Each month we ask clients to spend a few minutes reading through our newsletter with the goal of raising their investor IQ. September’s Timely Topics commentary focuses on the recent rating downgrade of U.S. government debt and recent changes to student loans.

- U.S. debt downgrade

- The threat of China

- Chinese real estate crisis & consumer rebound

- Student loan forgiveness & repayment

- NSAG news

- Where will the equity markets go next?

U.S. Debt Downgrade

On 8/01/2023, Fitch (one of the three major rating agencies) downgraded the U.S. debt rating from AAA to AA+. For reference, AAA is the highest possible rating for any debt instrument and AA+ is one notch below.

Fitch cited the following reasons for their decision to make the downgrade:

- Erosion in governance due to consistent political standoffs relating to the U.S. debt ceiling.

- Expected increase in the government deficit from 3.7% of GDP in 2022 to 6.3% in 2023 accompanied by weaker government revenues and increased spending.

- Fitch forecasts a Debt/GDP ratio of ~118% in 2025, compared to the current level of ~113%. The median Debt/GDP ratio for other AAA rated countries is 39.3%. Higher debt levels leave the U.S. more vulnerable during future economic shocks/financial crisis.

- Lastly, higher interest rate levels have significantly increased the U.S.’s interest expense.

There are many contrarian arguments that could be made that counter the downgrade’s rationale, including global reliance on the U.S. economy and the U.S.’s military strength. These two key realities continue to provide stability for the U.S. economically. In terms of global competition, China has been the U.S.’s closest competitor over the past decade. As China’s economy begins to crack, the U.S. could gain additional stability (we will discuss this further in the next section).

Overall, both sides of the argument make valid points. With that being said, the downgrade happened. So, what does this mean for the markets?

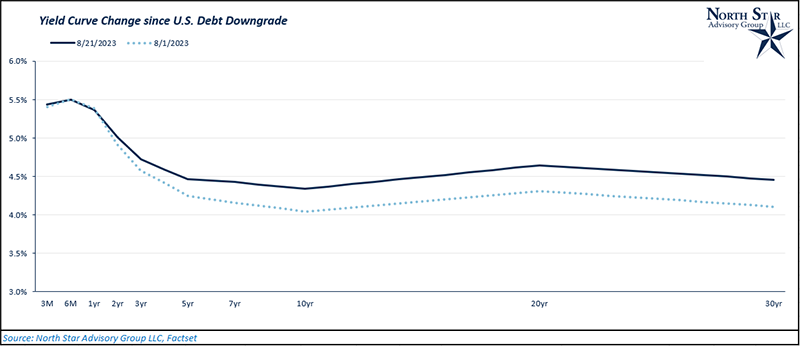

Since 8/01/2023, equity markets are generally lower. As of 8/30/23, the Dow Jones Industrial Average, S&P 500, and the NASDAQ indices are down 2.1%, 1.4%, and 1.5%, respectively. Generally, bond prices are also lower as government bond rates have risen and the yield curve has undergone a “bear steepening.” A bear steepening occurs when long-term rates have risen more than short-term rates (see chart below). Bear steepening tends to put downward pressure on equity prices. The U.S. 10-year Treasury yield increased from 4.05% to a peak 2023 yield of 4.35% on 8/21/2023.

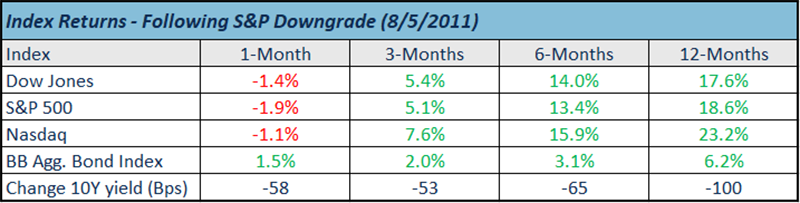

The last time U.S. debt was downgraded by a major rating agency came almost exactly 12 years ago on 8/5/2011 when Standard and Poors (S&P) lowered their rating down one notch from AAA to AA+ as well. In the following month, the three major equity indices posted modest declines but were all higher over the subsequent 3-, 6-, and 12-month time periods (See table below).

The threat of China

China has been the U.S.’s top economic competitor for more than 10 years. Over the past 30 years, China has grown its real GDP at an average annual year-over-year rate of 8.9%, while the U.S. has grown at an average annual rate of 2.5%. Although this number may seem alarming, the two countries were vastly different 30 years ago in 1993. China was much less developed and a true emerging market country while the U.S. was developed and considered the strongest nation in the world. China had much more growth potential from labor, capital, and technological advancements. The U.S. (like any well-developed country) has relied heavily on technological advancement for economic growth.

As of 2022, China had an annual nominal GDP of $17.9 Trillion, while the U.S. remained the world’s largest economy with a nominal GDP of $25.4 trillion. China’s growth rate created the appearance that they were a threat to overtake the U.S. as the world’s largest economy. However, this threat appears to be softening as economic growth in China slowed in 2022 to 3.3% year-over-year. It is possible that China’s continued investment in infrastructure has become overheated and they will begin experiencing diminishing rates of return from their capital investment. This can be evidenced by the potential real estate crisis happening in China as vacancy rates have been increasing in major cities (Grade-A office vacancy rate is around 20% according to South China Morning Post), and global companies begin diversifying their supply chains closer to home and away from China. Additionally, China has one of the lower population growth projections globally. More than 40% of China’s population is 50 years or older compared to 34% for the U.S. Lower birth rates, lower manufacturing for overseas and less stimulus through infrastructure spending could mean that China has to heavily rely on technological advancement for economic growth just like any other developed country. These recent developments could put the CCP’s 5% annual economic growth target at risk moving forward.

Chinese real estate crisis & consumer rebound

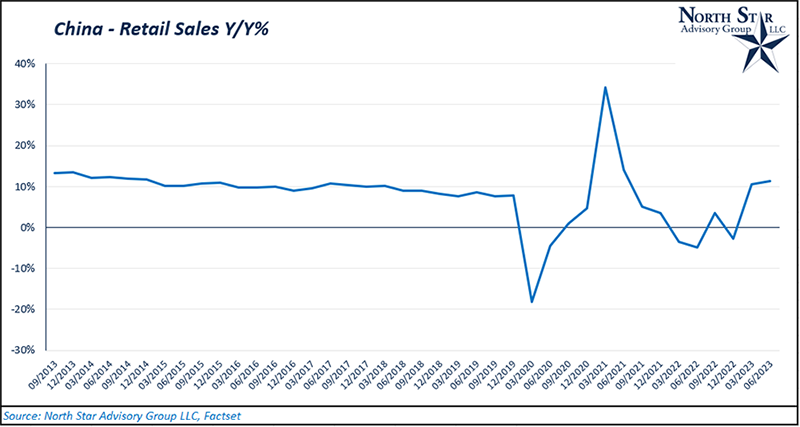

While retail sales in China are now exceeding pre-Covid levels from 2019, the ongoing potential of a real estate crisis in China could reduce future sales. The impact that this could have on the Chinese consumer could have major implications for economic growth in China and other countries globally. Slowing population growth, impacts from covid, and “Zero-COVID” policies, combined with over-investment in the real estate sector have led to increasing vacancy rates in major Chinese cities. These developments have put various real estate developers, such as Country Garden and Evergrande under significant financial stress. Evergrande filed for bankruptcy on 8/17/2023. The real estate sector has been a major driver in economic growth for China historically and consumer wealth in the country is largely tied to real estate.

Historically, the Chinese consumer has had a strong impact on economic growth globally from their discretionary spending on goods and services such as travel, restaurants, American technology, and European luxury items, etc.

On 8/21/2023, China’s central bank cut its one-year policy rate and took various steps to stabilize its currency value as the yen had been depreciating through 2023 amid the countries weak economic outlook. If the economy in China continues deteriorating, we’d expect the CCP and People Bank of China (PBOC) to continue implementing stimulative policies to stabilize their economy and currency. As we have previously discussed, foreign currency stabilization (yen) could lead to a slightly weaker U.S. dollar and potentially boost returns for international investments.

Student loan forgiveness & repayment

For the first time since March 13, 2020, many borrowers are preparing to restart student loan payments after the COVID-19 payment pause. The first payment is due in October 2023. Borrowers will get a bill, with the payment amount and due date, at least 21 days before the due date. Borrowers who are eligible for the new SAVE program will have any outstanding balance on their loan forgiven if they haven't repaid their loan in full after 20 years (if all loans were taken out for undergraduate study) or 25 years (if any loans were taken out for graduate or professional study).

Click HERE for easy-to-follow actions borrowers should consider before payment resumes in October. Important steps include, but are not limited to:

- Setting up auto payments to save 0.25%.

- Evaluate income-driven repayment plans, including the new SAVE program.

Saving on a Valuable Education (SAVE) program The Biden administration announced the SAVE program earlier this summer, following the Supreme Court's decision to overturn their proposed loan cancellation program.

The SAVE program does not deliver debt forgiveness immediately as the administration initially sought to do. But millions of borrowers, including those with higher incomes may see some of their debt forgiven under this plan.

The program will calculate monthly payments based on the borrower's income and family size. Borrowers will need to pay between 5% and 10% of discretionary income, weighted by the percent of your loans from grad school (all undergrad pays 5% while all grad pays 10%). Payments are recalculated each year and are based on your updated income and family size. The administration estimates that under SAVE more than a million borrowers will qualify for $0 monthly payments, while the average borrower will save about $1,000 a year. Under the SAVE plan, as long as borrowers make their monthly payments, interest will not accumulate.

Borrowers with federally held loans including direct subsidized, unsubsidized and consolidated loans, qualify for SAVE. Parents who took out a federal loan to help their children pay for college (known as Parent PLUS loans) are not eligible for SAVE.

The new SAVE program does provide for forgiveness based on the newly eligible months from the one-time account adjustment, borrowers who have reached 240 or 300 months (as applicable) worth of payments for Income Driven Repayment (IDR) forgiveness or 120 months of Public Service Loan Forgiveness (PSLF) started to see their loans forgiven in the spring 2023. The Department will continue to discharge loans as borrowers reach the months needed for forgiveness, based on their loan types.

In addition, under New REPAYE, you can file taxes separately and exclude your spouse's income from the payment, which means many borrowers should consider filing as “married filing separately” for tax year 2023. This filing may impact any Roth IRA contributions made for 2023.

Borrowers can now apply at www.studentaid.gov/SAVE. The application process is estimated to take 10 minutes.

NSAG news (new login)

For clients transitioning to Charles Schwab & Co., Inc. or any of its affiliates (“Schwab”), you will have choices when it comes to the accessing and trading platforms you use at Schwab. Once accounts move to Schwab, clients will have access to Schwab.com and the Schwab Mobile app, plus the entire thinkorswim suite of platforms (desktop, web, and mobile).

We know that any platform change can be an adjustment. More information is available on what to expect from Schwab's platforms, get an overview of key differences, and see what's coming.

Labor Day weekend, clients will be in a “black out period” where they will not be able to access their accounts while they migrate to Schwab.

September 5 is the target date for clients to switch the way they directly access their accounts with their new custodian Schwab.

- Please be aware that alerts established the old custodian’s website or mobile app will not move with your account to Schwab. You'll need to establish new alerts after the account move.

- If you did not setup your new UserID through the old custodian’s website, you can use Schwab’s web portal and click on “New User?” in the bottom right-hand corner. You will need your account number, date of birth, social security number and phone number to complete the new user registration.

- Do not hesitate to give us a call. NSAG is happy to assist you in setting up your new access and providing your new account numbers.

- You can access your accounts via Schwab’s web portal, mobile app or ThinkorSwim:

- Your prior custodian’s UserID will not work for the new Schwab portal.

Schwab's mobile app (link to download).

- You can delete the prior custodian’s app from your mobile device.

- Use your finger, face ID or preset passcode to quickly check your portfolio balance (including non-Schwab accounts), holdings and statements.

- Deposit checks directly into your Schwab Brokerage and IRA accounts by snapping a few photos.

ThinkorSwim While the ThinkorSwim trading and research platform will migrate to Schwab, your prior custodian’s UserID will not work for the new Schwab ThinkorSwim portals. You will need to use your new Schwab login credentials noted above. You can continue to access ThinkorSwim in the following three ways:

- The desktop version will remain the same, no new download will be needed.

- Access the website, plus an easy-access link on Schwab.com.

- For mobile access, there's nothing to download or install. Enjoy a smooth and seamless mobile experience on your current app.

NSAG’s client portal will remain unchanged and accessible. NSAG is working with our technology partner (BlackDiamond) to seamlessly link prior any prior account balances, activity and history to new corresponding Schwab accounts. Prior to the linking, clients will see the prior custodian’s balances and activity stop and the new Schwab accounts start. After the linking is completed, the accounts will appear as one smooth account. No action is needed by clients. We will automatically be working on this in the background.

Where will the equity markets go next?

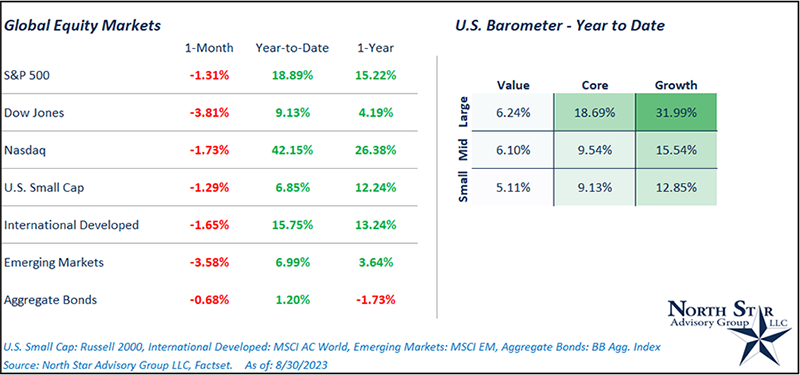

In recent weeks, the market has slashed prices for companies who miss their earnings, have low positive cash flow and/or have significantly higher debt to their peers. NSAG views this type of price action as positive for the health of equity markets as we are seeing a flushing out of investing in financially unhealthy companies. Furthermore, we previously discussed this month’s U.S. debt rating downgrade, which has pushed up the yield on the 10-year U.S. Treasury. In the following chart, we break down performance for various indices, which include the impact of a higher U.S. 10-year yield. This impact has put additional negative pressure on equity prices in August.

Looking a little bit deeper, the above chart sheds light on two important areas of investing.

- The perception of risk-free does not always equal good returns. Rising interest rates have sparked a renewed interest in bonds from investors. The thought process for many has been, “why not buy a bond fund when you can get 5%+ in interest without taking risk in equities?” Meanwhile, bonds have are down for August, essentially flat year-to-date, negative for the 1-year and had significant losses in 2022.

- The Nasdaq was down big in 2022. With the help of the mega cap names and the Artificial Intelligence (AI) boom, the Nasdaq has rebounded significantly in 2023. Those who abandoned growth after 2022 likely missed out on one of the best performers in 2023. While NSAG continues to hold investments in large cap growth, NSAG continues to warn clients about over concentration and/or chasing returns in technology as the forward-looking returns are likely not as favorable for parts of the Nasdaq relative to other investments in the global markets.

As we finish writing this commentary, there is one trading day left in August. It’s impressive to see that heading into the final week of trading, the S&P 500 went all month without back-to-back positive days. Now, the S&P has strung together its fourth straight positive day. That’s the good news. The bad news is that we’re heading into one of the toughest parts of the calendar. Over the last ten years, September has been the weakest part of the late summer/early fall consolidation period for the S&P 500.

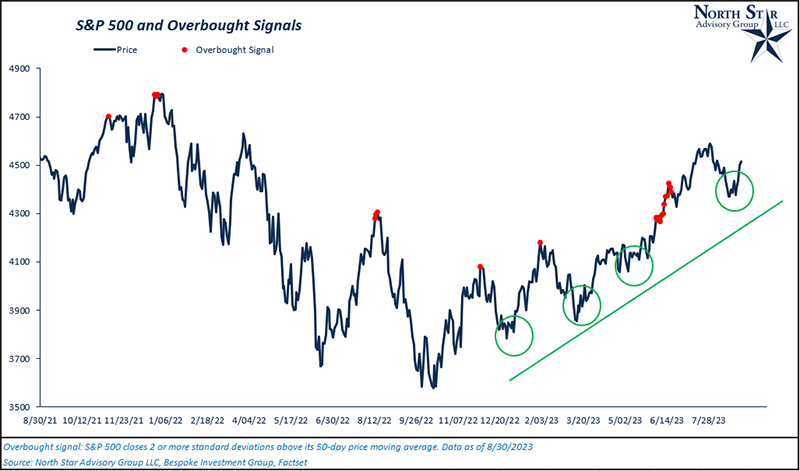

Even with August’s pullback, the S&P 500 is still in an upward bull market from October 2022’s lows. Below we updated the chart we provided in July 2022’s Timely Topics to help provide a high-level view of recent price volatility. While the first 10 months of 2022 tested the resolve of many investors, we still believe we are in a secular bull market, which started in 2010 and typically lasts around 15-20 years. However, this secular market is likely to last longer due to a slow start in 2010-2013. It is not uncommon to have bear market pullbacks inside of longer secular bull markets. We saw a bear market in 2020 due to COVID and the markets entered and exited bear market territory three times in 2022 (May, June & October).

We are passionately devoted to our clients' families and portfolios. Contact us if you know somebody who would benefit from discovering the North Star difference, or if you just need a few minutes to talk. As a small business, our staff appreciates your continued trust and support.

Please continue to send in your questions and see if yours get featured in next month’s Timely Topics.

Best regards,

Mark Kangas, CFP®

CEO, Investment Advisor Representative