Each month we ask clients to spend a few minutes reading through our newsletter with the goal of raising their investor IQ. Heading into early Fall, we are focusing October’s Timely Topics on the recent CPI data, the expected impact of rate cuts on the market, volatility during election cycles, and what to do to prevent security breaches.

- Inflation update

- Onset of a rate cut cycle

- Elections, wars, and civil unrest

- Security threat

- Where will the stock market go next

Inflation update

Inflation came in at 2.50% year-over-year for the month of August. This marks two consecutive months of sub-3% year-over-year readings on CPI. It also represents five consecutive months of disinflation (positive but decreasing) year-over-year readings since March.

Throughout 2024, the labor market has begun normalizing and unemployment has slightly ticked up from historically low levels. When you combine these trends with the consistent disinflation we are experiencing, it is clear to us that now is an appropriate time for the Federal Reserve to begin their rate cutting cycle. In fact, the Federal Reserve made their first rate cut of this cycle on 9/18/2024, lowering their target policy rate by 0.50% to a range of 4.75-5.00%.

As of now, it appears that the Federal Reserve has accomplished their goal of lowering inflation while not blowing up the labor market and throwing the country into a recession. This is known as a “soft-landing.” We believe that there is a strong case to cut rates at a faster pace than what the committee is signaling to. We draw this conclusion from diving deeper into the most recent inflation data release.

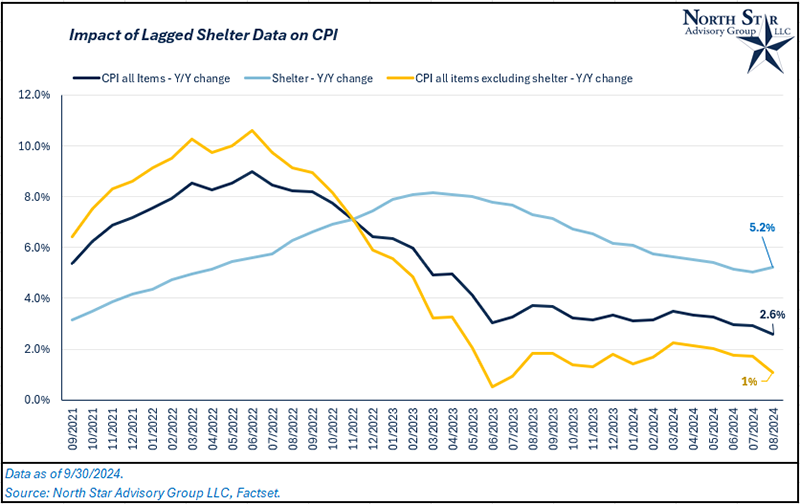

In a previous Timely Topics article (November 2023), we discussed the impact of lagged shelter data on the aggregate CPI Index itself. Shelter makes up a large portion of the aggregate CPI Index, given that this is generally one of the larger expenses for a majority of the population. Unlike other expense categories (gas, food, etc.), shelter is known to be “sticky” meaning that the data is generally lagged and doesn’t necessarily represent what’s happening in the economy in real-time. There are a couple reasons for this; rent prices generally only reset once per year (at lease expiration), and typically the rent prices surveyed are based on available units not occupied units. On top of the lagged nature, rent price calculations within the CPI index are known as “owner’s equivalent rent” and largely based on changes in mortgage rates. As rates increase, the cost of a mortgage increases, and therefore, so does “owner’s equivalent rent.” A large portion of the population has mortgages that are fixed and locked in with a 3-4% interest rate, so these people haven’t even experienced any of this inflation. With all of this said, let’s remove the impact of shelter on the aggregate CPI index to see where prices have been trending in the economy.

As mentioned, August 2024’s inflation reading was 2.5% year-over-year. When shelter is stripped out, that year-over-year number falls to just 1.1% (see chart below).

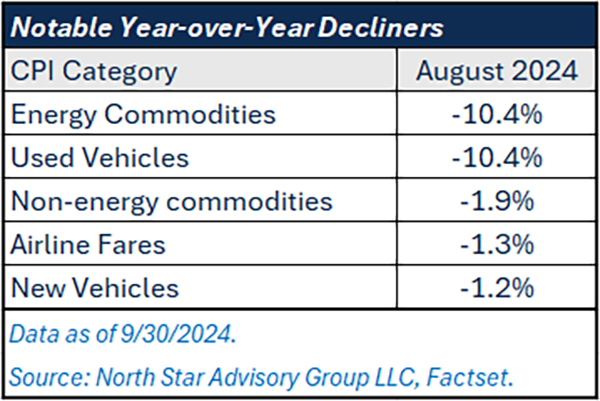

Some parts of the economy have been experiencing deflation over the past year; most notably, energy, new and used vehicles, non-energy commodities, and airline fares (see table below). After removing shelter, you’ll notice how quickly the inflation rate has fallen from its peak in summer 2022. Deflation (negative inflation rates) are not a positive catalyst for equities, real estate, and other risky assets. At the time of writing this section, the CPI data had just been released on 9/11/2024 and the market was in overwhelming agreement that the Federal Reserve was going to make their first interest rate cut. These inflation numbers led us to believe that there was a strong case to make a 0.50% cut in lieu of a 0.25% cut. One week later, on 9/18/2024, we were proven correct as the Fed opted for a 0.50% cut.

Onset of a rate cut cycle

As discussed above, on 9/18/2024, the Federal Reserve made their first rate cut since their rate hiking cycle began in early 2022. The committee voted to lower their target policy rate by 0.50% from a range of 5.25 – 5.50% to 4.75 – 5.00%. While the market unanimously expected a rate cut, the odds on 9/18 were in favor of a 0.25% move. In Jerome Powell’s post-meeting speech, he acknowledged that the committee “probably could’ve” made their first rate cut back in July, given where inflation has been trending.

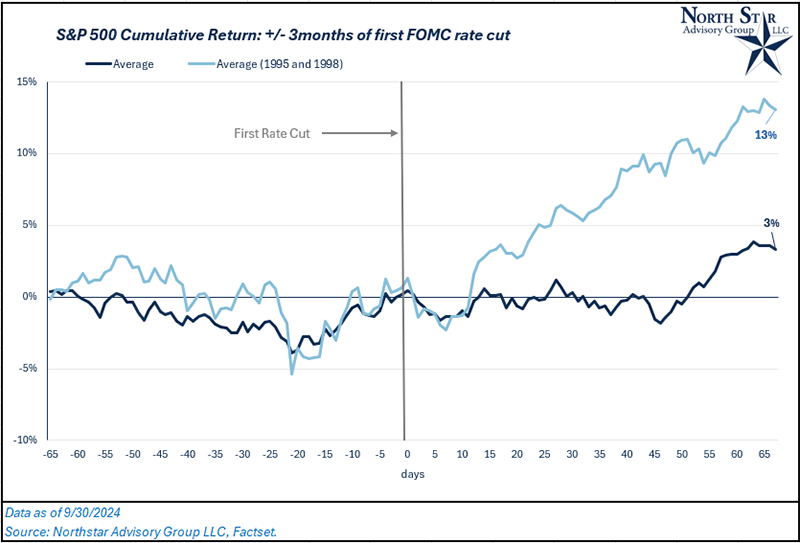

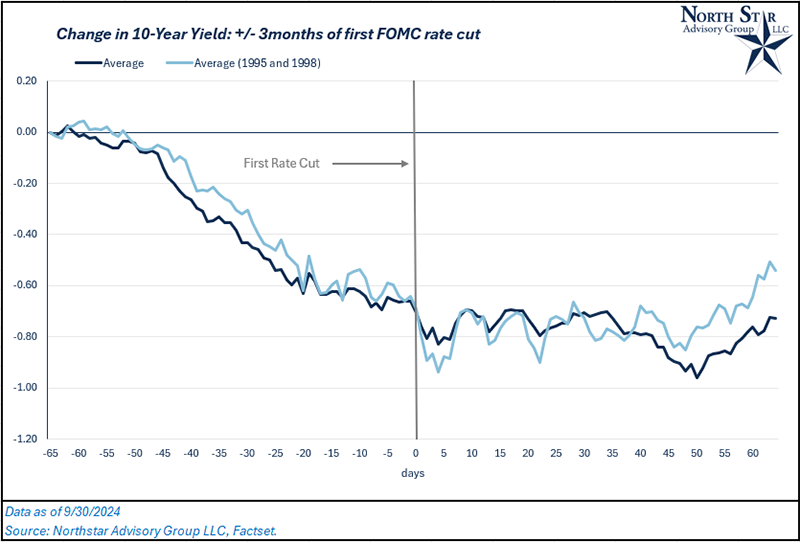

Now that the first cut has come and gone, what does that mean for the stock market? In the chart below, we examined the previous five rate cutting cycles that began on 7/6/1995, 9/29/1998, 1/31/2001, 9/18/2007, and 7/31/2019. On average, the S&P 500 posted positive returns (~3%) in the following three months after the first-rate cut was made. The majority of these returns came in the third month after the market had gone flat during the first two. Focusing on cutting cycles that weren’t followed by a recession (1995 and 1998), the S&P 500 experienced much stronger returns (+13%) in the three months following the first rate cut.

In this cycle, the stock market has positively reacted to the rate cut. From 9/18/2024 through 9/30/2024, the S&P 500 is up 1.8%. This has been fueled by the combined impact of a rate cut and subsequent positive economic data. Initial jobless claims came in less than expected for two consecutive weeks and housing sales were better than expected for both existing and new homes. This has given markets more confidence that the Federal Reserve orchestrated a soft landing by slowing inflation without crippling the economy.

Let’s now apply this same framework to the bond market. Whether we average the past five cutting cycles or just focus on 1995 and 1998, both historical period averages display a similar move in the 10-year yield. Rates tend to fall in the three months prior to the first rate cut and then go flat in the subsequent three months. For many reasons, this data did not surprise us.

Typically, the Federal Reserve “telegraphs” their interest rate movements to the market, and bond market investors price in their expectations prior to the actual cut decision. Additionally, the Federal Reserve only meets nine times per year to make policy decisions, and outside of what’s called an “emergency meeting,” the committee can’t change policy on any random day they see fit. (The last emergency meeting took place during the COVID-19 pandemic.)

As economic data comes out daily or weekly, it helps to shape the market’s expectation of what the Federal Reserve will do. For example, in July, worse than expected employment data shook both the stock and bond markets. From 7/1/2024 to 9/18/2024, The U.S. 10-year yield fell from 4.37% to 3.64% as the market had taken in this weaker economic data and predicted a rate cut from the Fed in their next meeting. Despite the data being released in July, the FOMC’s next meeting wasn’t until September. Since 9/18/2024 (the first rate cut), the 10-year yield has risen by ~15 bps to 3.8%. This movement is in-line with the market’s expectations for the economy, given that stocks have also reacted positively.

We do expect short-term treasury rates to continue falling as more rate cuts are expected throughout the remainder of the year and in 2025. These short-term rates (such as 3- or 6-month treasuries) are heavily tied to where the actual policy rate stands (in comparison to long-term rates, like the 10-year). This will affect the rate on newly issued CDs, money market funds, and other short term bond securities.

Elections, civil unrest, and wars

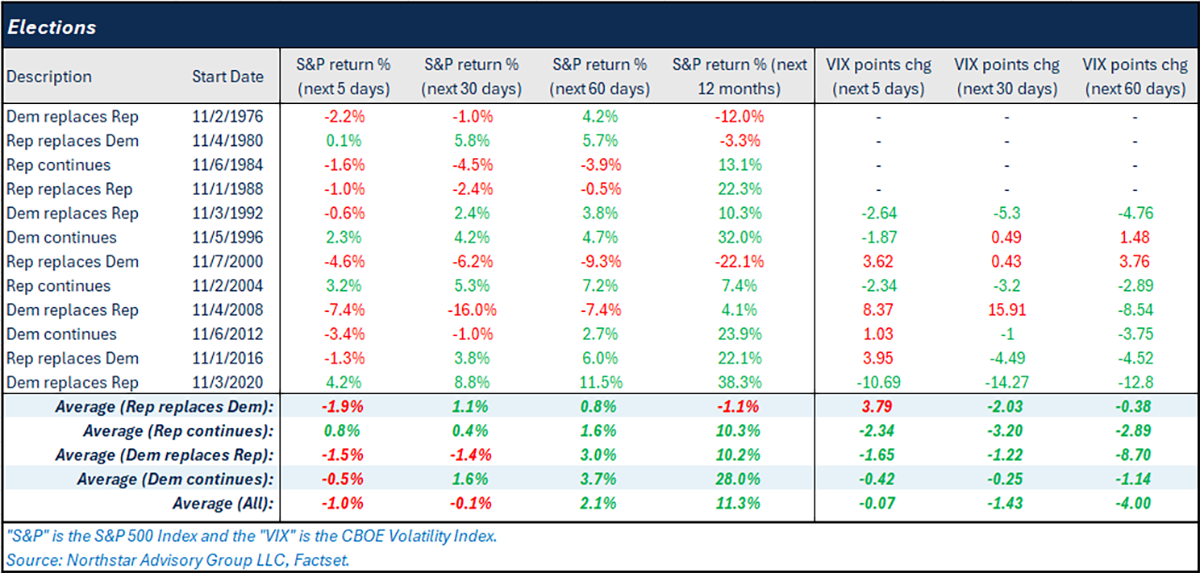

With an upcoming election that feels as politically charged as it’s ever been, many clients may find themselves uneasy about what that means for the stock market. There is a lot of uncertainty as to what major events may occur regardless of which candidate prevails in November. As students of history, we want to know the impact of these major events on the stock market. We particularly want to focus on short-term reactions to these events and news headlines to understand whether we should be expecting a spike in volatility.

Let’s start by assessing short-term market reactions following an election. On average, the S&P 500 has returned +2.1% 60 days after a presidential election takes place, while the CBOE Volatility Index (VIX) falls by 4 points. Focusing in on the two possible outcomes for 2024’s election, the S&P 500 has had positive performance (+3.7%) on average when a democrat continues to hold office while a republican replacing a democrat has typically led to lower positive performance (+0.8%) over the next 60 days. On average, the S&P 500 has been up 11.3% in the subsequent 12 months of the past 12 election cycles.

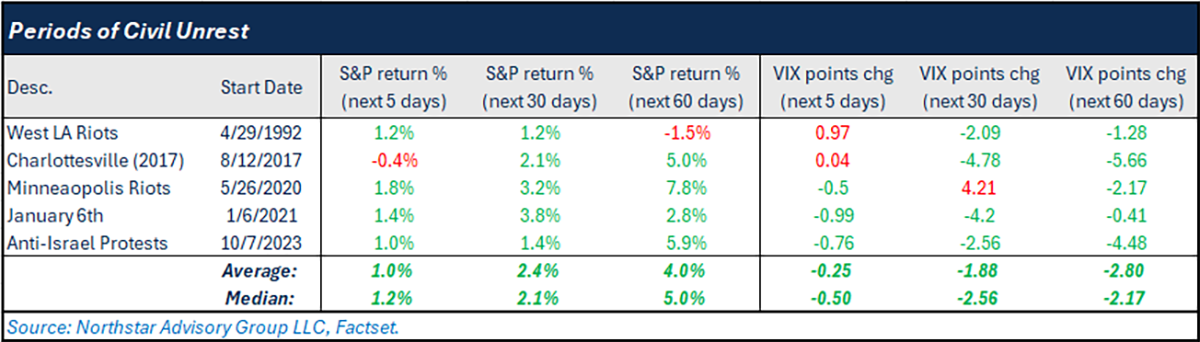

Turning our focus to periods of “civil unrest” in the U.S., have these events sent major ripples through the stock market? The answer is no. Whether we look at 5-, 30-, or 60-days post event, the S&P 500 has had positive returns on average.

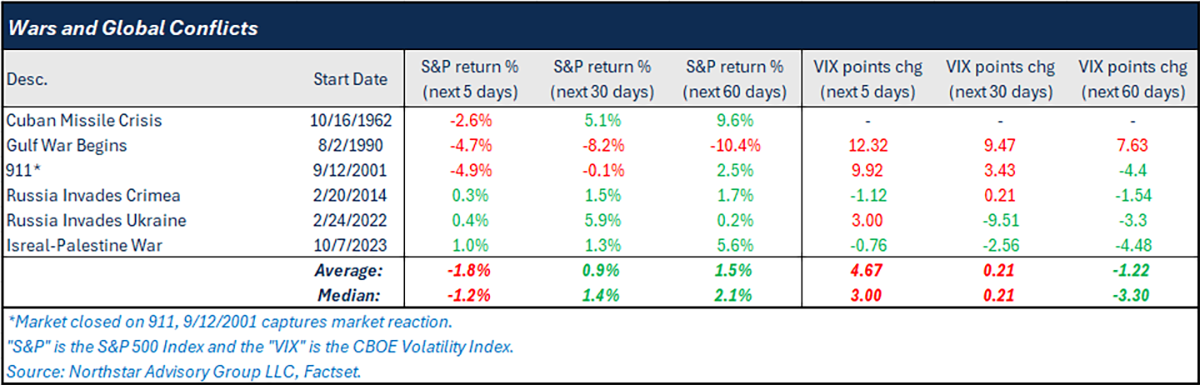

Lastly, let’s look at short-term market reactions from wars and global conflicts. On average, the stock market has been positive for the 30 and 60 days following these events. Although, they typically come with very short (5-day) periods of market pressure. This is likely because war can cause much larger systemic problems, such as energy crisis and supply chain disruptions.

Security threat

Freezing your credit is a crucial step in protecting yourself from the potential fallout of data breaches, both current and future. NSAG is recommending to all clients that they maintain a freeze on their credit at all times.

The number of data breaches and magnitude of data being exposed continues to climb. Here are some recent significant data breaches:

- National Public Data Breach: In August 2024, a massive breach exposed 2.9 billion records, including Social Security numbers, names, and addresses.

- MOVEit Transfer Breach: In June 2023, a vulnerability in the MOVEit Transfer software led to the exposure of data from numerous organizations, affecting millions of individuals.

- T-Mobile Breach: In January 2023, T-Mobile disclosed a breach that impacted 37 million customers, exposing names, addresses, and phone numbers.

- Twitter Breach: In December 2022, a breach exposed the data of 5.4 million users, including email addresses and phone numbers.

- Uber Breach: In September 2022, Uber suffered a breach that exposed sensitive data of both employees and customers.

These incidents highlight the importance of taking proactive measures, such as freezing your credit, to protect your personal information. Here are some key reasons why freezing your credit is important:

1. Prevent unauthorized access

When a data breach occurs, sensitive information such as social security numbers, birthdates and addresses can be exposed. This information can be used by identity thieves to open new credit accounts in your name.

2. Mitigate financial loss

A credit freeze can help you avoid significant financial loss. If a thief opens a credit card or takes out a loan in your name, you could be held responsible for the debt. This can lead to a lengthy and stressful process to clear your name and restore your credit.

3. Protect your credit score

Identity theft can severely damage your credit score, which can take years to rebuild. A poor credit score can affect your ability to get loans, mortgages, and even jobs.

4. Peace of mind

Knowing that your credit is frozen can provide peace of mind. With the increasing frequency and scale of data breaches, it’s reassuring to know that you have taken steps to protect your financial identity.

5. Free and easy to implement

Freezing your credit is free and relatively easy to do. You can place a freeze with each of the three major credit bureaus: TransUnion, Experian, and Equifax.

How to freeze your credit

To freeze your credit, contact each of the three major credit bureaus individually. They will ask for some personal information to verify your identity. Once the freeze is in place, you will receive a PIN or password that you can use to lift the freeze when necessary.

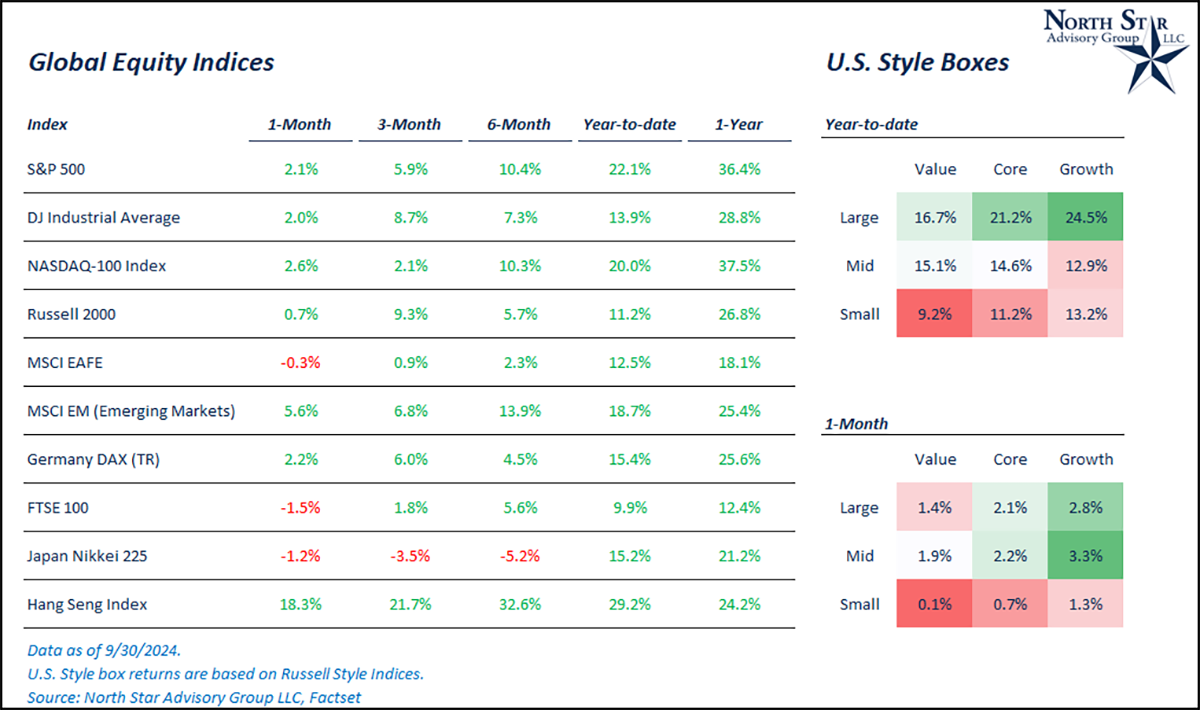

Where will the stock market go next?

In September, we saw the stock market perform well globally. Not only were all three major U.S. large cap indices positive on the month, but various international markets, particularly in Asia, received a sharp boost from Chinese stocks. The S&P 500 was +1.6% and the MSCI EM Index (emerging markets) was +5.6% for the month.

Focusing in on China, the PBOC (China’s central bank), unveiled a variety of new monetary and fiscal policy measures intended to stimulate their economy. The Shanghai Stock Exchange Composite Index rallied ~17% for the month in response to these policy shifts. President Xi Jinping, who has been attempting to be more “pro-business” since 2022, reiterated his backing of the PBOC’s new policies. Chinese citizens have a very high savings rate on average (+20%), and these stimulative policies are incentivizing increased consumption and investment within the country, as citizens are currently sitting on record levels of bank savings. This policy change could have a positive effect on other Asian-Pacific nations such as Japan and South Korea, as well as European companies who benefit from Chinese travel and luxury consumption. There are some who believe China’s economy has too many structural issues (aging population, low-birth rates, historically bad governance, etc.) and these policies may only provide a short-term boost in stock prices. While this is not a flawed view, it may not be wise to go against a government who is actively promoting investment in their capital markets.

Turning to the U.S., we are heading into a seasonally strong part of the year for the stock market. On average over the past 40 years, the S&P 500 has had positive returns in October, November, and December. Although, this seasonal trend is shifted during election years. When averaging the previous 10 election years, the S&P 500 is down 1.8% in October, +1.5% in November, and +1.4% in December.

We expect short-term government interest rates (1-month through 1-year maturities) to continue falling as the Federal Reserve eyes future rate cuts and we expect long-term interest rates (such as the 10 year) to remain flat or slightly higher, barring a recession.

With interest rate cuts expected to affect shorter-term lending rates, we expect future rate cuts to be a continued positive catalyst for small cap stocks as these companies rely heavier on short term variable lending, leading to a broader performing market.

Lastly, we expect the U.S. dollar to continue weakening. Year-to-date, the U.S. dollar index is only down ~1%, but down ~5.5% from its 2024 peak.

We are passionately devoted to our clients' families and portfolios. Contact us if you know somebody who would benefit from discovering the North Star difference, or if you just need a few minutes to talk. As a small business, our staff appreciates your continued trust and support.

Please continue to send in your questions and see if yours get featured in next month’s Timely Topics.

Best regards,

Mark Kangas, CFP®

CEO, Investment Advisor Representative