Each month we ask clients to spend a few minutes reading through our newsletter with the goal of raising their investor IQ. We are focusing November’s Timely Topics on options-based investment strategies and the parallels between our current bull market versus historical bull markets. We also have some exciting news to share for the firm!

- Covered call strategies (income tradeoff)

- Historical performance of covered call strategies

- Bull markets

- Presidential election

- NSAG News

- Where will the stock market go next

Covered call strategies

Clients have shown interest in options-based investment strategies. We aim to educate them on the benefits and risks of these strategies, which are typically used to generate income and minimize downside risk.

There are a wide variety of investment products available that use options-based strategies, and they can become complicated to understand. So, we will review one of the simplest and most popular forms of options-based investment strategies, the covered call. You’ll typically see these strategies deployed in either an ETF or mutual fund product with enhanced income, buy-write, or option income in the strategy’s name.

What is a covered call? This strategy involves two trades: buying stock and selling a call option on the same stock.

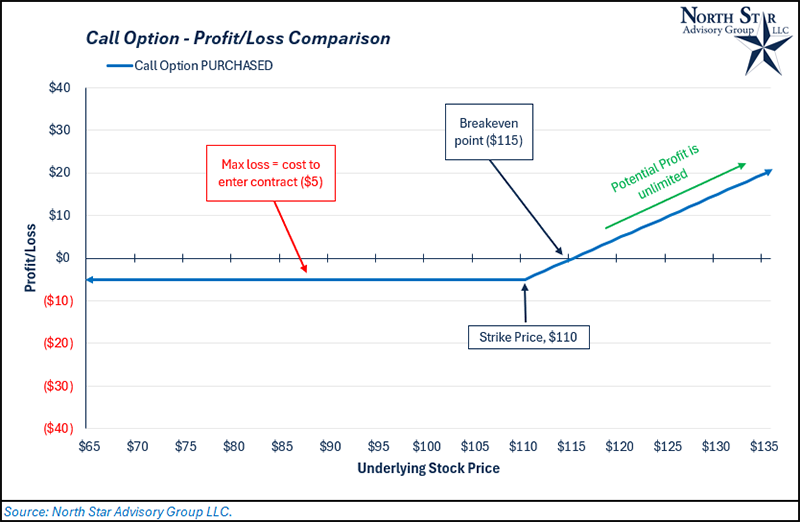

What is a Call Option?

Before we get into the covered call example, we need a better understanding of what a call option is. Think of them as a contract that allows the buyer of that contract to purchase a specified asset (stock, bond, etc.) at a set price, also known as the strike price. These contracts cost money to enter and have set expiration dates.

Let’s say an investor pays $5 for a call option on XYZ stock with a strike price of $110 and it expires in 90 days. That investor now has the right to buy XYZ stock for $110 within the next 90 days. So how does this investor profit? They’ll need the share price of XYZ to increase to at least $115 to break even, that way they can buy XYZ for $110 and immediately sell XYZ stock in the market for $115, covering the cost of the contract ($5). The potential upside for the buyer of the contract is theoretically unlimited (the same as owning any stock). But again, there is a finite timeframe (90 days in this case) and if XYZ doesn’t move in the investor’s favor prior to expiration, the contract expires worthless, and the investor experiences a $5 loss due to the cost of the call contract.

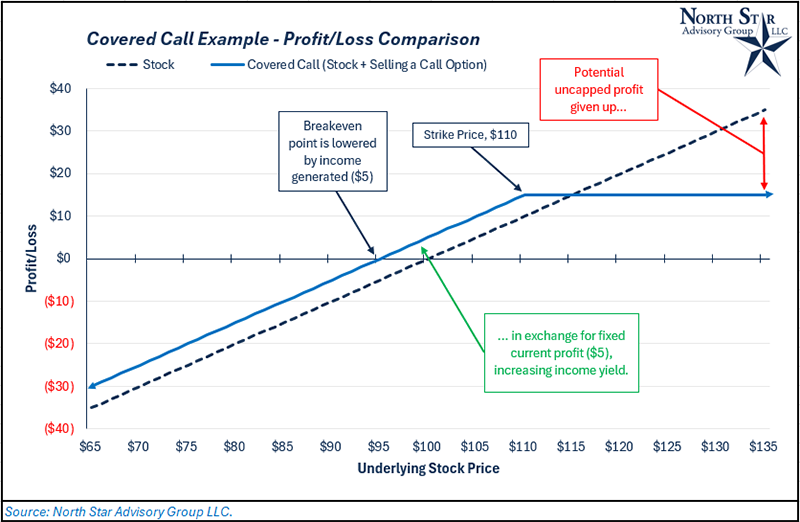

Covered call

Now that we know the payout structure of buying a call option, we have to flip this structure on its head. Refer back to the two trades to create a covered call: buying stock and SELLING a call option on the same stock. We are no longer buying that same call option contract; we are selling it (or shorting it). Step one is simple… buy XYZ stock. The buyer now has a linear profit/loss chart (dark blue dotted line in the chart below). Our potential gain is unlimited, and our potential loss is the share price (buyer would lose should the stock goes to zero).

In step two, we overlay the shorted call option. Instead of paying $5 for this contract, we are selling it for $5 of income, hence enhanced income or option income. By taking this income, we are now obligated to sell the XYZ stock we just purchased for $110 to the buyer of that contract. Our potential profit is now capped at a share price of $110, because at any level above this, the buyer of the contract will force us to sell for $110. Assuming the original share price of XYZ was $100, our max profit is $15. Income of $5 + a capital gain of $10 ($110 sale price + $5 contact price - $100 initial purchase). The additional income gives the investor some room to breathe in terms of their breakeven point, shares can fall from $100 to $95 before having a negative profit. Overall, what has the investor done by taking this covered call position? In simplest terms, they’ve exchanged unlimited upside for current income, reducing the risk in their portfolio to an extent.

Historical performance of covered call strategies

We understand that the strategy may be complex, and we are happy to set up a call to explain it further. As these products advertise higher income to investors, it is crucial to understand the mechanics behind this income and what investors might be sacrificing in return.

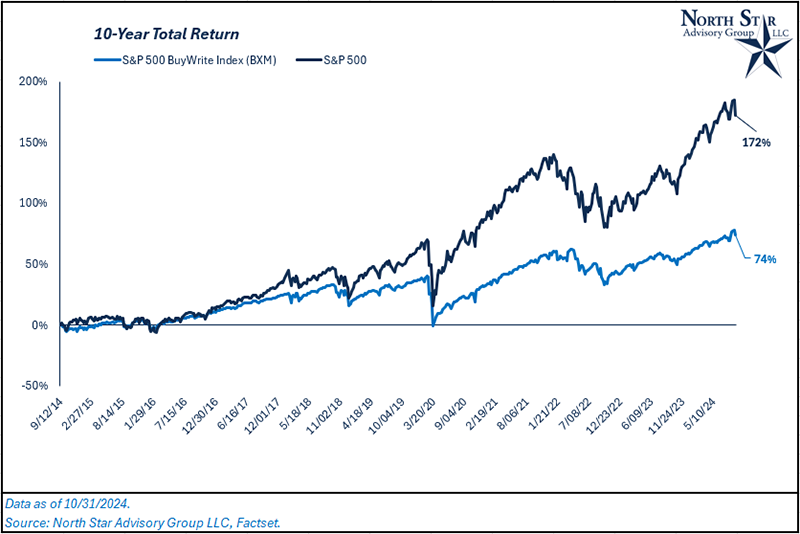

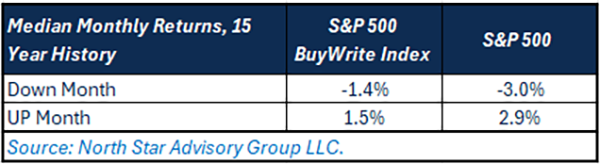

Let’s now turn to the actual performance of some of these products. While several clients tend to be intrigued by the higher income that is being marketed, we want to focus on the total return for an investment, not just the income component. Total return = capital appreciation + income.

The most common index that tracks this type of strategy is the CBOE S&P 500 BuyWrite Index. This index tracks the performance of buying the S&P 500 and writing calls against the S&P 500 each month. Cumulatively over the past 10 years, this strategy has severely lagged the S&P 500 Index.

What is causing this underperformance? By capping an investment’s upside in exchange for income, the strategy will lag when markets are up and outperform when markets are down. With that in mind, we must remember that stock markets have an upward bias (compensation for taking market risk) over the long run. On average, the S&P 500 is positive 7 to 8 out of 12 months in any given year. If an investor sits in one of these strategies over long periods of time, they will be underperforming on a consistent basis.

As of October 2024, there are currently 103 different mutual fund and ETF products that employ these covered call strategies. They are classified by Morningstar as option income. Today, their combined assets under management (AUM) are ~$82 billion. Just five years ago, there were 18 of these products available, with a combined AUM of ~$5.8 billion.

Finally, covered calls can be tax inefficient due to the nature of the income generated and the potential for short-term capital gains. When an investor sells a call option, the premium received is considered income and is taxed at the investor's ordinary income tax rate. If the call option is exercised, the investor may also face short-term capital gains taxes if the underlying stock is sold within a year of purchase. This can result in a higher tax burden compared to long-term capital gains, which are taxed at a lower rate. Additionally, frequent trading associated with covered call strategies can lead to higher transaction costs and further tax implications.

Please feel free to reach out to our team any point to discuss options strategies in greater details.

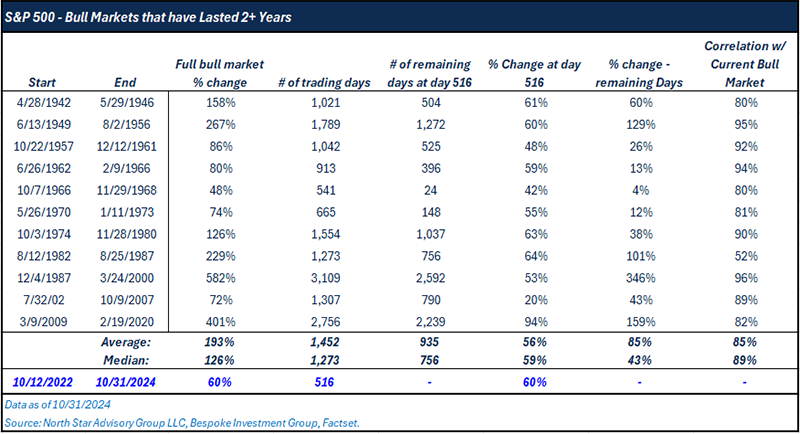

Bull markets

The end of October signifies just over two years of the current bull market for stock markets. We aim to compare the last two years with other historical bull markets that also persisted for at least two years. Since the Great Depression (excluding the current bull market), there have been 12 other bull markets lasting a minimum of two years. These time periods are identified by a 20% or greater rally in the S&P 500 Index, followed subsequently by a 20% or greater decline, indicating a bear market.

As forward-looking market participants, we want to focus on the time period following the first two years of each bull market. Using median values, bull markets had 756 trading days remaining (or ~3 years) in their run after the two-year mark was crossed. In the first two years, the median change for the S&P 500 was ~59%, and the median remaining change was ~43%. This data proves that the early years of a bull market (first two) tend to contribute more toward the bull market’s total return in relatively less time. Economically, this makes sense as stock markets tend to rally harder when they come off the lows of a bear market. The majority of the highest daily % changes (best days to be invested) for the S&P 500 come during a bear market.

Focusing on the bull markets that began in 1956 and 1987, both have a high correlation to the current bull market’s first two years and the majority of their returns came in the latter years of each run. While correlation does not imply causation for the current market, it is an interesting observation.

From 10/12/2022 to 10/31/2024, the S&P 500 is up 60%, and while nothing is guaranteed, history tells us that there is a likelihood for strong returns to continue. A meaningful tech slowdown, particularly in artificial intelligence spending, or a reduction in government spending (shift towards a restrictive fiscal policy to manage government debt) are likely the two biggest risks that could cause an end to this bull run.

Presidential election

We wanted to outline potential short-term market moves that could come from either outcome of the election this month. While each candidate has discussed a range of proposed policy changes, we highlight a few areas that have driven recent client conversations.

Trump victory

- Corporate tax cut from 21% to 15% -> Short-term boost to earnings expectations for public stocks broadly.

- Tariffs uncertainty -> Likely to see increased volatility for international stocks, particularly in Canada, China, United Kingdom, Mexico and Japan (our top trading partners).

- Industries that could perform well: technology and financials (expectations of less regulation), defense contractors (increased military spending), and cryptocurrencies (Trump has embraced this community on the campaign trail). The energy sector could see a short-term pop, although we already have an oversupply of energy, and further increases in supply could put significant pressure on oil and natural gas prices, hurting long-term profitability for these businesses.

Harris victory

- Corporate tax hike from 21% to 28% -> Short-term detraction from earnings expectations for public stocks broadly.

- Tariffs uncertainty -> While democrats are also pro-tariff, they are not as aggressive, and you could see a short-term pop for international stocks.

- Industries that could perform well; clean/sustainable energy (increased demand for the electrification of the economy via clean sources combined with increased regulation on the oil and gas industry), healthcare services (expansion of the affordable care act), cannabis (expectation for legality on the federal level), and cybersecurity (Harris has emphasized the need for improving national cybersecurity).

While the President may have the executive power to enact certain tariffs on his/her own, each candidate does not have the power to enact all of these changes on their own. They need new policies to be approved by Congress and the Senate. With a high likelihood of Democrats or Republicans retaining control of at least one of the three branches, we are less likely to experience significant policy swings.

Regardless of who claims their victory on November 5, small cap stocks may rally and outperform large cap stocks between the election and inauguration day. Over the past 10 election cycles, small cap stocks have outperformed large cap stocks by an average of 5.2% between the end of October and the end of January (the following year) in election years.

NSAG News

North Star Expands

Erik Keister channeled his inner child and acted like the Kool-Aid man as he literally broke through the wall into our new office space (directly adjacent to our existing office). Click HERE to watch a composite video of Erik’s contribution to our construction. It is worth a chuckle.

The expansion has more meaning than many know. In 2013, Mark started North Star in a small office down the hall from our current space. In 2018, NSAG outgrew the original office and moved one suite over into our current bigger office. In 2024, Keister’s breaking though the wall literally rejoins our new and old offices. While it was always part of Mark’s plan to expand back into NSAG’s original space, it is a surreal experience to have that moment come true six years later.

If you couldn’t tell… long-term planning has always been part of our DNA.

The additional space will allow NSAG to add staff as needed to maintain high levels of client service and satisfaction. We are also adding and enhancing technology resources to support our collaborative in-office working environment.

Another North Star champ In October, Brian's sand volleyball team won the Razzles 1st-place co-ed championship. Razzles is well-known on Cleveland's west side for its popular outdoor leagues. Over the summer, 15 co-ed teams played weekly, culminating in the October tournament. Brian’s team, seeded 4th, fought to the championship game where they needed two straight wins—and they got the sweep! It's fortunate Brian knows how to sweep; we keep finding sand around his desk in the office.

Where will the stock market go next?

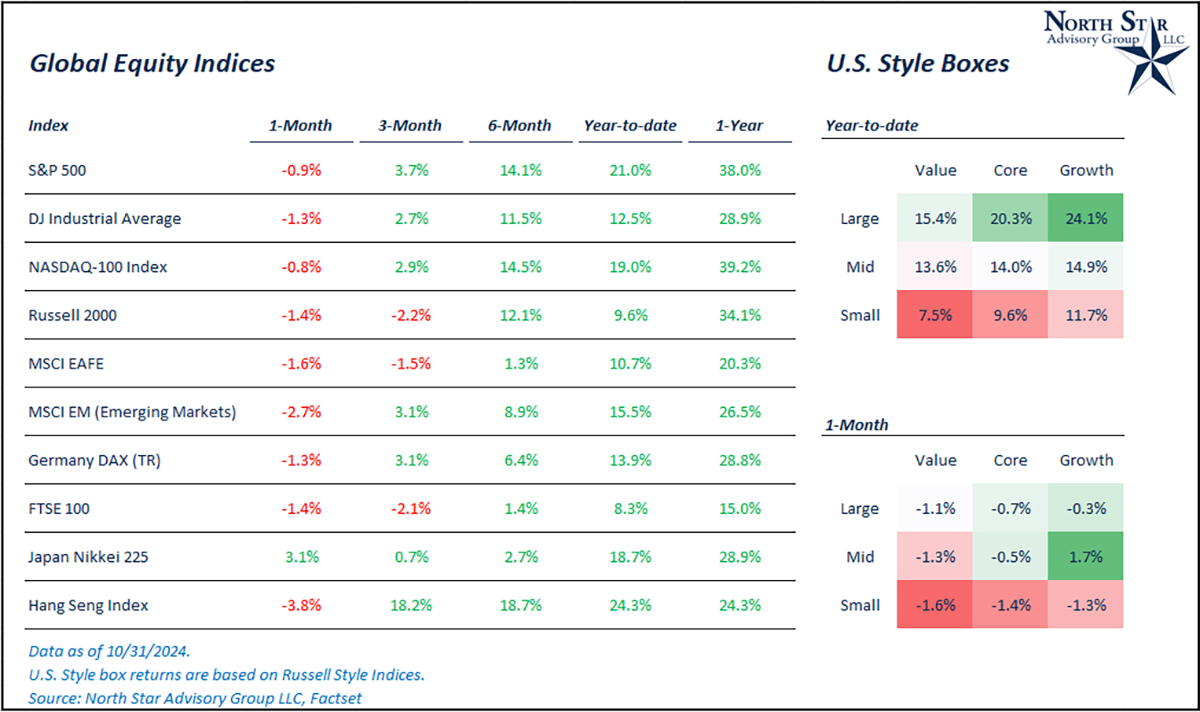

Through October, the S&P 500 fell 0.9%, sticking with the historical trend of a negative October preceding an election. The majority of the index’s fall in October came within the last two days of the months, where we saw some mega-cap technology companies report their quarterly earnings. For the most part, these companies posted positive earnings surprises (actual EPS > estimated EPS), but their guidance numbers did not impress the market (guidance refers to the company’s internal sales and profit expectations in future quarters and years).

The technology sector is currently trading at ~27x next 12 months’ earnings. For reference, the sector traded at ~28x in Q3 2020 when the sector was experiencing high growth rates and near-zero interest rate levels. This leads us to believe that the sector is “priced for perfection,” and if we don’t receive “perfect” guidance figures from major tech companies, there is a chance for a selloff in the short term. This experience is what weighed on the S&P 500 in the final days of October. The majority of the technology sector is yet to report Q3 earnings and guidance expectations.

Outside of technology, we are well passed the early innings of the third quarter earnings season, with 338 out of 504 S&P 500 constituents reporting quarterly results in October. So far, 257 out of 338 companies reporting earnings have had positive surprises, which is a positive surprise rate of 76%. In aggregate, these 338 companies reported EPS that was 4% higher than expectations, based on the median value. Overall, the positive earnings trend should continue to lift stock markets to new all-time highs.

Digging deeper into these earnings numbers, 63 companies in the financial sector reported their quarterly results at a positive surprise rate of 83%. Additionally, 61 companies in the industrial sector have reported their quarterly results with a positive surprise rate of 74%.

Elsewhere in the world for October, emerging markets fell by ~2.7%, small cap stocks were down ~1.4%, and international developed markets were down ~1.6%. It is important to note that emerging markets and small cap stocks had a strong Q3 performance of 6.8% and 9.3%, respectively.

Lastly, the 10-year yield jumped from 3.78% to 4.28% in October. This violent reversal in interest rates comes off the back of the Federal Reserve making their 0.50% rate cut in September. Following this cut, we’ve received a slew of positive economic data releases which has increased the probability of a soft-landing, causing investors to rotate dollars out of bonds and back into stocks.

We are passionately devoted to our clients' families and portfolios. Contact us if you know somebody who would benefit from discovering the North Star difference, or if you just need a few minutes to talk. As a small business, our staff appreciates your continued trust and support.

Please continue to send in your questions and see if yours get featured in next month’s Timely Topics.

Best regards,

Mark Kangas, CFP®

CEO, Investment Advisor Representative