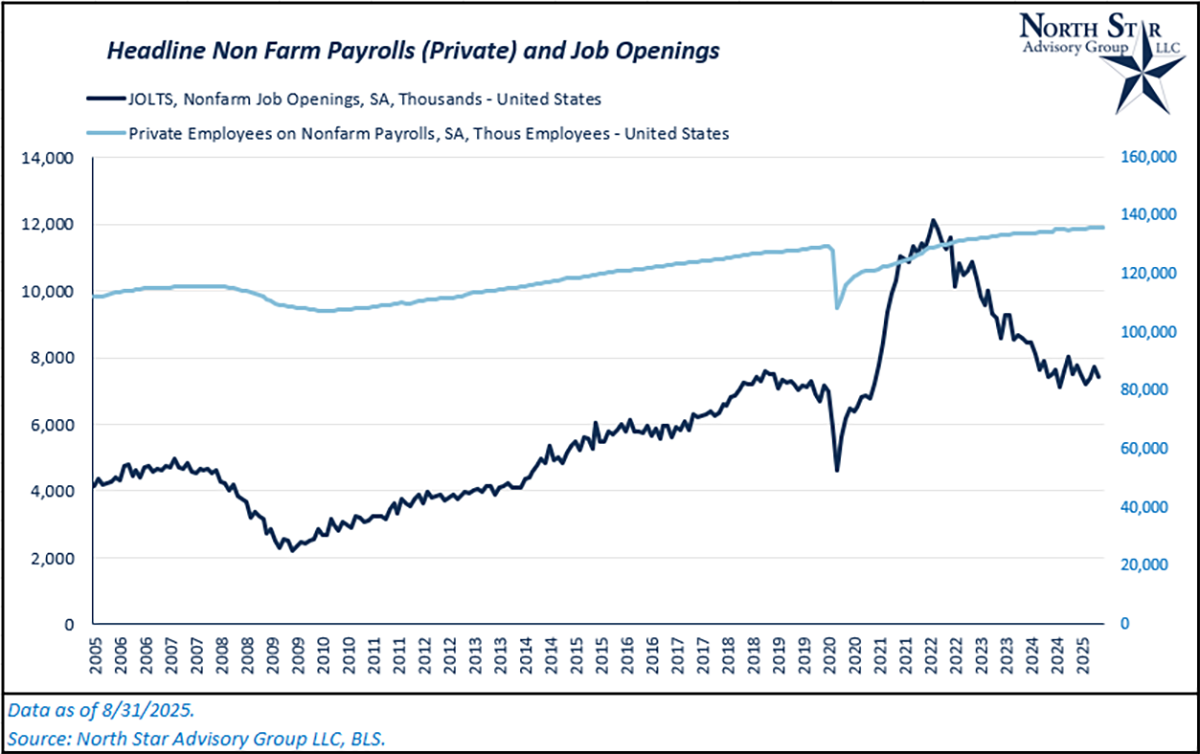

Zooming out, average monthly NFP revisions of around -77k over the past six months. Excluding Covid and the global financial crisis, this is the worst six-month average number in the past 20 years, causing some concern for investors. While revisions have been more negative in recent months, overall employment data has been historically strong in recent years and a couple cracks in the armor (negative revisions) may look worse than what’s actually occurring in the labor market. The unemployment rate is still near historical lows at 4.2%, and initial claims for unemployment insurance have been relatively in line with expectations. We will be focused on August’s payroll numbers and any potential revisions to July’s +73k number.

In the two charts below, you’ll see that the unemployment rate continues to hover around historical lows despite tricking up to 4.2% over the past 18 months. This is still well below the 20-year historical average and is driven by the fact that we have yet to see an overall decline in employment despite negative revisions, as evidenced by the total number of employees on private payrolls. Additionally, job openings (“JOLTS”) continue to remain above pre-Covid levels as a lot of the decline in this data is being driven by an unwind of Covid-era stimulus/fiscal policy.

Update on Global Markets

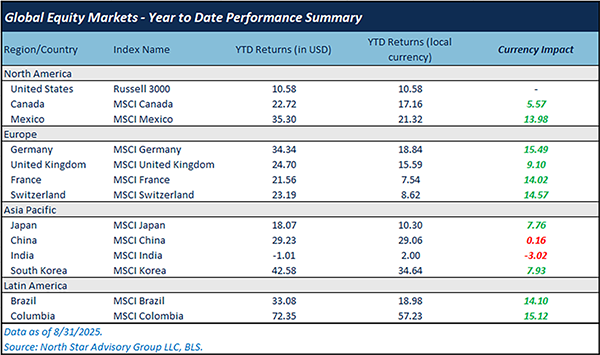

Many clients have been surprised by how well global markets are performing so far in 2025 with non-U.S. stocks leading in performance. We’ve seen many regions outside of the U.S. begin a new cycle of positive valuation re-rating. We’ve long mentioned and discussed with clients that relative valuation discounts in these markets create attractive long-term potential. But we’ve also emphasized that re-ratings of valuation levels don’t happen without a catalyst, and they don’t happen overnight. Typically, these cycles are secular and develop over multiple years. Year to date as of 8/31/2025, the U.S. dollar index has fallen 9.6%, as capital has shifted out of the U.S. denominated investments and into other markets. This has been the first broad catalysts to spark 2025’s re-rating of non-U.S. stocks. In the table below, we’ve summarized the performance of global stock markets for 2025, breaking down the total return in U.S. dollar terms, and how much of that return was generated by currency fluctuations. Most major international markets are outperforming the U.S. in 2025, with the exception of India. Even if you strip away the currency benefit realized from a falling dollar, most major markets are still well outperforming the U.S., with the exception of India, Japan, France, and Switzerland.

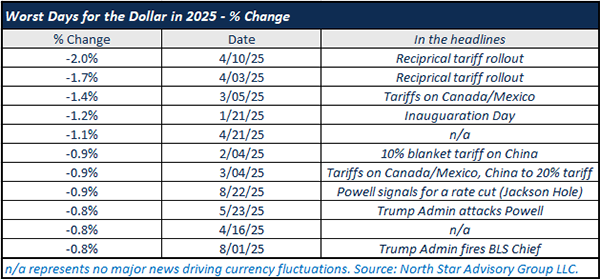

As mentioned in the prior section, certain actions by the administration have been putting some stress on global trust in the U.S. capital markets. In the table below, we’ve pulled some of the worst days for the U.S. Dollar Index in 2025 to see what was happening in each of those days. As you’ll notice, the volatile nature of the administration’s trade policy swings is a common theme that has been driving volatility in the dollar.

IPO Revival

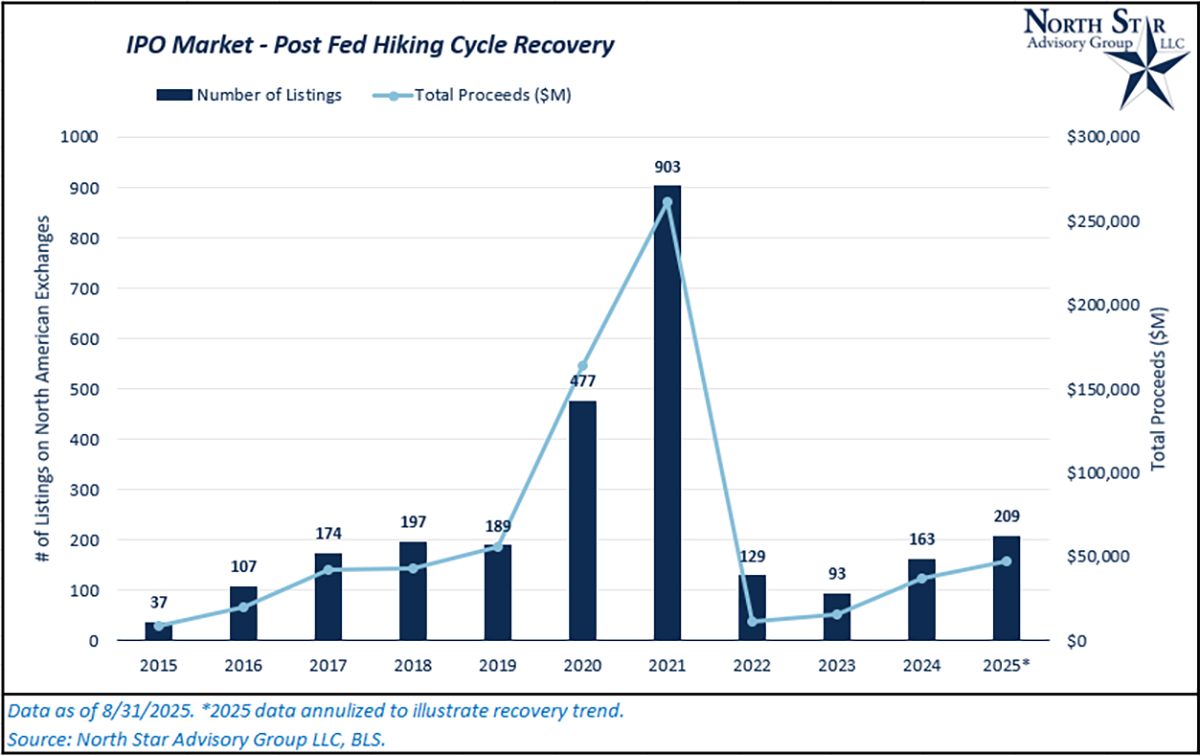

After the record-breaking IPO activity of 2020 and 2021, with 903 listings in 2021 raising more than $261 billion, the market experienced a sharp correction. In 2022, IPO activity plunged to just 129 deals totaling $11.5 billion, marking one of the weakest years in recent history. 2023 showed only modest improvement, with 93 offerings raising $15.8 billion. The rebound gained more momentum in 2024 with 163 listings generating $36.9 billion, and 2025 has so far sustained that recovery with 139 IPOs and $31.7 billion in proceeds. While still far below the highs of 2020–2021, the past two years indicate a healthier, more stable IPO environment compared to the post-pandemic slump.

For private equity and venture capital investors, the IPO market is a key exit channel, and its fluctuations directly influence deal strategies. During the 2022–2023 slowdown, many private equity-backed companies delayed going public, turning instead to secondary sales or holding portfolio companies longer. With capital raising conditions improving in 2024 and 2025, more PE-backed firms are finding favorable windows to list, though valuation discipline remains much tighter than in the frothy 2021 cycle. If the current moderate but steady pace continues, private equity could see a more predictable exit environment, one that rewards quality over speed, potentially leading to stronger post-IPO performance and more sustainable returns.

NSAG News

This summer, Bowling Green State University’s Accounting and Finance Department received their largest single corporate gift to date.

“Grants of this magnitude are not done overnight. It has taken three years of work and coordination by the Schmidthorst College of Business Finance Advisory Board, Charles Schwab, BGSU and myself," said Mark Kangas, a BGSU alumnus, current CFP holder and owner of North Star Advisory Group, an Ohio-based RIA firm. "We were fortunate to tap into the connections that North Star Advisory Group had made with Charles Schwab to help facilitate the largest single corporate gift that the college’s Accounting and Finance Department has received to date."

Bowling Green State University’s Schmidthorst College of Business is partnering with Schwab Advisor Services and the Charles Schwab Foundation to strengthen student success in the growing financial planning field. Through a multi-year grant, the collaboration will fund scholarships, particularly for first-generation and non-traditional learners, support faculty outreach, and provide opportunities for students to attend national conferences and connect with professionals in wealth management and registered investment advising. The grant will also allow BGSU to host an annual financial planning symposium to foster valuable networking and career opportunities. Leaders from BGSU and Schwab emphasize the partnership’s importance in preparing graduates to meet workforce needs and increasing the number of candidates for the Certified Financial Planner certification.

In 2022, while Mark Kangas served as President of the Finance Advisory Board, he started an initiative to increase support for the department and the number of students graduating with either a CFP or Chartered Financial Analyst designation. Three years later, the college is seeing a 50% increase in the number of new students interested in studying finance for Fall 2025 compared to last year. This partnership further demonstrates the College’s goal of continuing this momentum and demonstrates the power of long-term public-private collaboration.

Where will the stock market go next?

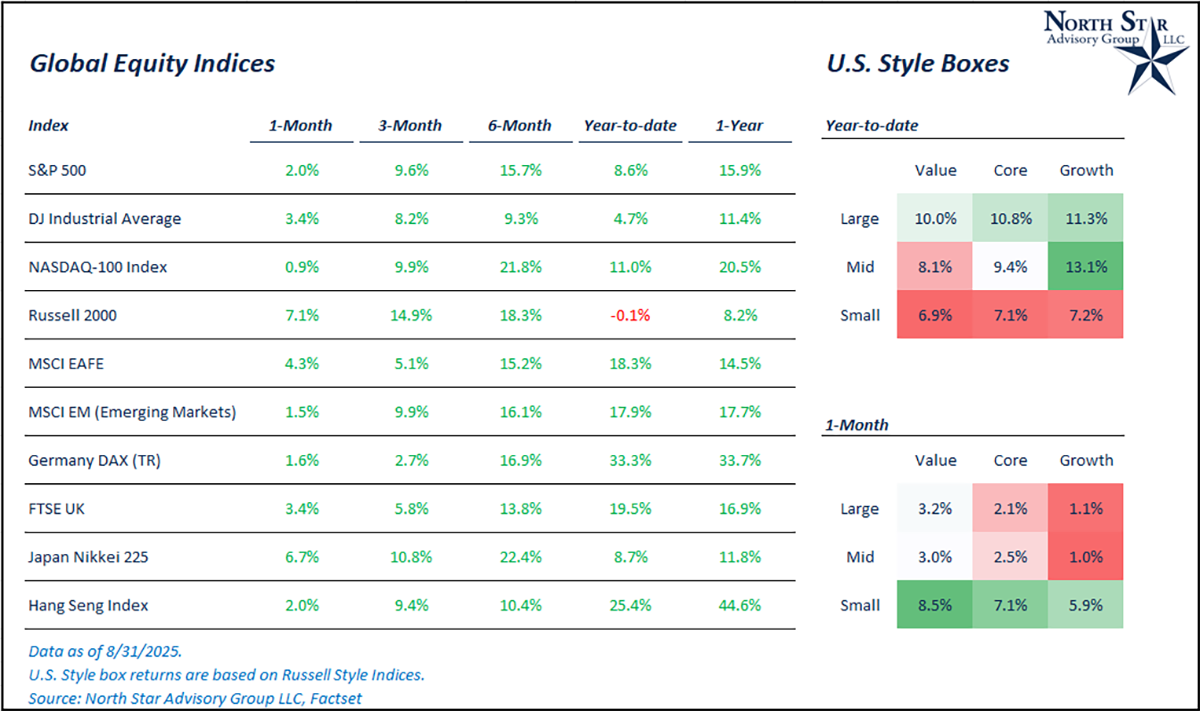

As of the end of August, the S&P 500’s year-to-date performance sits at 8.6%, and the next twelve months (NTM) price to earnings ratio for the index sits at 22.3x. At over 22 times NTM earnings expectations, the index’s valuation is nearing levels where previous short-term pullbacks in the market occurred over the past couple of years. While valuation alone is usually not the sole factor driving a buy or sell decision, it does provide guidance on the type of returns we should expect going forward. Our view has not changed, and we continue to expect lower than historical average (but positive) returns for the U.S. market going forward due to the valuation headwind. Given that we are already positive by almost 10% for the year, we don’t expect too much upside potential for the S&P 500 throughout the remainder of 2025. This is why we have and continue to encourage clients to diversify into other areas of the market, such as emerging markets, international developed, and U.S. small/mid cap stocks. In August, we saw the growthiest/highest valued areas of the market pull back a bit as investors trimmed positions and took profit on some the stocks that had the most momentum in 2025.

Small cap stocks in the U.S. showed strong performance in August as markets saw the probability of Federal Reserve rate cuts increase. The Russell 2000 Index was up 7.1%. Additionally, developed international stocks showed strength in August as the MSCI EAFE index was positive by 4.3%. In August, we also saw the growthiest/highest valued areas of the market pull back a bit as investors trimmed positions and took profit on some the stocks that had the most momentum in 2025. In last month’s Timely Topics, we noted that relative valuations between growth stocks and value stocks were hitting levels where growth stock valuations were almost 100% higher than value stocks. In August, we saw some of this unwind as investors began rotating back into value. We expect this to at least continue in the short term.

We are passionately devoted to our clients' families and portfolios. Contact us if you know somebody who would benefit from discovering the North Star difference, or if you just need a few minutes to talk. As a small business, our staff appreciates your continued trust and support.

Keep sending your questions for a chance to be featured in next month’s Timely Topics.

Best regards,

Mark Kangas, CFP®

CEO, Investment Advisor Representative

Brian Duffield, CFA®

Co-Portfolio Manager & Market Strategist