Each month we ask clients to spend a few minutes reading through our newsletter with the goal of raising their investor IQ. As the markets continue to be fixated on monthly inflation prints and potential next moves for central banks across the globe, we wanted to take a quick step back to assess the cumulative impact on consumers in recent years.

- Inflation-adjusted wages

- Shifts in spending

- Cracks in the economy

- Where does inflation go from here?

- NSAG News

- Where will the stock market go next?

Inflation-adjusted wages

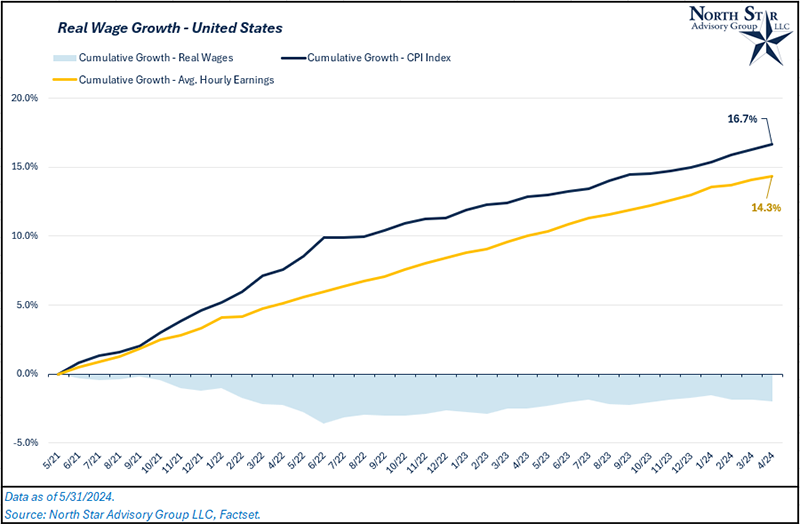

Over the past three years, consumer prices have risen by 16.7% cumulatively, or 5.3% on an annualized basis. Over this same time period, U.S. wages (measured by average hourly earnings of private employees) have risen by just 14.3%, or 4.6% on an annualized basis. So, on an inflation-adjusted basis, U.S. wages have decreased by ~2% from April 2021 to April 2024.

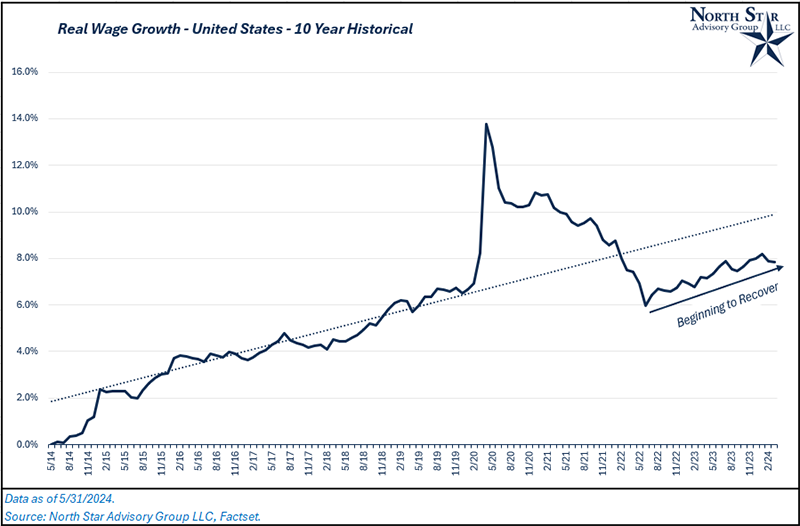

The bulk of the decline in real wages occurred from May 2021 to June 2022 when inflation was accelerating, and cumulative real wage growth bottomed out at negative 3.6%. Since June 2022, real wages have grown grown and began recovering their losses towards the 10-year historical trend.

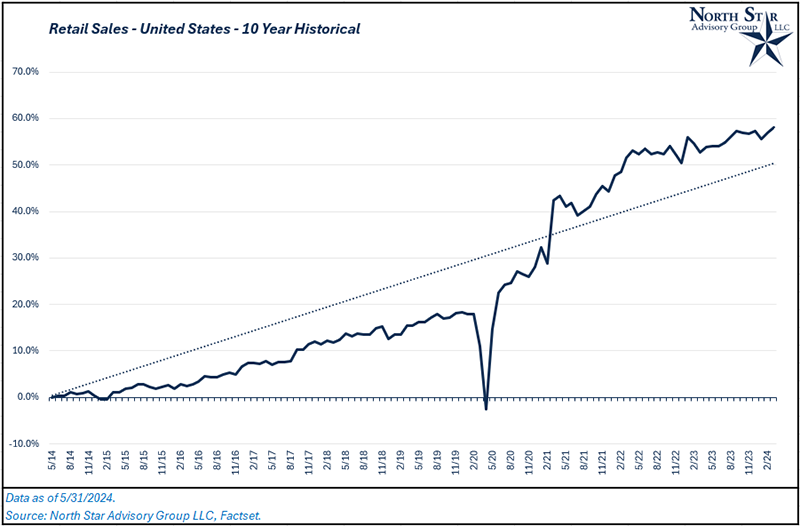

As inflation has eaten away consumer’s recent wage growth, how have they reacted and what are they doing to combat it? Consumer spending has continued to grow at a robust rate. Retail sales in the U.S. had jumped well above trend during Covid-times and continue to grow, powering through negative growth in real wages. This has displayed the sheer resilience of the consumer through the headwind of higher prices. Retail sales have grown by ~16% since May 2021 in the face of the decline in real wages.

Three main factors have allowed the consumer to be resilient: savings drawdown of COVID stimulus, increased credit card spending, and part time employment. Credit card debt has increased by ~43% since May 2021, although, this growth rate is coming off of a historically low number for credit card debt as consumers had used Covid stimulus to pay off a lot of their current balances in the year prior. There was $2.3 trillion in excess savings generated during Covid, which has been drawn down to ~$600 billion. Lastly, an increasing portion of the workforce, already employed full-time, has taken on an additional part-time job.

While the trends in these factors are not sustainable in the long run, it’s likely that the consumers will not need to lean on them as much moving forward. Historically, positive real wage growth has led to strong growth in the underlying economy. As we mentioned earlier in this section, real wages are recovering towards their long-term trend growth and if disinflation continues, this could be accelerated.

It’s important to note that not everyone in the U.S. has experienced these trends, particularly our client base. But, the markets and the Fed will continue to be focused on the data in aggregate for the entire economy.

Shifts in consumer spending

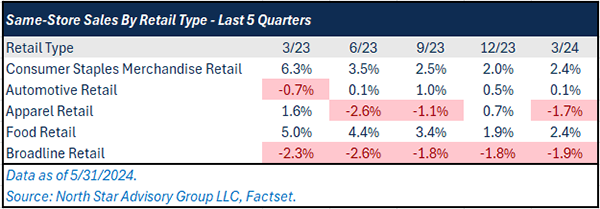

While the U.S. consumer has yet to take a beat in aggregate, we’ve seen some areas of pushback and spending shifts caused by inflationary pressures in certain areas of the economy. For example, we sampled multiple companies of various retailer types and compared same-store sales* growth over the last few quarters.

As budgets become tighter, we are seeing a pullback in discretionary areas such as broadline retail** and apparel retail, displayed by negative same-store sales growth in the table above.

Food and consumer staples growth remain positive as these are areas that are generally a need and not a want. Coincidently, food has experienced one of the highest inflation rates over the last three years while apparel has been the opposite. Food prices are up ~20% while apparel is up ~10%. It’s logical to see consumers pullback in discretionary spending areas in order to make up for price increases on necessity items.

*Same-store sales measures the growth in average sales per location. This is the preferred metric within the retail industry to assess consumer demand and organic growth.

**Broadline retail refers to companies that sell multiple items in their stores (Clothing, food, home products, etc.)

Cracks in the economy

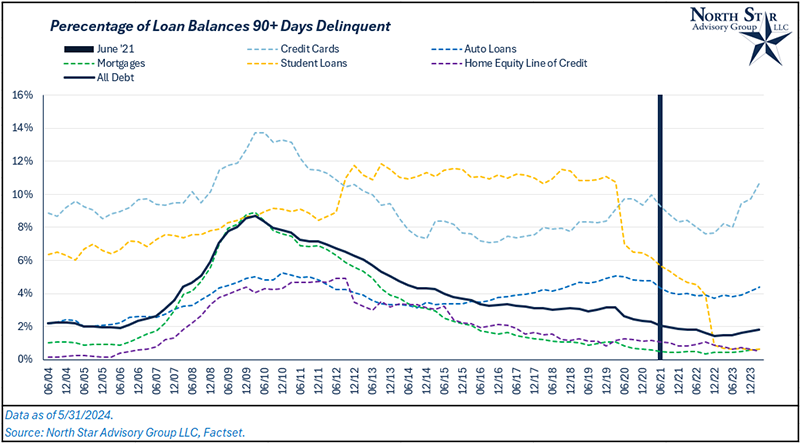

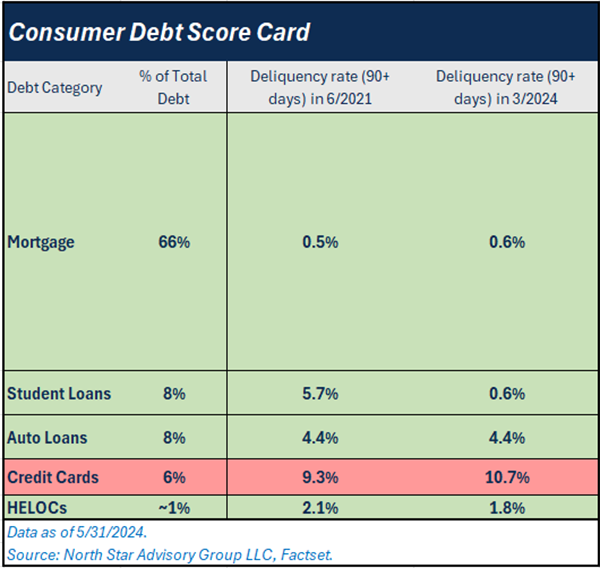

As real wages have fallen and consumers are feeling inflationary pressures evidenced by shifting demand, are we starting to see cracks forming in the economy? Let’s examine consumer debt and how manageable it has become. Primary categories of consumer debt include mortgage, auto loan, credit card, student loan, and home equity line of credit (HELOC).

Since June of 2021, we’ve only seen a material uptick in delinquencies for credit card debt, and even then, it has not risen to unmanageable levels outside of historic norms (Not to mention credit cards only account for ~6% of total consumer debt).

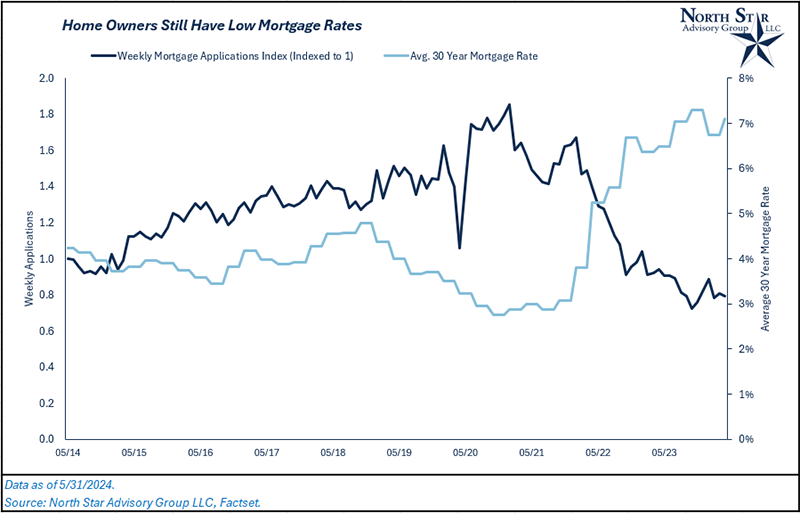

Mortgages delinquencies remain low as consumers have been unwilling to sell their homes in the face of higher mortgage rates. The majority of homeowners have mortgage rates locked in from ~3-5%, so they have not felt the same inflationary pressures that new homeowners post-2021 have felt. Mortgage debt makes up ~66% of total consumer debt, so this has been an additional tailwind for consumers as a large portion of their budgets have been fixed payments and not exposed to inflation. The chart below shows mortgage activity was growing at a high rate when 30-year rates were between 3-4%. Since rates have more than doubled, activity has collapsed. The majority of outstanding mortgage debt has a low rate attached.

One of the larger potential stress points moving forward would be student debt payments coming back online for the masses. As of March 2024, delinquencies are just under 1%. Student loans make up ~8% of total consumer debt.

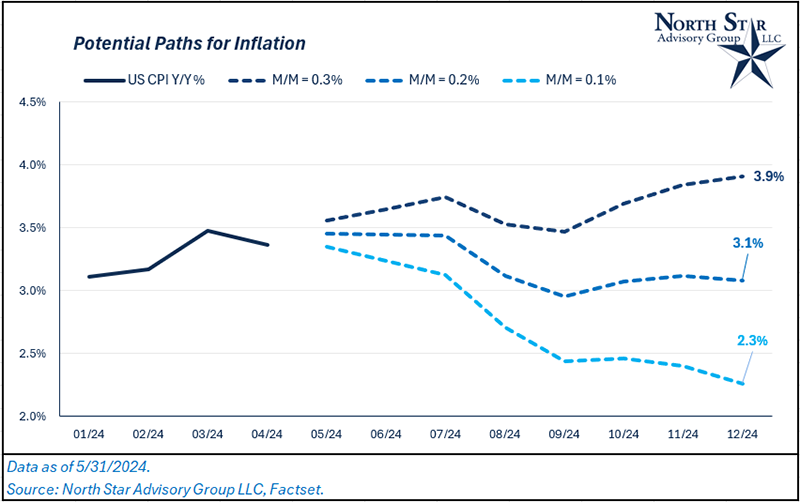

Where does inflation go from here?

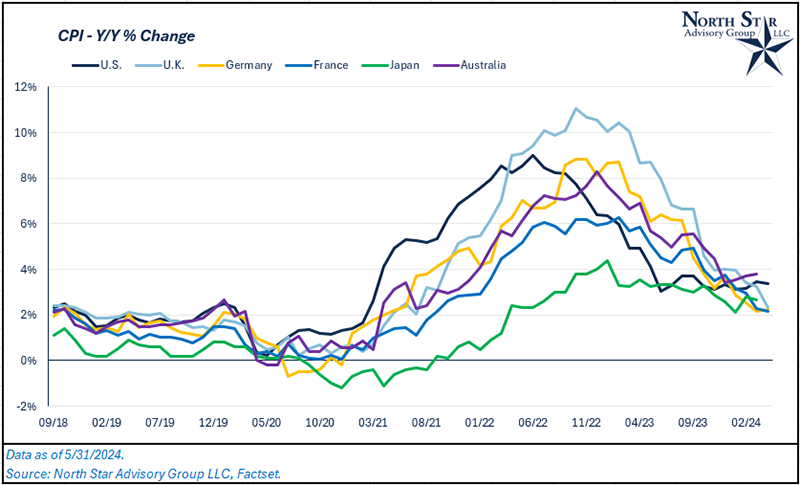

The U.S. is still on a disinflationary path and it’s following a similar trend as the rest of the developed world. Over the past year, inflation in the U.S. has been relatively flat averaging around 3.5%, prompting the Federal Reserve to hold off on interest rate cuts while the rest of the world’s central banks talk more dovish (more in favor of supportive monetary policy).

The Federal Reserve has a target inflation rate of 2% and they have been consistently communicating that rate policy will likely be unchanged until the path to 2% is clear. What would it take to return the U.S. to 2% inflation by year end? Consistent month-over-month (M/M) inflation changes of 0.10% would bring CPI back down to 2.3% from 3.4%, measured in April. We’ve been running at an average M/M change in CPI ~0.35% so far in 2024.

Given that we’ve seen producer prices (PPI) continually fall and commodity markets stabilize, the door is open for disinflation to continue along with the rest of the world. We’ve seen a significant drop in commodity volatility since 2022. Even as a second war broke out last year in the middle east, oil prices saw relatively no material impact. Producer prices (PPI) bottomed out last year with a Y/Y change of 0.8% and have since picked back up. Although, PPI remains at lower levels (2.2% Y/Y in April). We’ve heard commentary from many consumer companies that they have no more room left to push prices through to consumers and we’ve actually seen price cuts in some discretionary areas such as autos. Although, there are continual near-term pressures that could re-accelerate inflation. For example, the global economy is hitting another shipping container shortage and ocean freight rates are spiking. This could spark a transitory increase in inflation as there is concern that freight rates could surpass peak rates during the Red Sea dispute. A short term reignition of CPI would force the Fed to push any rate cut possibilities even further down the road, with the market reacting negatively.

NSAG News

A tiny bundle of joy has arrived!

Lisa and Sal are over the moon,

As they welcome a baby boy, a precious boon.

Santo Niño Saia, a name so sweet,

Born on May 27th, a miracle to greet.

At 8 pounds and 1 ounce, he's just right,

20.75 inches long, to their delight.

A new adventure for this family starts,

With tiny hands and a big heart.

So, let's celebrate this joyous news,

With baby giggles and little coos.

Welcome, Santo Niño, to love's endless dance,

Your journey begins with just one glance.

Santo Niño Saia

Born: Monday, May 27th, 2024

Weight: 8 lbs 1 oz

Length: 20.75 inches

Proud Parents: Lisa & Sal

Where will the stock market go next?

In our view, the stock market will continue to be hyper-focused on where investors believe the Federal Reserve’s rate policy will go. We see these reactions daily. When economic data comes in hotter than expected, investor’s expectations for rate cuts decrease and the market sells off (and vice versa). Although, the Fed continues to walk the tight rope between slowing growth in the economy without collapsing the economy.

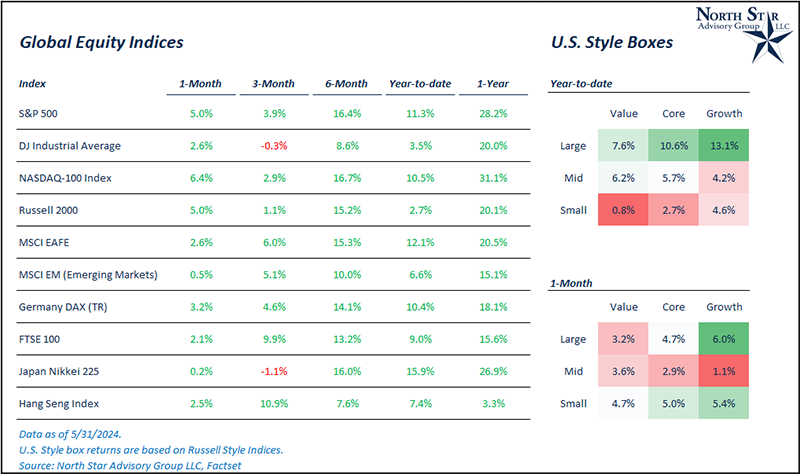

Broadly, stocks recovered their April losses in May. The S&P 500 was up 5%, the Russell 2000 (Small Cap) was up 5%, MSCI EAFE Index (International Developed) was up 2.6%, and MSCI EM (Emerging Markets) was up 0.5%. International stocks continue to outpace the U.S. in 2024, led by Germany, Japan, and Italy. Additionally, Hong Kong is beginning a new bull market with the Hang Seng Index up 11% over the past 3 months and 20% higher off the index lows. Cheap valuations, expectations of supportive monetary policy, and influx of Chinese investors has led the index higher.

We are seeing new bull markets begin to form in various developed international markets (Germany, Japan, and Italy noted above) as these economies are recovering from their earnings troughs of 2022 and 2023.

We are passionately devoted to our clients' families and portfolios. Contact us if you know somebody who would benefit from discovering the North Star difference, or if you just need a few minutes to talk. As a small business, our staff appreciates your continued trust and support.

Please continue to send in your questions and see if yours get featured in next month’s Timely Topics.

Best regards,

Mark Kangas, CFP®

CEO, Investment Advisor Representative