Each month we ask clients to spend a few minutes reading through our newsletter with the goal of raising their investor IQ. August’s edition of Timely Topics examines the major changes coming from the passing of the “One Big Beautiful Bill” regarding taxes, federal student loan financing, and defense spending. Additionally, we provided an example of an asset location strategy for clients as a refresher.

- Tax policy

- Federal student loan financing

- New defense budget

- Asset location

- NSAG News

- Where will the stock market go next?

Tax policy

The recently passed One Big Beautiful Bill (OBBB) brings sweeping changes to the U.S. tax code, impacting individuals, families, and businesses at all income levels. While the bill extends many popular provisions from the first Trump Administration, it also offers new opportunities for tax efficiency and introduces limitations that will require careful planning.

Key Tax Changes That Benefit Most Investors

- Standard deduction limits were increased

- Tax filers who take the standard deduction will receive a larger benefit after the passing of the OBBB. For the 2025 tax year, the standard deduction amounts are:

- Single filers and married filing separately: $15,750 (was $15,000)

- Married filing jointly and qualifying surviving spouse: $31,500 (was $30,000)

- Head of household: $23,625 (was $22,500)

- This change should will not likely have a meaningful impact on the economy as each additional $750 deduction is worth around $125 per person. Furthermore, the benefit of the small amount will be delayed until it is realized when filing the 2025 tax returns in 2026.

- Permanent lower income tax rates

- The bill locks in the 2017 Tax Cuts and Jobs Act rates, preventing a scheduled increase in marginal tax rates. This means the top federal income tax rate remains 37%, rather than reverting to 39.6%.

- While this is a win for taxpayers, however, maintaining existing rates will not stimulate the economy further.

- Up to $10,000/year on auto interest paid

- The new car loan interest deduction applies to all qualifying new cars, but there are some important caveats.

- The car must be new (not used or leased), be for personal use (not commercial or fleet), be assembled in the U.S. and weigh less than 14,000 lbs.

- Income phaseouts apply to those making $100K and filing single or $200K filing joint.

- This is a new above-the-line interest deduction that can be taken in addition to the standard deduction.

- While this is a win for taxpayers, the actual amount of interest deduction and economic benefit will be very small, illustrated in a few examples below:

- A 4-year $30,000 auto loan at *6.8% will generate interest of ~$1,100 in its first year

- The economic benefit is further reduced when you consider the deduction is applied at the tax filer’s marginal tax rate. Using the 22% marginal tax rate, the benefit ends up being reduced to ~$240.

- A 2025 Honda accord ranges from $28k-$39k based on the package. Assuming an average loan of $30k after trade in or downpayment and Honda’s 3% interest rate, first year interest is ~$470 (or a $103 economic benefit at the 22% marginal tax rate.

- To maximize the full $10,000 deduction at *6.8%, you would need to have an auto loan of ~$290k. Anyone buying this type of car is likely above the income phaseout range with some exceptions for retirees.

- Higher SALT deduction cap

- The State and Local Tax (SALT) deduction cap increases from $10,000 to $40,000 through 2029.

- While this is a win for taxpayers in high-tax states, the larger amount may be less beneficial than the headline reads. The bill phases down the $40,000 SALT cap for taxpayers making over $500,000 and effectively reduces the SALT cap back to $10,000 for those making over $600,000.

- Simplified and expanded child tax credit

- The Child Tax Credit is expanded to $2,200 per child, fully refundable for most taxpayers, with simplified income thresholds to improve access for middle-income families.

- While this is a win for taxpayers, the increase was only $200 per child and will not likely have a meaningful impact on the economy.

- QBI deduction made permanent

- Business owners who file as sole proprietors or pass-through entities can now permanently claim the 20% qualified business income deduction, offering long-term certainty for self-employed taxpayers. Higher-income business owners are subject to partial deductions and phase-outs when earning $75,000 for individuals and $150,000 for joint filers.

- While this is a win for taxpayers, this deduction already existed and will have little additional impact on the economy.

- Estate tax certainty

- The most impactful provision of the OBBBA is the permanent increase of the federal estate and gift tax exemption to a substantial $15 million per individual, effective January 1, 2026. For married couples, this translates to an impressive $30 million. This change is a game-changer, especially for those who were anticipating the sunset of the Tax Cuts and Jobs Act (TCJA) provisions, which would have significantly reduced these exemptions. The OBBBA removes that uncertainty, providing long-term clarity and a much higher baseline for tax-free wealth transfer. This means many more families will find their estates entirely exempt from federal estate taxes, allowing their full legacy to pass to their chosen beneficiaries without federal intervention.

- While this is a win by increasing certainty around tax and estate planning, a $14 million per individual or $28 million per couple deduction already existed. Therefore, the new limits will have little additional impact on the economy.

- Itemized deduction limitations for high earners

- For those earning more than ~$500,000/year, the tax benefit of itemized deductions is capped at the equivalent of a 35% tax rate, which may reduce the value of charitable and mortgage deductions.

- Excise tax increases on private foundations & large universities

- High-net-worth families involved in charitable foundations or university endowments may see higher excise taxes on investment income.

- International business tax changes

- Those with foreign investments or business interests should be aware of higher tax rates on Global Intangible Low-Taxed Income (GILTI) and changes to Foreign-Derived Intangible Income (FDII).

- New, used, and commercial EV credits expire Sept 30, 2025

- The OBBB removes the prior $7,500 tax credit for qualifying new electric vehicles.

- The government has effectively removed their subsidies for the auto industry with the elimination of EV tax credits and the minimal benefit of the new auto interest deduction noted above. While this helps the federal budget, it will have little positive impact on the economy.

*As of August 2025, the average APR for new auto loans is hovering around 6.8%.

Provisions to watch out for

What does this mean for clients The bill offers tax certainty and some new planning opportunities, especially for families, small business owners, and those saving for retirement. But higher earners will face new planning challenges, particularly around deductions and charitable giving.

Federal student loan financing

The One Big Beautiful Bill introduces significant restrictions on federal student borrowing, overhauls income‑driven repayment (IDR), and phases out the current SAVE plan.

New caps on federal loan amounts

- Undergraduate limits tied to expected earnings

- Annual and aggregate borrowing for undergraduate students is now capped based on the median starting salary in their chosen field (e.g., STEM vs. liberal arts), replacing the flat-dollar limits.

- Graduate & professional degree caps

- Master’s and professional programs face tiered borrowing ceilings which are typically between $50,000 and $100,000 depending on projected first‑year incomes.

- Impact on families

- Students pursing jobs with lower‑paying median starting salaries (education, social work…) may need to rely more on their own contribution, income from working while going to school, family contributions or institutional aid once federal loans are max out.

Overhaul of Income‑Driven Repayment (IDR)

- Streamlined, one‑size‑fits‑all IDR

- All legacy plans (SAVE, REPAYE, PAYE, IBR) are consolidated into a single, simpler IDR formula:

- Monthly payments ranging from 1-10% of adjusted gross income (AGI) (down from prior 10–20% range of discretionary income).

- Stricter certification requirements

- Annual income recertification moves to a two‑year cycle, with semi‑annual income checks to reduce over and under payments.

- Interest subsidy adjustments

- Unpaid interest on subsidized loans is forgiven only for the first five years of repayment; thereafter, any unpaid interest may capitalize annually.

-

Phasing out SAVE (Saving on a Valuable Education)

- Return to standard IDR Terms. With SAVE eliminated, borrowers lose its key features:

- 0% interest on low‑income borrowers (previously under 225% of poverty line).

- Family size adjustments that exempt a larger portion of income from payment calculations.

- Longer forgiveness horizons

- Without SAVE’s accelerated forgiveness (20 years for undergraduate; 25 for graduate), the new plan’s 30‑year standard timeline may delay relief for many graduate‑degree holders.

- Higher effective payments for low-income borrowers

- Those who benefited from SAVE’s zero‑interest subsidies and larger income exclusions will see modestly higher monthly bills and more interest capitalization.

What should clients do now

- Check your remaining eligibility

- If you’re near the new borrowing caps, consider consolidating before limits tighten and explore whether parent PLUS or private options still make sense.

- Lock In SAVE benefits

- Borrowers currently in SAVE should maximize its zero‑interest and larger exemption features before the phase‑out begins.

- Reassess your repayment strategy

- With a single IDR formula replacing multiple plans, run fresh amortization scenarios to compare standard vs. IDR outcomes over 20-30 years.

- Plan for higher payments if applicable

- Low‑income borrowers previously on SAVE may see increases and need to budget accordingly or explore deferment options during low‑income periods.

- Explore alternative funding

- Stay Informed

- Implementation details (e.g., exact cap formulas, recertification schedules) will roll out over the next 12–18 months; keep in touch with us if you find yourself in the middle of college financial planning.

New defense budget

The One Big Beautiful Bill includes one of the largest increases in defense spending in recent years, reflecting shifting global security priorities and renewed focus on both traditional and emerging threats. Here’s an overview of how the new funding is allocated, along with the potential upsides and challenges for the military, defense contractors, and taxpayers. The bill authorizes approximately $950 billion in total defense funding for FY 2026, a 10% increase over the prior year’s base budget.

Some of the highlights in the new defense budget include

- Focus on Indo-Pacific deterrence

- Roughly $120 billion is earmarked for the Pacific Deterrence Initiative and related efforts to counter China’s expanding influence in the Indo-Pacific region. This includes new forward bases, missile defense systems, and joint exercises with allies.

- Modernizing the nuclear triad

- The bill provides an estimated $80 billion to modernize America’s nuclear deterrent which involves replacing aging ICBMs, upgrading submarine-launched ballistic missiles, and revamping strategic bombers. Supporters say this is critical for long-term security; critics warn it could fuel a new arms race.

- Strengthening cybersecurity and AI

- Around $50 billion will go toward developing advanced cybersecurity defenses, artificial intelligence tools, and unmanned systems to counter threats from state and non-state actors in cyberspace.

- Increased personnel pay and benefits

- The bill includes the largest pay raise for active-duty military personnel in over 20 years (~5.5% year over year increase) with expanded childcare support and housing stipends aimed at improving recruitment and retention.

- Deficit impacts

- The Congressional Budget Office estimates that the defense spending increase will add approximately $450 billion to the federal deficit over the next 10 years, unless offset by spending cuts elsewhere or supplemented with new revenue (tariffs). Spending on cybersecurity/emerging technology/AI, Indo-Pacific deterrence, and European deterrence are seeing the most robust growth relative to recent years. Overall, research & development continues to grow at a faster rate than procurement. Cybersecurity and AI-focused software companies are likely to experience growth in new contracts from the new budget, given its focus areas. Additionally, defense contractors who are focused on drone technology, unmanned missile systems, and shipbuilding will likely benefit greatly from the Indo-Pacific and European regional focus.

- Oversight challenges

- Defense analysts caution that rapid spending hikes, especially in advanced technology programs, increase the risk of waste, fraud, and cost overruns without stronger oversight and procurement reforms. Reading further between the lines, the hyper-competitive landscape for the businesses building AI-enabled software and researching new technologies will continue to drive the speed of innovation and increased demand for computing power/AI-infrastructure.

- Potential for geopolitical tensions

- While the increased focus on deterrence in the Indo-Pacific region and Europe aims to bolster national security, some foreign policy experts warn it could escalate regional arms races and strain diplomatic relations.

Spending on cybersecurity/emerging technology/AI, Indo-Pacific deterrence, and European deterrence are seeing the most robust growth relative to recent years. Overall, research & development continues to grow at a faster rate than procurement. Cybersecurity and AI-focused software companies are likely to experience growth in new contracts from the new budget, given its focus areas. Additionally, defense contractors who are focused on drone technology, unmanned missile systems, and shipbuilding will likely benefit greatly from the Indo-Pacific and European regional focus.

Reading further between the lines, the hyper-competitive landscape for the businesses building AI-enabled software and researching new technologies will continue to drive the speed of innovation and increased demand for computing power/AI-infrastructure.

Asset location

Asset location is a powerful strategy for investors; rather than changing your mix of investments, you optimize where those investments are held to minimize taxes and maximize long-term wealth. Recently, we’ve had a few clients inquire about asset location strategies with respect to Roth IRAs (tax exempt accounts) and Traditional IRAs (tax deferred accounts). When dollars are withdrawn from Traditional IRAs, those withdrawals are taxed at income tax rates, while dollars withdrawn from Roth IRAs are not subject to taxation.

The following example outlines a strategy that NSAG has utilized with clients for several years. Given recent inquiries, we believe it is appropriate to provide a brief refresher review of this particular strategy.

General rule of thumb

- Place higher returning assets (like stocks) in Roth IRAs, where growth is tax-free if withdrawn after age 59.5.

- Place lower-returning, income-generating assets (like bonds) in Traditional IRAs, where withdrawals are taxed as ordinary income.

This strategy works best over longer horizons and does not require taking more risk as it’s purely about smarter asset placement. To illustrate how this strategy works in a simple way, we’ll provide two basic scenarios below for a hypothetical client.

Assumptions for both scenarios:

- $500k in Roth IRAs

- $500k in Traditional IRAs

- 8.5% annual growth rate for stocks*

- 4.1% annual growth rate for bonds*

- 60% Allocation to Stocks / 40% allocation to bonds in aggregate

- 25% income tax rate

- 20-year time horizon

*Rates of return are not guaranteed and are only used for the purposes of this example.

.png)

Key takeaways for clients

- Same portfolio, better outcome: You don’t need to take more risk, just hold your assets in the right types of accounts. In this example, we held the same amount of bonds ($400k) in both scenarios.

- Stocks love Roths: High-growth assets benefit the most from tax-free compounding in Roth IRAs.

- Bonds fit best in Traditional IRAs: Slower-growing, taxable-income-producing investments are better sheltered in tax-deferred accounts.

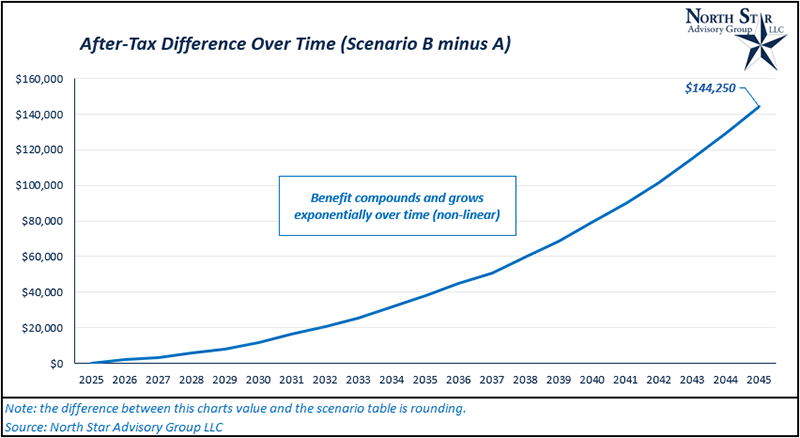

- Compounding advantage grows over time: The longer your time horizon, the greater the benefit (See chart below).

Note: The difference between the ending value in the chart ($144,250) and the table ($140,000) is solely due to rounding of values.

NSAG News

Nick Stern successfully passed the Series 65 examination in July 2025. This accreditation authorizes individuals to serve as investment adviser representatives, covering critical subjects necessary for offering informed investment advice to clients. Nick's continuous educational accomplishments highlight our firm's commitment to personal development and professional excellence. Nick will continue his educational pursuits by going after his life and health insurance license and finally the Certified Financial Planner™ (CFP™) designation. We look forward to seeing the positive impact he will continue to make as he grows with NSAG. Congratulations, Nick, on this well-deserved milestone.

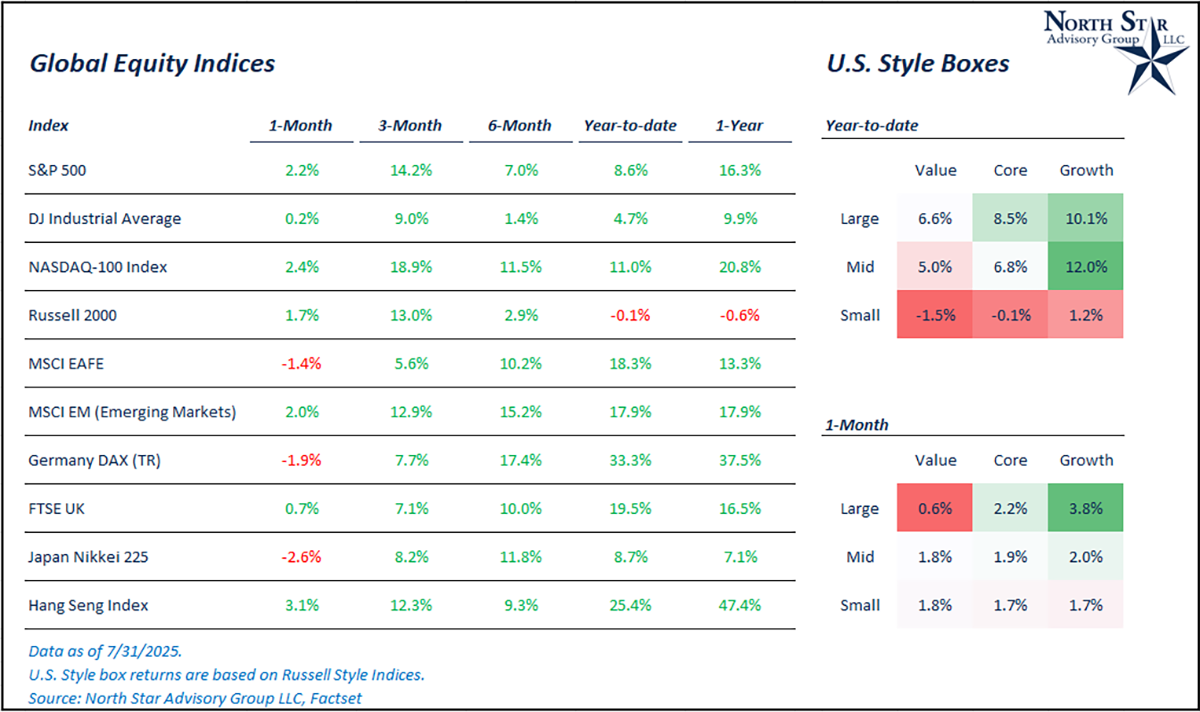

Where will the stock market go next?

Another strong month for stocks has taken various stock markets to new all-time highs across the globe. Last month, we mentioned the fact that, historically, new all-time highs following a 20% correction generally led to continued strong returns over the next year. In just one month after hitting new highs in June, this trend is off to a strong start. The S&P 500 rose 2.2% in July, while the Russell 2000 rose 1.7%. International markets pulled back a bit in July as the dollar reversed some of its downtrend in the short term. The MSCI EAFE index fell 1.4% in July, although the index is still more than double the returns of the S&P 500 for the entire year of 2025 (+18% vs +8.5%). Emerging Markets were positive in July rising by 2%, particularly led by Chinese/Hong Kong markets. These stocks gained traction following a slew of positive economic data reports coming out of the country (June’s data released in July).

Looking within the U.S. market, growth stocks have experienced a very strong rally following the April 9th pause on reciprocal tariffs. Growth stocks (+10%) are now leading value stocks (+6.6%) for the year, despite value outperforming in Q1. We’d caution investors from passively chasing this trend in the near term as relative valuations have stretched to levels where previous growth stock pullbacks occurred. While we are long term believers in AI globally, we continue to be disciplined in our approach to valuation, growth and assessment of competitive advantages when making investments across this theme.

We continue to stress the importance of diversification for client stock portfolios across geographies and styles. We also continue to favor active management over passive management due to structurally unfavorable concentration in certain market indices.

We are passionately devoted to our clients' families and portfolios. Contact us if you know somebody who would benefit from discovering the North Star difference, or if you just need a few minutes to talk. As a small business, our staff appreciates your continued trust and support.

Keep sending your questions for a chance to be featured in next month’s Timely Topics.

Best regards,

Mark Kangas, CFP®

CEO, Investment Advisor Representative

Brian Duffield, CFA®

Co-Portfolio Manager & Market Strategist