Each month we ask clients to spend a few minutes reading through our newsletter with the goal of raising their investor IQ. In April's Timely Topics, we’re highlighting a new free premium app designed to combat inflation and providing an in-depth analysis of various markets amidst recent volatility.

- Cut costs and combat inflation: NSAG brings you Monarch Money for free!

- A return to normal

- Where’s the bottom?

- FOMC Recap

- Investing at the peak of the tech bubble

- Where will the stock market go next

Cut costs and combat inflation: NSAG brings you Monarch Money for free!

Clients are expressing concerns that tariffs could increase the cost of goods, potentially driving up overall prices and exacerbating inflation on everyday products. NSAG is thrilled to announce that it is now offering Monarch Money, a cutting-edge expense tracking app, free of charge to our valued clients.

Monarch Money’s all-in-one financial dashboard consolidates all your financial accounts—bank accounts, credit cards, loans, real estate, automobiles and investments—into a single, easy-to-use platform. Essentially, it creates a clear real-time overview of your entire financial picture, that both you and NSAG can access.

- Expense analysis and tracking: Monarch categorizes your expenses and provides insights into spending patterns, helping you identify areas to cut costs and save more effectively.

- Integration: Over the last few months, NSAG built an integration to effortlessly transfer real time client expense data from Monarch Money into NSAG’s proprietary retirement planning software.

- Budgeting made simple: The app allows you to create personalized budgets, track your expenses in real-time, and stay on top of your financial goals without hassle.

- Goal setting and progress tracking: Whether it’s saving for a vacation, paying off debt, or building an emergency fund, Monarch helps you set and track progress toward your financial goals.

- Collaboration features: For couples or families, Monarch enables collaborative budgeting and planning, ensuring everyone stays on the same page financially.

- Customizable financial plans: With tools to create tailored financial plans, you can adapt to changes in your financial situation, like inflation or unexpected expenses.

- Secure and private: Monarch prioritizes data security with bank-level encryption, so you can trust that your financial information is safe.

These features make Monarch Money a powerful tool for reducing expenses, combating inflation, identifying reoccurring expenses, planning for the future and navigating financial challenges with confidence.

With NSAG & Monarch Money, you can take control of your financial future and navigate budget challenges with confidence.

More about Monarch Money

Monarch Money helps combat inflation by empowering you to take control of your finances and make informed decisions to offset rising costs. After months of development and beta testing with clients, NSAG is proud to provide this powerful tool as part of our mission to deliver personalized financial solutions. NSAG’s multi-year investment into this initiative underscores our commitment to empowering clients with tools to achieve financial clarity and resilience.

For more information, reach out to North Star Advisory Group.

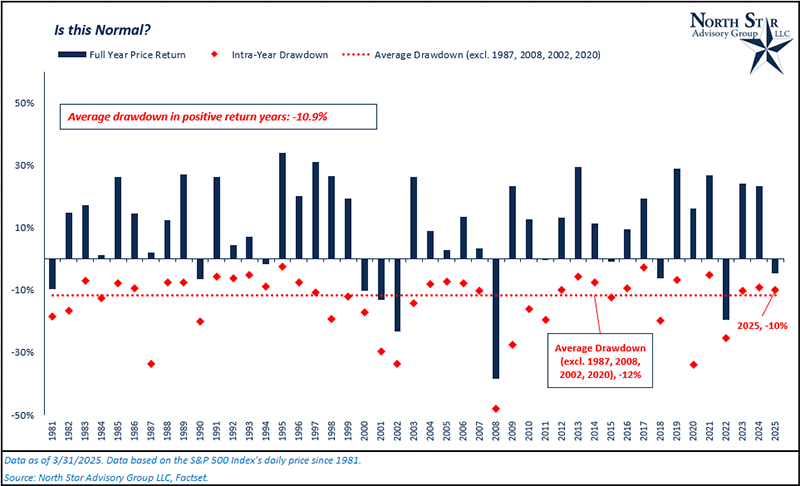

A return to normal

On February 19, the S&P 500 Index made an all-time high intra-day at 6,147. Subsequently, the index experienced a drop of 10% through 3/13/2025. For someone who only checked news headlines, social media chatter or prevailing market sentiment, they might’ve thought we experienced an “2008 level” recession. In reality, this 10% drawdown was not only normal, but it was expected. Since 1980, the average annual intra-year drawdown for the S&P 500 is -12%. This average excludes the drawdown years of 1987 (Black Monday), 2002 (Recession/Tech Selloff), 2008 (Housing Crash), and 2020 (Covid). Additionally, we calculated what the average drawdown was just for the years in which the S&P 500 finished with a positive return. Still, the average drawdown was -10.9%. So, the data is not skewed, and it actually tells us that we should expect these types of volatile moves on an annual basis. This is why NSAG often reminds clients that a 7-10% pullback is on his annual “to do list” for a healthy market.

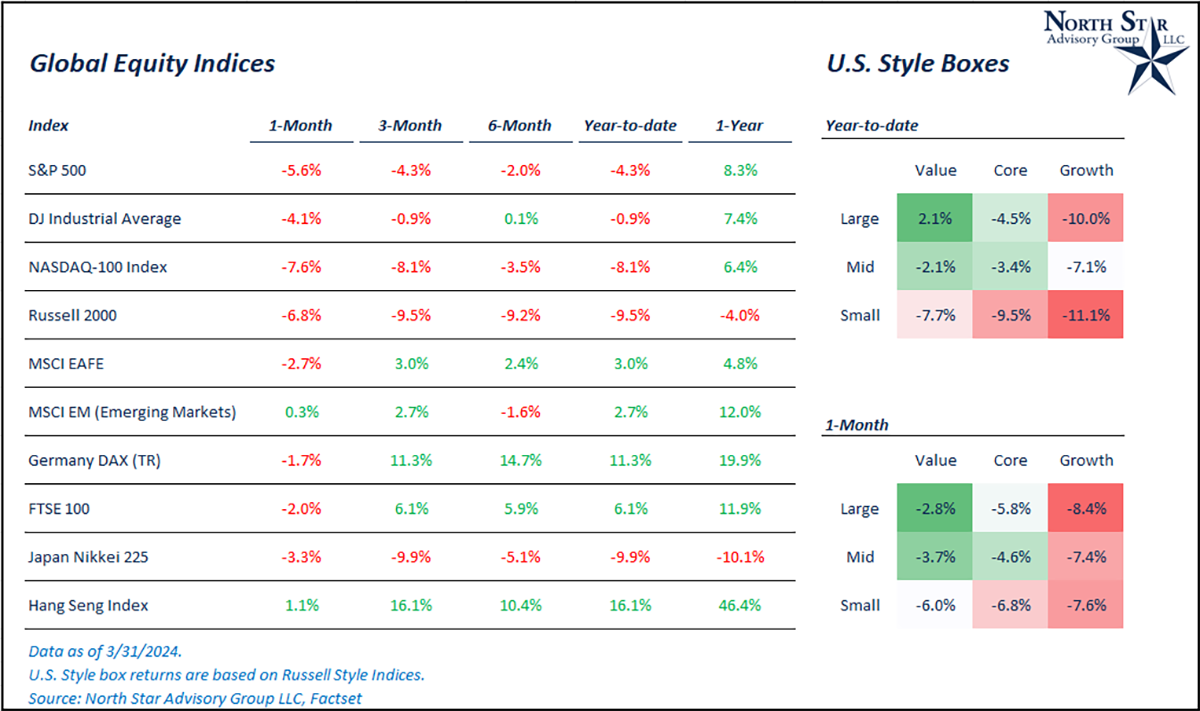

During this same time frame (2/19/2025 – 3/13/2025), international markets posted either flat or positive returns. Europe was up by 2.7%, China was up 3.5%, and Japan was down only 0.5%. Investors with globally diversified portfolios weathered this drawdown better than investors who have been concentrated in U.S. stocks, in particular those who are concentrated in U.S. large cap technology. The “Magnificent 7” (Microsoft, Amazon, Meta/Facebook, Apple, Alphabet/Google, Nvidia & Tesla) was down 14% during this timeframe.

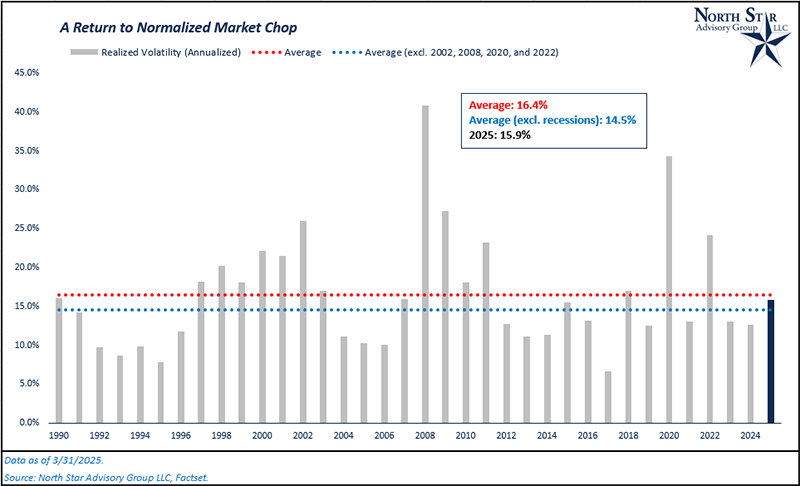

Based on headlines, sentiment and chatter, why did this normal drawdown feel so psychologically painful? If we look back on the last two years, annual volatility was lower than historical averages. This year, volatility returned to being in line with annual averages (excluding years with a recession). Given the market experience in 2023 and 2024, a return to “normal” volatility likely felt worse for investors who had a recency bias and became accustomed to the low volatility environment of the past two years.

Volatility is a measure of the variability of daily percentage changes in stocks. More days of larger percentage moves (in either direction) are typically evidenced by higher overall volatility numbers. Average annual volatility since 1990 is 16.4%.

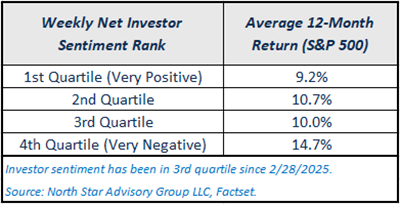

As the stock market ebbs and flows, panicking is not going to be an optimal long-term strategy. Future returns and investor sentiment have generally been negatively correlated over time. As of 3/31/2025, the index was still ~8.7% off its all-time high.

The inverse relationship of sentiment and forward returns lead to one of Warren Buffett’s most famous quotes, “Be fearful when others are greedy and greedy when others are fearful.”

Where’s the bottom?

The recent market correction was sparked by a barrage of new tariff plans to be implemented by the Trump administration this year, with particular focus to the reciprocal tariff plans that go in effect on April 2. The initial reaction, as evidenced by market movements, is that these plans will slow earnings growth in the near term as companies scramble to re-align their supply chains. So far for the year, the S&P 500’s 2025 earnings estimates have been revised down by only 1%. The bulk of the correction has come from valuation compression. So, the market has already discounted a near-term earnings slowdown and will likely chop around these price levels for the next few weeks until we are well into the Q1 earnings season. Hearing from management teams and their expectations for profitability will help the market to gauge whether earnings expectations need to be pulled down further (or not at all).

There is also a scenario out there known as the “Trump Put.” This scenario refers to the chance of reductions/deals being made around tariffs. Ask for X and settle for Y. This scenario is still probable in our view, especially given all the new talking points/quotes that have been coming out of the administration during the last week of March.

A few of these talking points include:

- “Tariffs will not be additive.” – Bessent

- “There will be flexibility.” – Trump

- “May exclude countries who we currently have a trade surplus with.” – Trump

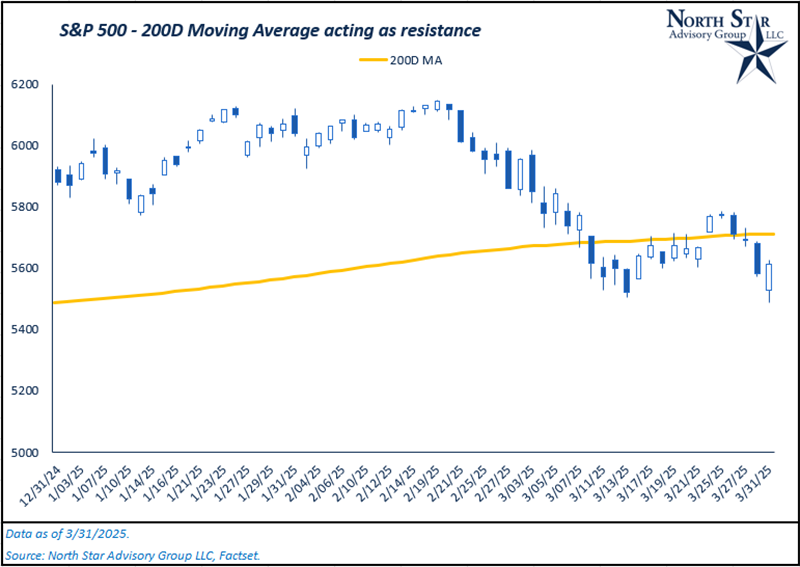

From a technical perspective, the S&P 500 had been feeling resistance right around its 200-day moving average price. Intra-day, the index had retested this average three times in March, which were promptly rejected. Once the aforementioned quotes began rolling out, the market had a string of positive days, and the index reclaimed its 200-day level. Ultimately, this was short lived as stocks fell back below this level after a 25% auto tariff was announced and the CPI print from earlier in March was revised down by 0.4% on 3/28/2025. The 200-day moving average will be a key metric to identify support and resistance levels for the stock market in the near term.

Since 1980, there have been 22 instances of a 10% or more drawdown. Eleven (50%) of these drawdowns turned into 15% corrections, while 6 (27%) of these drawdowns turned into bear markets (Greater than -20% correction).

FOMC Recap

With potential trade wars brewing and concerns over the economy growing, we thought it would be beneficial to recap the most recent Federal Open Market Committee (FOMC) meeting to get a pulse on how Federal Reserve policy makers are taking in the recent changes to our economy. This meeting took place on March 18 and 19, 2025.

From an actual policy standpoint, the FOMC decided to hold the policy rate steady at a range of 4.25% – 4.50%. This decision was expected by the market. In previous meetings, Jerome Powell had stated that he believes the current policy rate is above the “neutral” rate, meaning that the committee is sticking to their restrictive policy in terms of rate levels. Additionally, the committee still expects to make two more 0.25% cuts by the end of 2025, which is unchanged from their prior meeting.

A bigger change came from their balance sheet reduction policies. Previously, the Federal Reserve had a monthly cap of $25 billion in treasury redemptions. This cap serves to reduce the Federal Reserve’s balance sheet (aka “reduce the money supply”) which helps to combat high inflation in the economy. They have been shrinking their balance sheet since 2022. During the March meeting, officials decided to reduce this cap to $5 billion per month. While it is still restrictive in absolute terms, it is an expansionary policy move relative to where they were prior. Reducing the pace of money supply shrinkage may put further pressure on the U.S. dollar and subsequently reduce the currency headwind of investing in international stock markets. On the other side of the coin, international investors who own U.S. stocks may start to feel the headwind of a weakening dollar.

When it comes to tariffs, the FOMC, like the rest of the market, appears to still be in a “wait and see mode.” As we’ve discussed ad nauseum, there is a lot of uncertainty surrounding where the Trump 2.0 tariff agenda will actually land. During the post-meeting press conference, Jerome Powell stated that he, “doesn’t know any forecaster who is confident in their current estimates.” With that said, the FOMC did adjust their economic forecasts, reducing 2025’s real GDP growth rate from 2.1% to 1.7%, and increasing their PCE inflation expectations from 2.5% to 2.7%. Jerome did state that they view the inflationary impacts from tariffs as “transitory,” a word that may give investors PTSD from the post-Covid era. As inflation was ramping in 2021, inflation was mistakenly thought of as “transitory” due to supply chain shocks from Covid lockdowns. In reality, the money supply is what truly drives inflation rates in an economy.

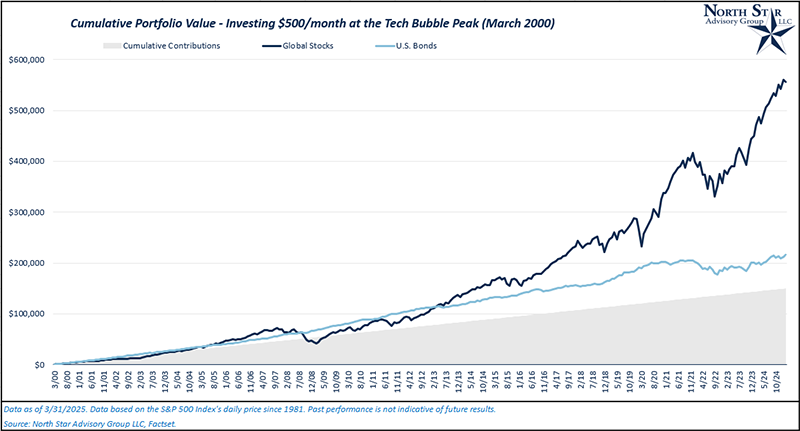

Investing at the peak of the tech bubble

The "Lost Decade" for the S&P 500 refers to the period from 2000 to 2010-11, when the S&P 500 index experienced around zero to negative growth due to a series of economic events, including the bursting of the dot-com bubble, 9/11 terrorist attacks and the 2008 financial crisis. After peaking in 2000, the S&P 500 endured significant volatility, with major declines followed by brief recoveries, but by the end of 2010, the S&P 500 was essentially at the same level as it had been a decade earlier. Investors during this time faced stagnant returns, highlighting the challenges of navigating through prolonged bear markets and economic turmoil. This period serves as a reminder of the unpredictability of financial markets and the importance of long-term perspective in investing.

With the rise in AI over the past two years, we’ve heard some skeptics compare the current market environment to the tech bubble’s environment at its peak. We strongly disagree with this comparison. For reference, the Nasdaq 100 Technology Index traded at ~60 times earnings during the tech bubble peak while today it traded at ~30 times earnings. If AI related earnings were to slow significantly (like internet earnings did in 2000), the pain would not be the same solely due to starting valuations.

With that said, let’s take an imaginary time machine back to March 2000. We’re just starting our careers and adding into our 401(k)s for the next at least the next 25 years until retirement. What does history tell us that our asset allocation mix should be? 100% Stocks, 50% stocks/50% bonds, or something else? Surely it doesn’t make sense to go 100% into stocks since they were flat over the next decade, right?

By making monthly contributions into a global stock portfolio (based on the MSCI All Country World Index) for the next 25 years (2000-2025), we finished with ~$556k in our account. This is despite riding through the volatile periods of 2000-2002, 2008, 2020, and 2022. The investor who took the ultra-conservative route by investing 100% into bonds (based on the Bloomberg Aggregate U.S. Bond Index) finished with ~$216k.

What is the key lesson to be learned from this historical scenario? Recognize that time is your most valuable asset.

Where will the stock market go next?

March was challenging for stocks as the market anticipated a higher chance of recession due to global trade war threats. Initial market reactions to the barrage of tariff headlines were an increase in inflation expectations and a decrease in real growth expectations. In tandem, these revisions have the market concerned about potential stagflation in the economy. Stagflation refers to slower growth coinciding with increasing inflation. During March, the S&P 500 fell 5.6%, bringing its year-to-date performance to -4.3%. Additionally, developed international and emerging markets felt some pressure in the second half of the month, bringing their respective monthly returns to -2.7% and 0.3%. International markets are still showing relative strength versus U.S. markets for 2025.

Within the U.S., value stocks are outperforming growth stocks. Mega-cap growth names have been especially hurt during this drawdown. The average “Magnificent 7” stock is down 24% peak to valley in 2025, while the S&P 500 is at an 8.7% drawdown. Despite negative U.S. performance, breadth has re-entered the market as more than 60% of S&P 500 constituents are outperforming the index level return in 2025. While U.S. markets remain volatile in the coming months, we expect that international markets will continue moving higher in 2025.

As we’ve discussed, stock markets are likely to continue their volatility around current levels until we are well into Q1 earnings season. After a 10% correction, market participants are likely in a “wait and see” mode on tariffs and their true impact to corporate earnings. The “Trump Put” is also still in play. Since tariff policy decisions truly heated up in the back half of February, there have been a flurry of announced investments into U.S. manufacturing across multiple industries. We’ll likely see more of these announcements if the Trump 2.0 administration continues their deal making/concession process with specific countries one by one.

A few of the companies who have recently announced large investments into the US are: Apple, Taiwan Semiconductor, GE Aerospace, Hyundai, ArcelorMittal, Diageo, Samsung Electronics, LG Chem, Ford Motor. If announcements like these continue, it could be a further signal that the “Trump Put” is happening somewhat behind closed doors.

We are passionately devoted to our clients' families and portfolios. Contact us if you know somebody who would benefit from discovering the North Star difference, or if you just need a few minutes to talk. As a small business, our staff appreciates your continued trust and support.

Please continue to send in your questions and see if yours get featured in next month’s Timely Topics.

Best regards,

Mark Kangas, CFP®

CEO, Investment Advisor Representative