Each month we ask clients to spend a few minutes reading through our newsletter with the goal of raising their investor IQ. February’s Timely Topics commentary covers a few potential sources for market volatility in 2024 and reinforces the power of continuing to invest through volatility.

- Red Sea trade disruptions

- Investing through an election year

- Lump sum vs. dollar cost averaging

- Taxes & tax forms

- Healthy eating & a healthy budget

- Where will the stock market go next?

Markets back to an all-time high?

Many factors have contributed to higher-than-average inflation rates across the globe over the past two years. While the primary catalyst for higher inflation has always been the increase in global money supply experienced during the COVID-19 pandemic, there have been many exogenous shocks since 2021 that have caused inflation to remain elevated. These include the Russia-Ukraine War, Covid-variant related lockdowns in the Asia Pacific (APAC) Region and China in 2021 and 2022, the Suez Canal blockage by a container ship in 2021 for 6 days and the Israel-Palestine conflict, to name a few. Now we have a new one stemming from the Israel-Palestine conflict, and it brings another potential shock in the Red Sea.

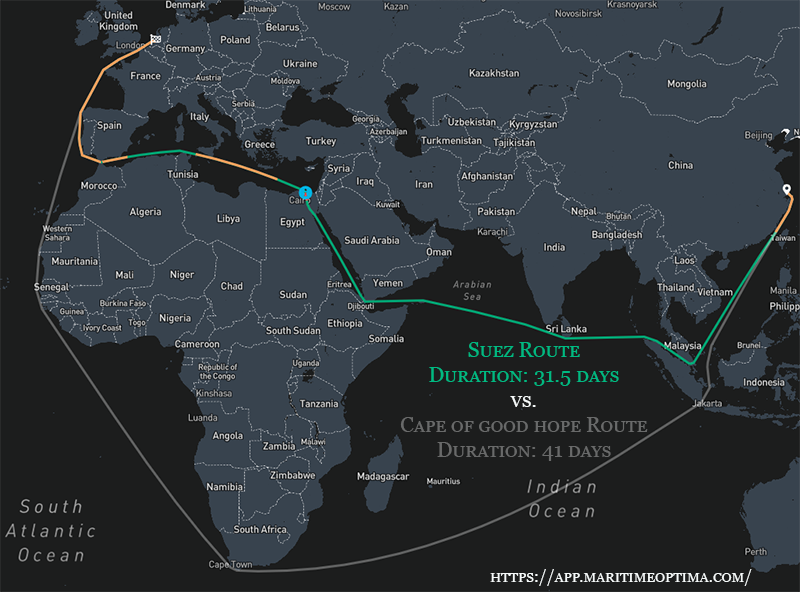

The Iran-backed Houthi Military Group has begun attacking container ships entering the Red Sea off the coast of Yemen. The Red Sea is an extremely important body of water for international trade, as it leads to the Suez Canal. The Suez Canal connects the Red Sea and the Mediterranean Sea, which indirectly connects the Indian Ocean to the Atlantic Ocean. This is the most important canal for European trade with APAC and the Middle East, with 12% of all global trade and 30% of global container traffic passing through it. While not the most important canal for U.S.-APAC trade, it certainly still carries its weight, with about 30% of U.S. East Coast trade traveling through the canal.

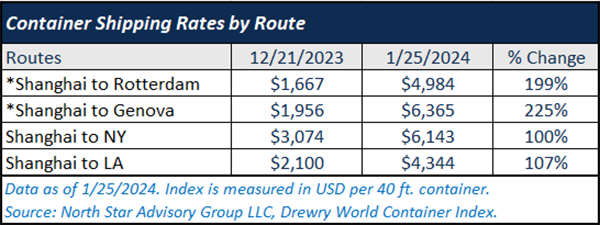

Due to the Israeli-Palestinian conflict and subsequent attacks in the Red Sea, container ships have opted to route themselves around the Cape of Good Hope (Cape Town, South Africa). Shanghai to Rotterdam (Netherlands) via the Cape of Good Hope route is 10-11 days longer than through the Suez Canal (~33% increase in trip time). This has spurred a spike in container shipping costs globally.

https://app.maritimeoptima.com/

*Heavily used sea-based shipping routes in APAC-Europe trade and most affected by the Red Sea dispute.

Additionally, as a result of this conflict, we are seeing side-effects such as:

- Increased air-freight rates

- Increased demand for U.S. and Brazilian energy as Europe turns to Atlantic basin nations.

Due to this exogenous shock, we should expect a transitory increase in consumer prices should the increased shipping rates be passed through to final products/consumers. This impact is likely be short-lived depending on the speed at which disputes in the Red Sea are calmed. The U.S. and U.K. have increased their military presence in the Red Sea to fend off Houthi attacks.

What does this mean for client portfolios? The increased pricing of some shipping may lead to an increase in inflation in the coming months. Increased inflation could put upward pressure on interest rates and subsequent downward pressure on long duration assets (stocks and bonds). It is important to remember the consumer price index is based on lagged data, so we likely won’t see this impact in the numbers immediately.

Investing through an election year

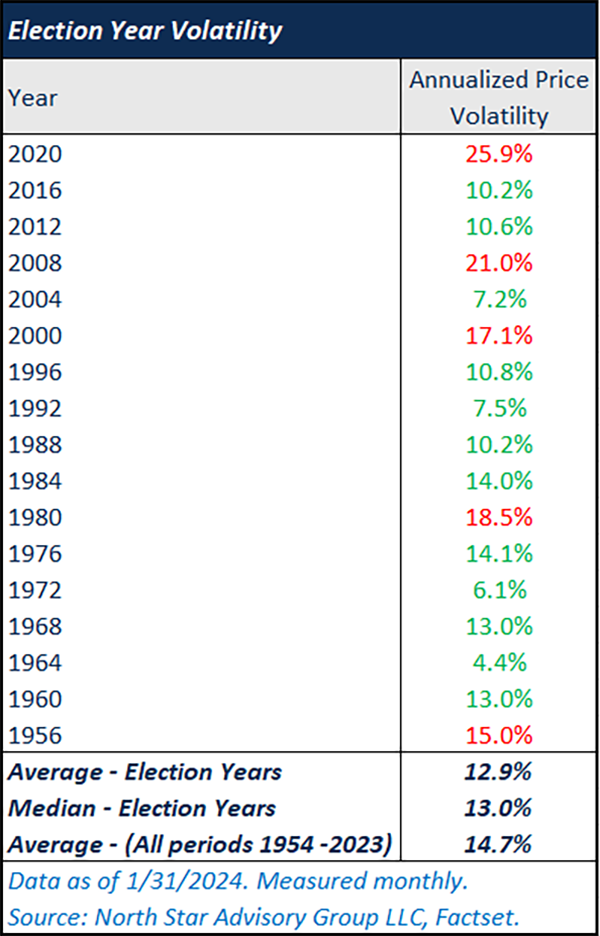

The GOP primary is under way in preparation for the upcoming U.S. presidential election in November 2024. Most investors are expecting higher levels of volatility in the markets driven by political tensions and constant presidential news cycles. In actuality, historical price volatility for the S&P 500 Index shows that equity prices tend to have less volatility in election years relative to all periods over the past 70 years, on average.

In the table below, we’ve shown the S&P 500’s annualized price volatility over the past 17 election years. Only five of the past 17 election years had higher volatility than the average since 1954. Four of these five years (1980, 2000, 2008, and 2020) had either a recession or significant market turmoil (for example, there was no recession in 2000 but we experienced the “Dot.com bubble”) leading to higher volatility.

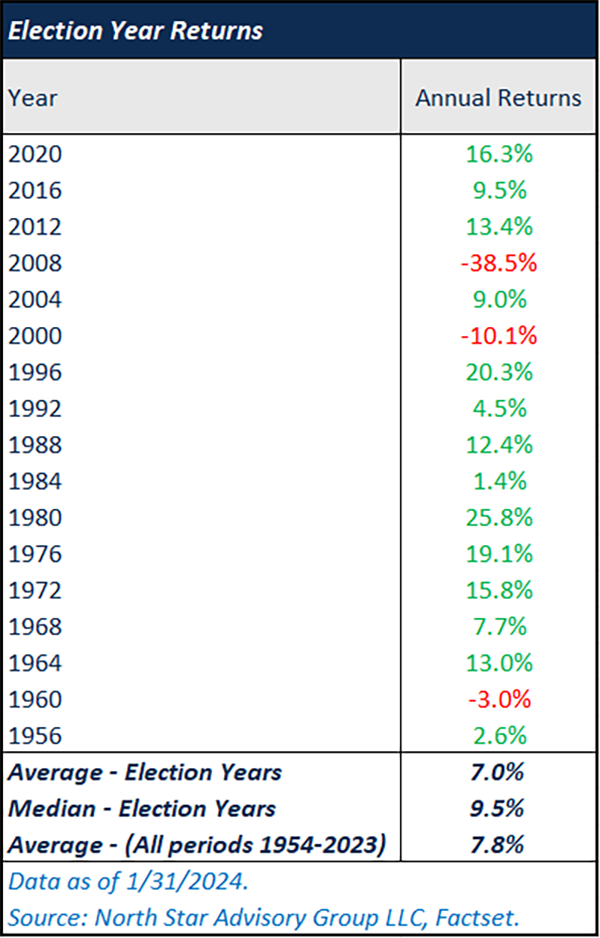

The S&P 500 had negative price returns in only 3 of the past 17 election years, with an average annual price return of 7%. Although this is below the average annual return of all years since 1954, the average return for the prior 14 election years with positive returns is 12.2%, around 4% higher than the all-period average.

Important Note: We are using price returns and volatility instead of total returns (price change + dividends) given that Factset’s total return data set does not extend back 70 years.

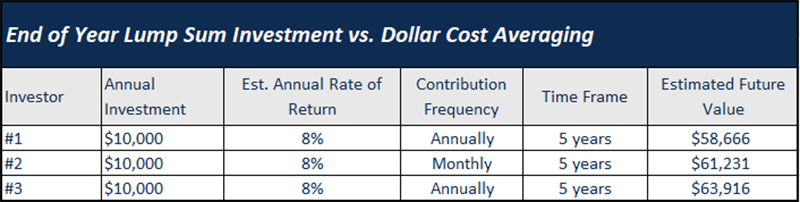

Lump sum or dollar cost average

Clients have asked us about various deployment methods for investing into the equity markets. Clients have asked whether investing smaller dollar amounts each month via dollar cost averaging (DCA) is better than investing a lump sum amount at the end of the year. To illustrate the differences between each method and what it means for the future value of your portfolio over time, we constructed a simple hypothetical time-value of money comparison. For this hypothetical, investor #1 is going to invest $10,000 at the end of each year over the next 5 years, earning an average annual return of 8%. Investor #2 will also invest $10,000 per year, but they will reach their annual goal of $10,000 by investing small amounts ($833) at the end of each month, earning an average annual return of 8%. Lastly, Investor #3 is going to invest $10,000 at the beginning of each year over the next 5 years, earning an average annual return of 8%.

Investor #2 will have been better off over the 5-year period by ~$2,500 relative to investor #1. The difference here is driven by the fact that investor #2 receives the benefit of monthly compounding. If the annual average return for these investors is 8%, the average monthly return is 0.67% (8%/12 months). When you compound the monthly return of 0.67% over 12 months, the actual annualized return for investor #2 is ~8.3% (not 8% flat). Investor #3 gets the benefit of both monthly compounding and having their full $10,000 investment receiving this compounding 100% of the time each year. Over the 5-year period, investor #3 is better off by ~$2,600 relative to investor #2.

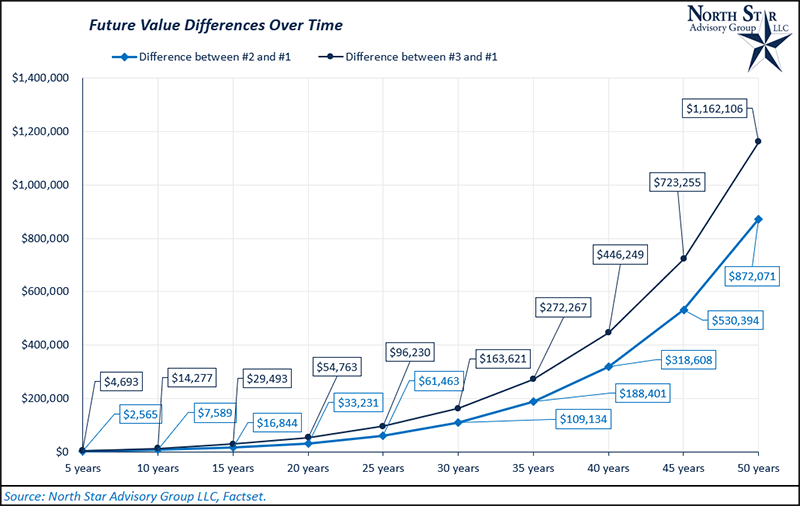

The benefit of time invested, and monthly compounding will also compound on itself over longer time horizons. If we extend the time frame from 5 years to 50 years, you’ll notice that each investor’s future values grow exponentially, but the relative difference between each also grows exponentially. At the end of 50 years, investor #2 has ~$872,000 more dollars than investor #1 and investor #3 has ~$1.2M more than investor #1. Increasing time in the market reaps the benefits of having more dollars exposed to the market risk premium for longer.

Taxes & tax forms

As we enter the early innings of 2024, clients are eager to set up meetings with their tax advisors and CPAs to prepare for the April 15 tax filing deadline. As these meetings are being scheduled, we want to remind clients to have realistic expectations for receipt of certain tax forms.

- W2s are supposed to be mailed by January 31.

- K1s for partnerships are supposed to be mailed by March 15, but can occasionally be mailed even later.

- 1099R for retirement account distributions are normally mailed by February 15.

- 1099 for realized capital gains, interest income, and dividend income amounts in brokerage accounts are normally mailed between February 15 and March 15. It is also not uncommon to have a corrected 1099 to reclassify the taxation of dividends. This corrected 1099 generally, but not always, will slightly reduce a taxpayers amount due. We also have custodians occasionally hold back mailing their 1099s if they are expecting a correction to it.

- For clients who transitioned between two firms in 2023 (for example, from TD Ameritrade to Schwab), we want to remind you that you may be receiving two form 1099s for your accounts.

- One from the first custodian (TD Ameritrade) for beginning of the year reportable activity

- One from the second custodian (Schwab) for end of the year reportable activity

- Delivery of forms will follow your paperless preferences. If you are enrolled for paperless delivery, you will receive an email notification when your tax forms are available for download, or you will receive tax forms via mail if you have selected to receive paper statements.

For more information on updated IRS guidelines for 2024, check out NSAG’s Tax Guide HERE.

Keep these dates in mind before scheduling your meetings with your CPAs. Please call us if you have any questions about your tax forms.

Healthy eating & a healthy budget

As mentioned last month, eating out is a fast way to drive your monthly expenses up. Here’s a recipe idea for a quick, nutritious, delicious breakfast to start your day off on the right foot while keeping costs down.

A day at the beach smoothie (Serves 2) Ingredients 1 frozen banana 1/3 cup frozen mango 1/3 cup frozen pineapple 1 inch peeled fresh ginger, or 1 tsp ground ginger ¼ tsp turmeric 1-2 scoops of your favorite protein powder (vanilla goes best with this recipe) 2 Tbsp hemp seed hearts 1 ½ cups unsweetened almond milk (or milk of your choice), add more to thin out, or less if you like a thicker consistency

Put all ingredients in a high-speed blender and blend to your desired consistency. You may need to scrape the sides down, add more milk or less, depending on your desired serving style. Divide smoothie between two glasses and feel like you’re back on the beach during these dreary winter months. With a thicker consistency, you may opt to serve this in a bowl sprinkled with some granola, fresh fruit, or sliced almonds. Enjoy!

A note about smoothies: Possibilities for flavor combinations are endless! You can easily substitute ingredients in this recipe with what you have in your freezer and pantry. Grocery stores also sell frozen fruit pre-mixed to take the guess work out of your recipes. Stick with frozen fruit as fresh fruit can make the smoothie too watered down.

A note on savings: Frozen banana’s are the base ingredient for this recipe. Several grocery stores sell bundles of bananas that have slightly browned for $1-2 for the bunch. These bananas are the ideal consistency and favor palate for smoothies. Simply buy the bunch and break each banana into 4 pieces on wax paper on a cookie sheet and then put the cookie sheet in the freezer overnight. The next morning, transfer them into a zip lock bag or plastic container for storage in the freezer for future use.

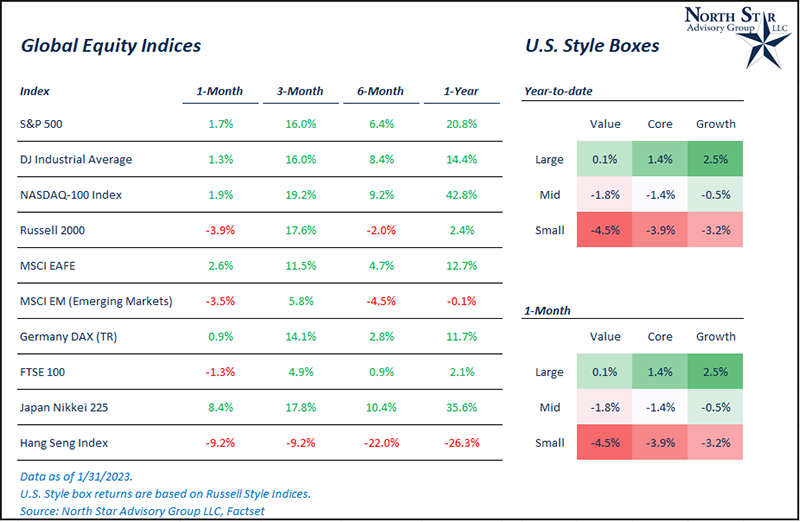

Where will the equity markets go next?

In January, equity markets continued to extend their gains following strong performance in Q4 of 2023. The leaders of the market in January have been U.S. large cap (S&P 500), which is up 1.7% through 1/31/2024. U.S. small cap stocks (Russell 2000) have notably lagged in January, down 3.9% through 1/31/2024. This downward move in small caps will likely be short lived as it followed a +21% move over the last two months of 2023, while U.S. large cap was only up 12% during that same time period. There’s been some short-term rotation following the small cap’s strong relative outperformance.

We’ve continued to have positive surprises for key economic data points in January. To name a few:

- Q4 2023 Y/Y GDP growth was higher than expected in its first preliminary reading (3.3% vs. 1.8%).

- Housing starts for December were higher than expected (1.46M vs. 1.42M)

- Michigan Sentiment preliminary reading for January was higher than expected (78.8 vs. 69.5)

- Retail Sales M/M for December was higher than expected (0.60% vs. 0.40%)

We are passionately devoted to our clients' families and portfolios. Contact us if you know somebody who would benefit from discovering the North Star difference, or if you just need a few minutes to talk. As a small business, our staff appreciates your continued trust and support.

Please continue to send in your questions and see if yours get featured in next month’s Timely Topics.

Best regards,

Mark Kangas, CFP®

CEO, Investment Advisor Representative