Each month we ask clients to spend a few minutes reading through our newsletter with the goal of raising their investor IQ. If rising interest rates are giving you the blues, perhaps the decreasing probability of a recession will brighten your portfolio with some green.

- Avoidable recession?

- Housing recession

- Small business improvement

- April’s Timely preview

- Where will the equity markets go next?

Avoidable recession?

In 2022, The Federal Reserve pivoted from a well-communicated three 0.25% rate hikes to an unprecedented seventeen 0.25% increases! While the US economy has so far proved to be very healthy and resilient when confronted with these hikes, not all stocks fared the same. In particular, short-term traders saw many of the high-flying stocks crash by 60-90%. What is in store for 2023?

The first rate hike of 2023 increased the federal funds rate by 0.25% to a range of 4.5% to 4.75%. If we can believe the Fed, there are two more expected hikes of 0.25% each.

St. Louis Fed President James Bullard told CNBC on February 22, 2023:

- “If inflation continues to come down, I think we’ll be fine,” he said. “Our risk now is inflation doesn’t come down and reaccelerates.”

- He thinks “we have a good shot at beating inflation in 2023” without creating a recession in the US or across the globe.

- “You’ve got China coming on board. You’ve got a stronger Europe than we thought. It kind of seems like the U.S. economy might be more resilient than markets thought, let’s say six or eight weeks ago,” he said.

Time will tell, but it still looks like the overall economy may be able to avoid a severe recession and possibly a recession all together. The end result could have you seeing more green in your portfolio.

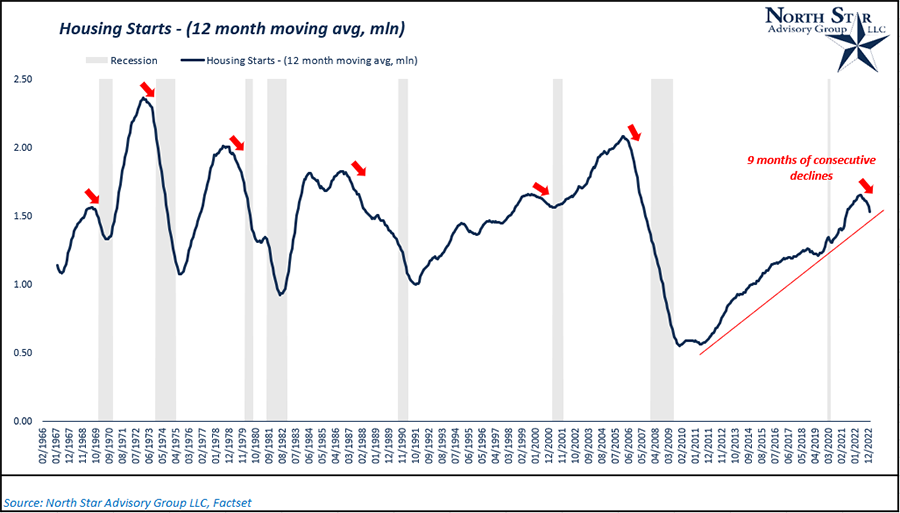

Housing recession

While the initial glance of housing starts data may lead one to think a recession is imminent, a deeper dive may shed light on a builder-specific recession vs a wider spread economic recession.

During the month of January, housing starts fell more than 4% on a month over month basis and more than 20% year over year. Single-family units, which tend to have a greater economic impact than multi-family units, were even weaker, falling by 27% while single-family building permits fell 40% year over year. When looking at the 12-month moving average of housing starts, what started as a gradual deterioration has turned into a more dramatic decline that looks increasingly reminiscent of prior rollovers that occurred during or leading up to recessions. From another perspective, the recent slowdown also appears to be taking out the COVID excess of housing starts and is approaching the slower than historical trendline in place since 2012.

As shown in the chart below, the 12-month moving average of housing starts has now declined for nine straight months, which is the longest losing streak since the Financial Crisis. Going back to the late 1960s, not all nine-month streaks occurred or were immediately followed by recessions, but most of them were.

.PNG)

In January, housing demand started to pick up as 30-year mortgage rates generally fell from recent highs in December around 6.5% to a more modest 5.5%. The high interest rates not only impacts the affordability of new borrowers, it also impacts the profitability of projects for the builders. Builders and investors are starting to delay some projects, which will put downward pressure on commodity prices. The eventual lower cost of materials will bring profit margins back into alignment and building will resume. In the meantime, the slowing of building will likely create an environment where demand stays high enough to create an ecosystem where home prices and rents will not significantly fall.

Mortgage demand’s sensitivity to interest rates can be seen in late February, as 30-year mortgage rates quickly spiked from 5.5% back to 6.5%. This move immediately started to cool new housing demand.

So, while we may have a recessionary environment for single and multi-family home builders, we do not foresee an environment where home prices collapse.

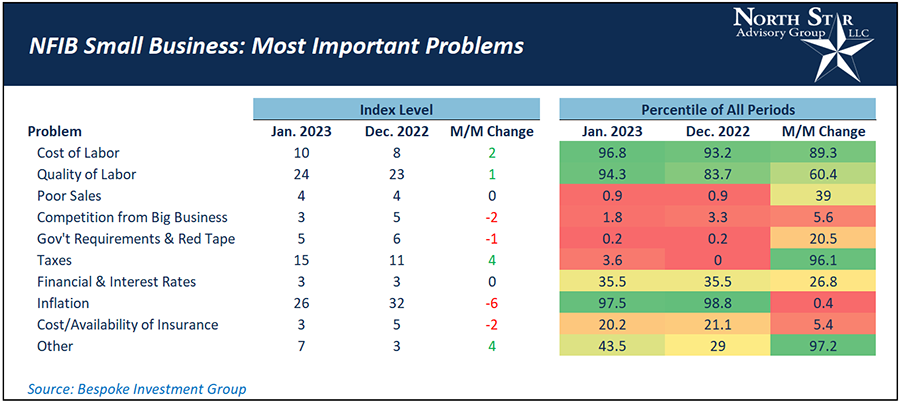

Small business improvement

Count small business owners among the crowd that predicted a recession in 2022. This year 25% less owners expect a recession, but the number of concerned owners is still high.

February’s release of the National Federation of Independent Business (NFIB) Small Business Survey showed fewer and fewer respondents observing price increases. Similarly, while still high, fewer respondents to the survey are reporting inflation as their biggest problem. While the issue remains historically elevated and the predominant issue for small businesses, the percentage of respondents reporting inflation as their biggest issue fell to 26% in January. That’s compared to a peak of 37% last summer. While this reading still has a long way to fall to get back to pre-COVID norms, it is at least trending in the right direction.

Businesses reported that January’s sales were higher than expected, but were not enough to pull down historically high inventory levels. High inventory levels are causing owners to continue with reduced production of new inventory in the coming months. If sales continue at moderate levels, the decreased cost of production should help profit margins this quarter.

In the table below, we break down the percentage of small business respondents that reported various issues as their most pressing this month. As mentioned above, inflation remains the single most commonly reported issue and that reading is also the most elevated with regard to its historical range. However, the six-point decline month-over-month ranks in the bottom 1% of all month-over-month moves.

At the same time, fewer respondents reported costs of insurance to be an issue. Government requirements and red tape also pulled back, albeit that was offset with a 4-percentage point jump (a 95 percentile month-over-month move) in the share reporting taxes as their biggest issue. When it comes to "poor sales," only 4% of small businesses listed this as their number one problem. That’s the same level it was at last month and in the bottom percentile of all readings in the survey's history. When it comes to recessionary indicators, we would expect small businesses to list "poor sales" as their number one problem when things really start to slow down, and that simply hasn't happened yet.

April’s Timely preview

We have already started working on April’s Timely Topics and thought we would preview a few of the topics that we will cover:

- Did you know that investors have one of five very distinct trading styles and mentalities that can influence their portfolio returns?

- Have you ever heard a radio advertisement for an investment that makes money when the markets go up and never loses money when the markets go down and wonder how these investments work?

- Can NSAG find an investment with an 80% return potential and no risk.

Where will the equity markets go next?

Last month, we said we expect a bumpy market for the next few months and the market has not let us down. The rush for lower quality and higher risk assets in January is starting to wear off as investors once again are starting to focus on quality of earnings and cash flow.

We continue to expect a bumpy market for the next few months as companies work through excess inventories, we do not expect that we will test the 2022 lows anytime soon. In fact, many of the larger bears on Wall Street and in the fund companies that we work with are starting to turn positive on the global economies. China is opening up, which may lead to a wave of Chinese travel and consumption. China’s reopening has led to a massive speculative rebound in their market, which has put China solidly into an over-extended valuation. Due to a warmer European winter and large shipments of fuel from the US, the energy crisis is not as severe in Europe or the US. In fact, Germany has excess gas supplies right now.

Equity markets will continue to be focused on earnings in 2023. As of 2/28/2022, the S&P 500’s aggregate 2023 earnings per share (EPS) estimate stands around $221.59, down from an estimate of $229 on 12/31/2022. To dive deeper, over the past month, 198 S&P 500 companies had their 2023 EPS estimates revised upwards, while 301 had their estimates revised downwards. Coming out of the most recent earnings season, in general, Q4 2022’s actual EPS numbers were stronger than expected with around 70% of companies exceeding expectations, while guidance for 2023 has been a bit weaker than expected. This announced EPS reductions in February of approximately 3.2% accounts for most of the S&P 500’s February decline of decline of 3.5%. Time will tell if management teams are “sandbagging” their performance guidance, essentially building in some room for error.

We are passionately devoted to our clients' families and portfolios. Contact us if you know somebody who would benefit from discovering the North Star difference, or if you just need a few minutes to talk. As a small business, our staff appreciates your continued trust and support.

Please continue to send in your questions and see if yours gets featured in next month’s Timely Topics.

Best regards,

Mark Kangas, CFP®

CEO, Investment Advisor Representative