Each month we ask clients to spend a few minutes reading through our newsletter with the goal of raising their investor IQ. This month we kick off 2023 with a quick recap of last year and what we favor for 2023.

- 2022 Recap

- 2023 Street consensus

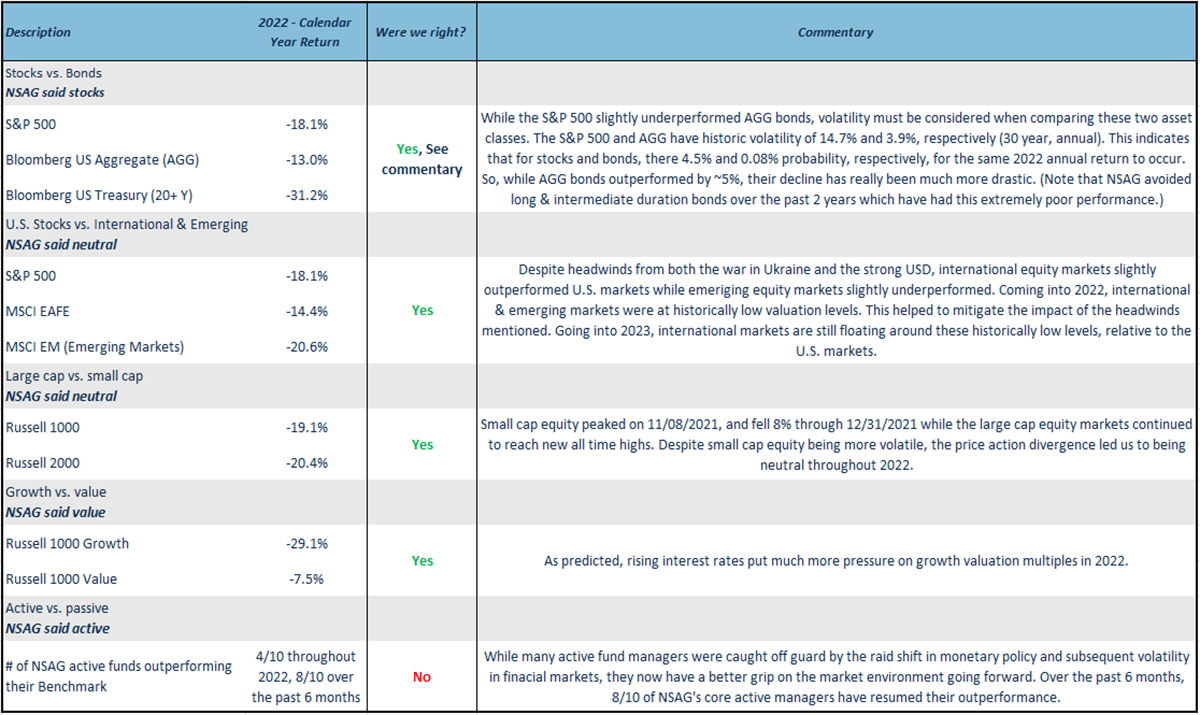

- Stocks vs. bonds

- U.S. stocks vs. international and emerging stocks

- Large cap vs. small cap

- Value vs. growth stocks

- Active vs. passive management

2022 Recap

As we head into 2023, North Star recaps a volatile 2022. If we rewind one year, NSAG laid out its 2022 outlook in the January 2022’s Timely Topics issue. Looking back, we want to know exactly where we were right and wrong, as we continue to help our clients navigate the complex and ever-changing financial markets. Click here to review last year’s macro-outlook.

2023 Street consensus

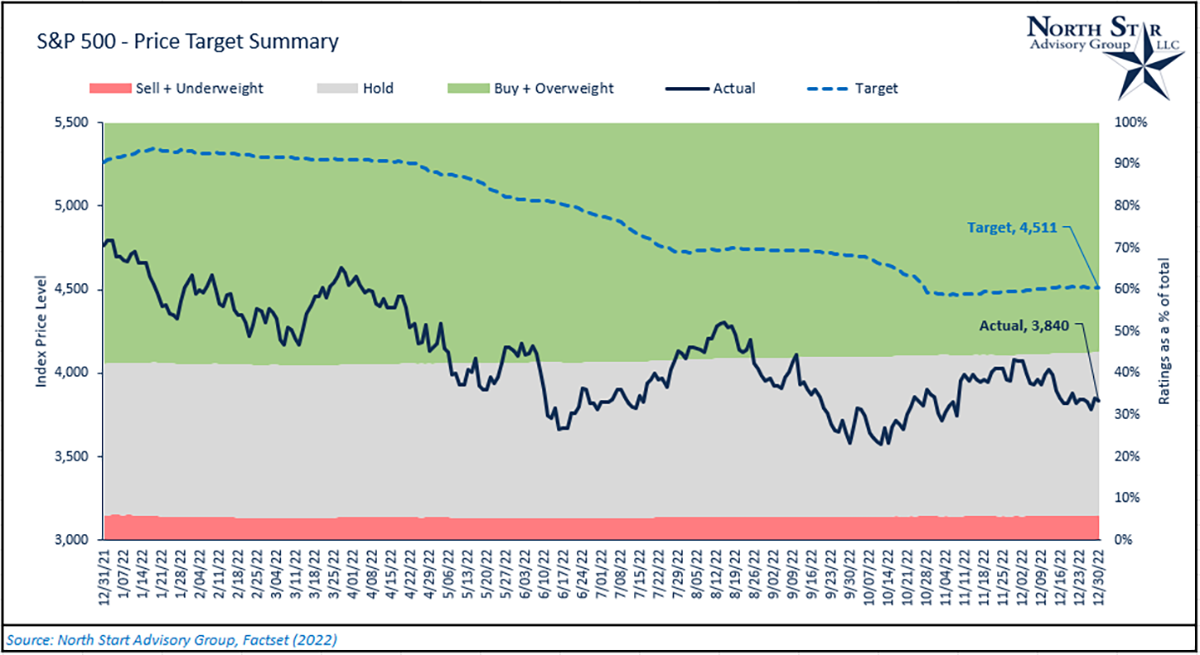

As of 12/31/2022, the consensus median price target for the S&P 500 for 12/31/2023 currently stands at 4,511. This represents an implied upside of ~17% for 2023. To get a better understanding of where analysts currently view the overall market, we are going to recap the changes in price targets throughout 2022, and the historical accuracy of annual forecasts over the past 20 years.

As of 12/31/2022, the consensus median price target for the S&P 500 for 12/31/2023 currently stands at 4,511. This represents an implied upside of ~17% for 2023. To get a better understanding of where analysts currently view the overall market, we are going to recap the changes in price targets throughout 2022, and the historical accuracy of annual forecasts over the past 20 years.

For more context, the chart below represents the actual S&P 500 price level in the solid dark blue line versus the aggregate price target in the blue dashed line over the past 12 months. The aggregate price target encompasses 12-month price targets for all 500 index constituents from various Wall Street analysts. Each constituent can have in excess of 30 different analyst inputs. In the background, we aggregate the % of index constituents that have either a sell + underweight, hold, or buy + overweight rating. Over the past 12 months, aggregate ratings have been little changed (buy, sell, etc.), while overall price targets have come down. Currently, around 6% of constituents have a sell or underweight rating, 39% have hold ratings, and 55% have a buy or overweight rating.

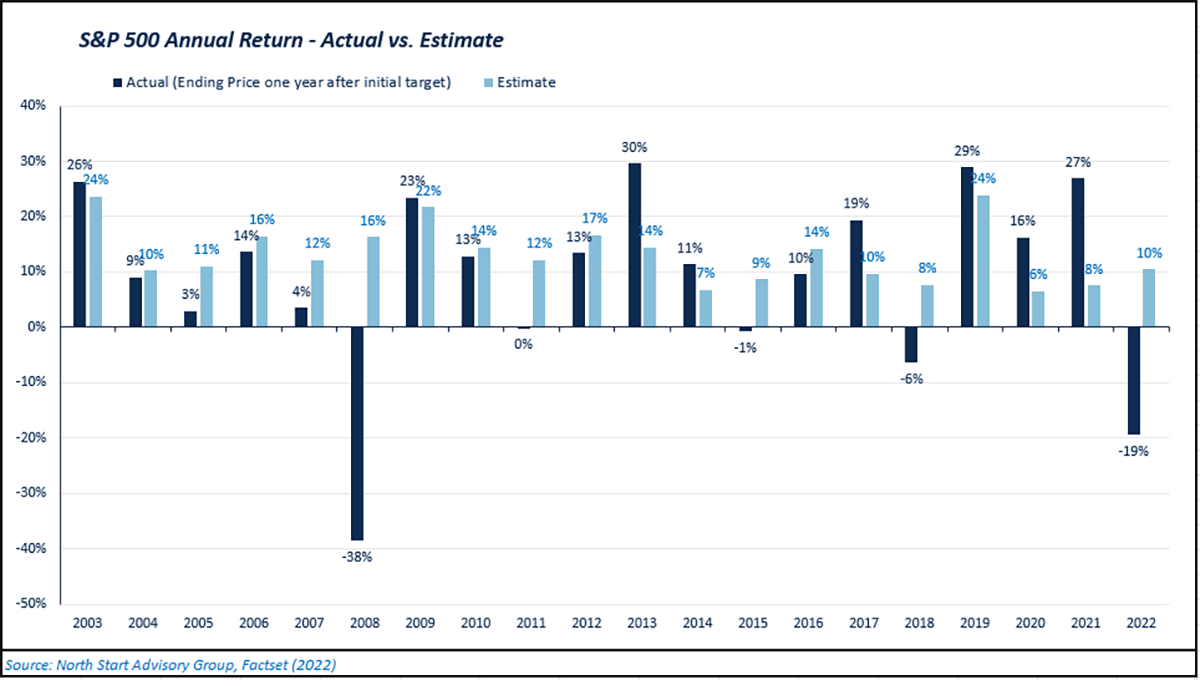

While the above chart can be helpful to get an understanding on the overall market’s outlook, historical accuracy should be highly considered. Over the past 20 years, we compared the 12-month price target at the beginning of each year versus where the index’s price actually finished that year. On average, aggregate estimates were overestimated by 4.0%. These errors were volatile, and the estimates were only within +/- 4% of the actual price return 6/20 years (~30% of the time). It’s interesting to note that over the past 20 years, analysts have not forecasted a down year.

In the table below, we also summarize the Wall Street’s consensus estimates for various key macroeconomic data points for the U.S. economy.

Stocks Vs. Bonds

Looking toward 2023, we continue to favor stocks over bonds. Although, higher interest rates have created an environment where our stock preference is no longer as one-sided as it has been over the past two to three years.

Looking toward 2023, we continue to favor stocks over bonds. Although, higher interest rates have created an environment where our stock preference is no longer as one-sided as it has been over the past two to three years.

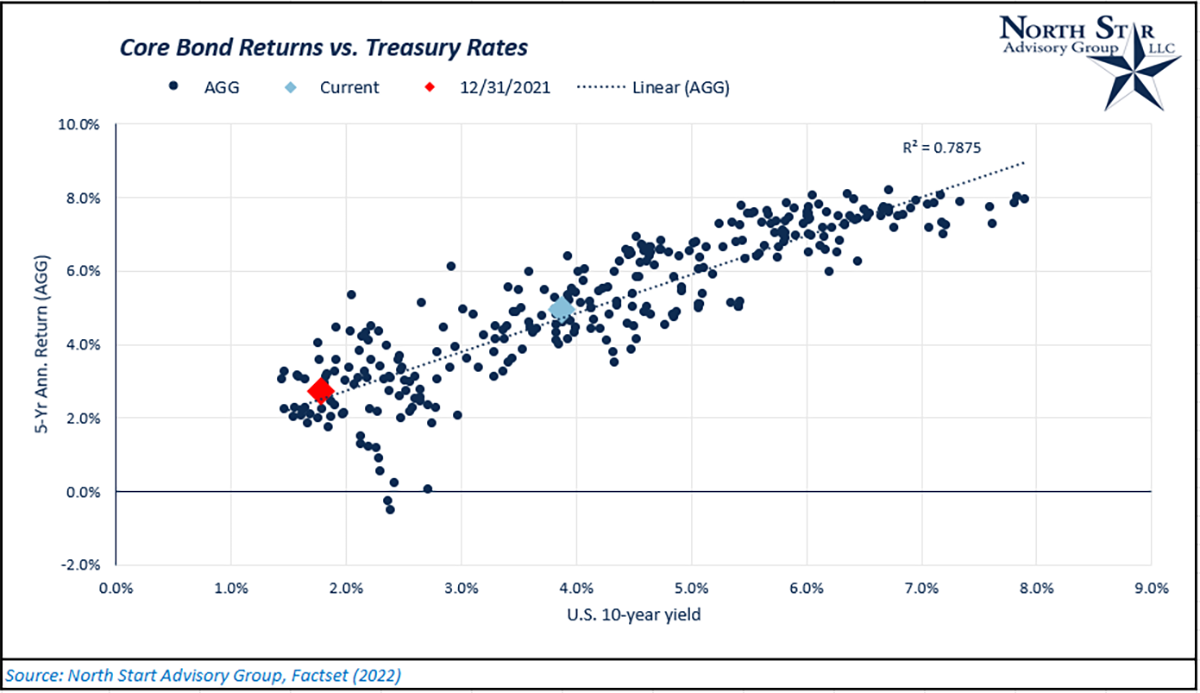

In 2022, treasury rates have risen more than 2 times for long-term maturities (more than 10 years) and 3-5 times in some short-term maturities (less than 5 years). This rapid rise in rates, have led to the worst year ever in the bond market when evaluated on historical annual performance. Additionally, rates were coming off near-zero levels from the pandemic-related monetary policy, causing even more performance pain. Most of the pain was felt in intermediate (5-10 year) and long-term bonds which NSAG has been avoiding over the past two to three years. Although, due to this pain, the risk/return profile in the bond market has been greatly improved moving forward. Currently, we can get 4-5% on CDs and investment grade corporate bonds. In the following chart, “Core Bond Returns vs. Treasury rates,” we analyze 30 years of historical 10-year treasury rates and each subsequent 5-year annualized return for the Bloomberg Barclays Aggregate Bond Index (AGG). The light blue diamond represents where we currently stand, while the red diamond represents where we were at in the beginning of 2022. The positive relationship between treasury rates and subsequent bond returns is strong. Overall, we’d still recommend short-term and some intermediate-term bonds moving forward.

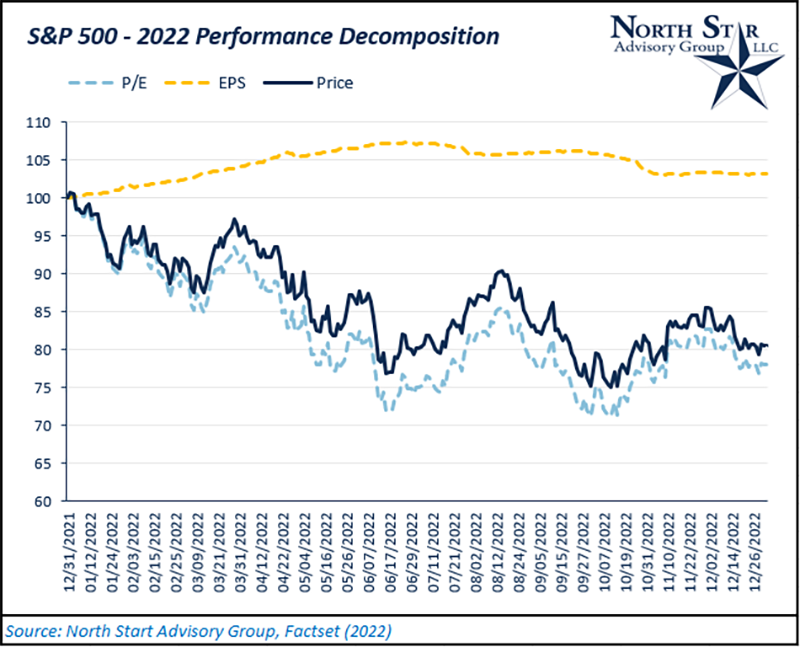

While bond return profiles have greatly improved through 2022, stock return profiles have also improved in comparison to where they were at the beginning of 2022. When the Federal Reserve tightens monetary conditions (rate hikes + balance sheet reduction), pressure was put on stock valuations and caused many stock prices to come down. Using the S&P 500 Index as a proxy for stocks, the index was down -19% in 2022. Valuation (P/E) compression drove -22% of the decline in the index, while earnings growth (EPS) drove +3%. This implies that 115% of the index’s performance for 2022 came from valuation compression, mostly triggered by the Federal Reserve.

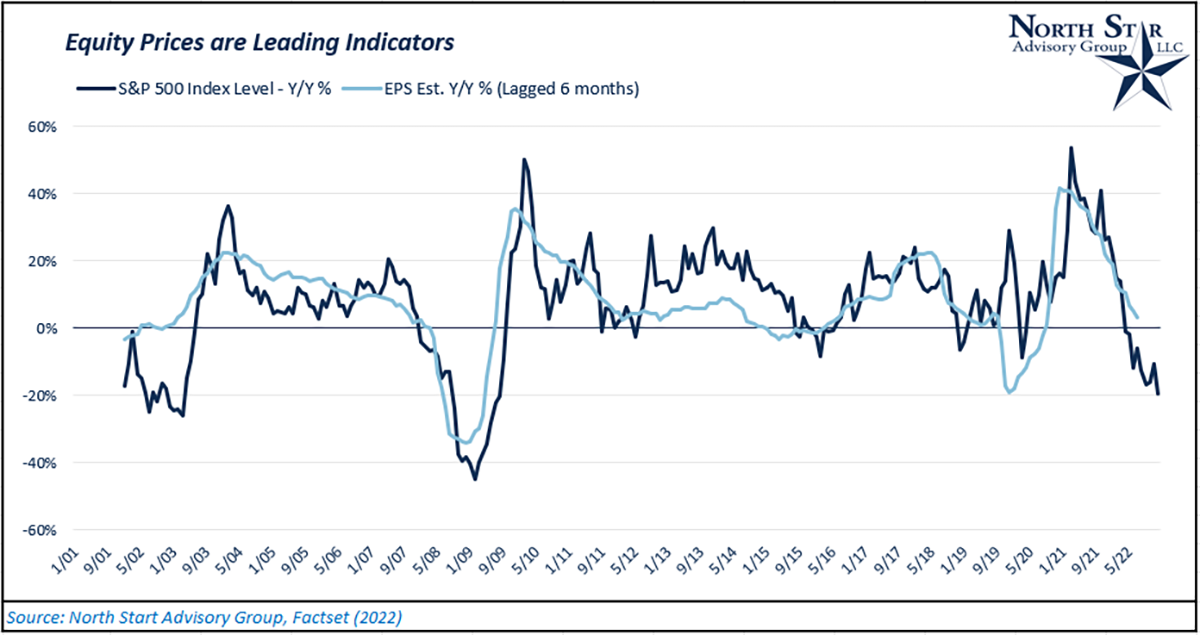

Looking to 2023, the stock conversation is likely to be laser-focused on economic growth and corporate earnings growth as the driver of stock returns. Currently, the S&P 500 is forecasted to grow earnings by 4.6% year-over-year. Assuming no change in valuation levels or share counts, this would imply a 4.6% return on the S&P 500 in 2023. Although, we must remember that forecasts are not always accurate in either direction. A more accurate earnings estimator may be the actual price level for stock indices. Stock prices are one of many “leading indicators.” Stock prices tend to forecast economic cycles before they happen in either direction. In the chart below, “Equity Prices are Leading Indicators,” we can analyze the relationship between EPS estimates and stock prices. While there may still be some short-term volatility, the equity markets have sold off throughout 2022, and prices tend to bottom before the real economy bottoms.

The impacts from tight monetary policy will continue to trickle through the economy as the Fed continues its fight against inflation. In December’s Fed meeting, the FOMC forecasted a peak policy rate of 5%-5.25%, implying 3-4 more 25bps rate hikes in 2023. On the other side of the coin, the consumer has shown continued strength throughout 2022 as wages have grown along with consumer prices and excess savings are spent down. There is still ~$600 billion of excess pandemic savings in the economy heading into 2023 (as of 11/30/2022). Based on the run, rate since the excess savings peaked in December 2021, this spending of excess savings could continue through May 2023 before the consumer would have to take out debt to maintain the same spending patterns.

Lastly, we continue our constant due-diligence process on our actively managed equity fund lineup and believe that there will be opportunities to outperform the overall equity market in 2023. More on this subject in “Active vs. Passive Management.”

U.S. stocks vs. international and emerging stocks

In 2022, NSAG was neutral on U.S. stock vs. international and emerging stock. While the rising USD and war in Ukraine acted as headwinds to the international and emerging markets in 2022, performance was still relatively in line with U.S. stock performance. Going into 2023, we slightly favor the international and emerging markets over U.S. stocks.

In 2022, NSAG was neutral on U.S. stock vs. international and emerging stock. While the rising USD and war in Ukraine acted as headwinds to the international and emerging markets in 2022, performance was still relatively in line with U.S. stock performance. Going into 2023, we slightly favor the international and emerging markets over U.S. stocks.

Catalysts for international and emerging stock in 2023 include:

- Falling USD

- Historically low valuation levels

- Higher dividend yields

- China re-opening, Russia/Ukraine resolution (although, both of these catalysts are extremely hard to predict and aren’t weighed heavily into our thesis)

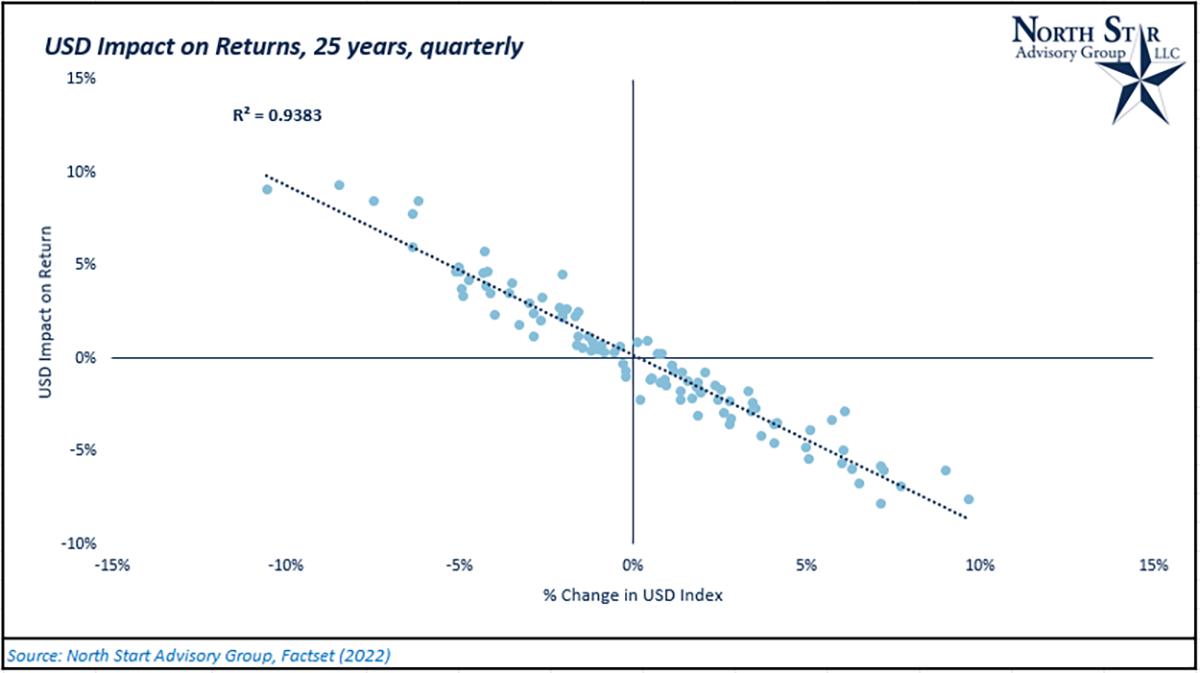

While there are many variables that affect currency values, interest rate levels are a primary driver. In 2022, we’ve seen the Federal Reserve hike interest rates at a historically fast pace. The pace of rate hikes in the U.S. greatly outweighed many foreign central bank policies, leading to higher interest rate levels in the U.S. compared to many foreign nations. Higher interest rates generally attract foreign direct investment (FDI), which strengthens that countries currency. In this case, the U.S. has seen increased FDI. In the stock markets, the USD and international and emerging stock returns display an inverse relationship. As the dollar rises, international returns tend to be lower, and vice versa (Seen in chart, “USD Impact on returns”).

In Q4 2022, we’ve seen the U.S. Dollar begin stabilizing and rolling over towards its long-term trend (as seen in chart, “USD Index – Price Level”). As FDI impact tends to be short-term, and many foreign central banks continue hiking interest rates, we expect this falling trend to continue for the USD, acting as a tailwind for international returns.

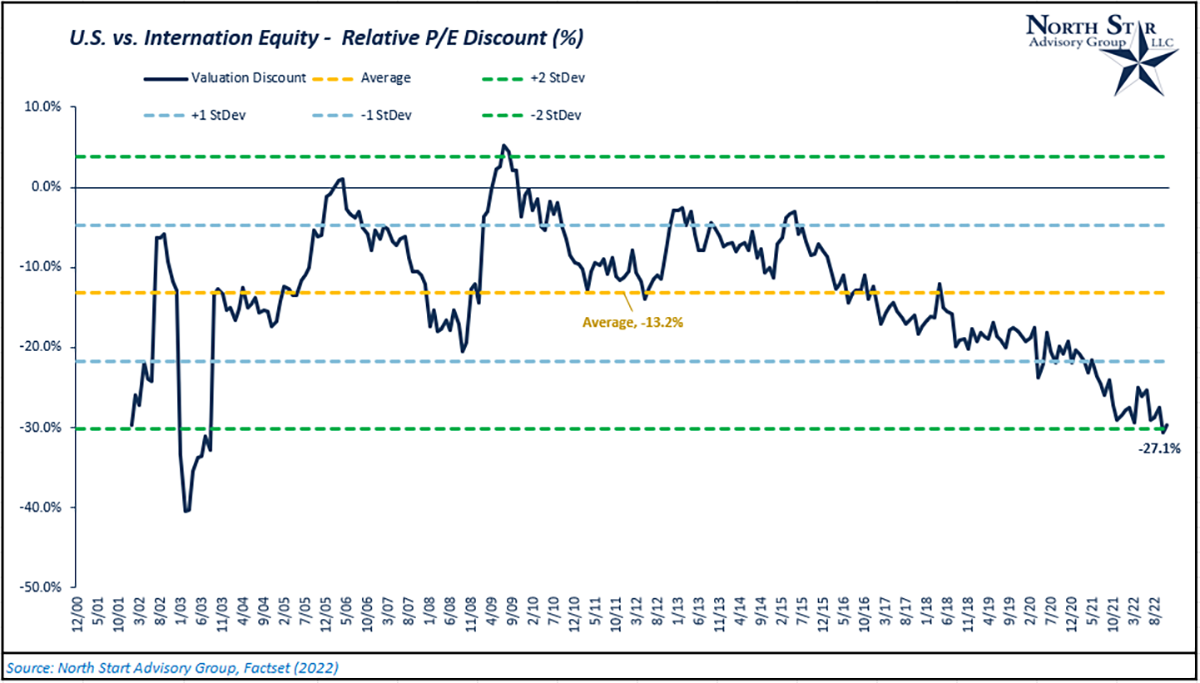

When comparing valuation levels, international markets are still at historically lower levels relative to U.S. markets. Looking at the P/E ratio for the MSCI EAFE Index relative to the S&P 500, international stocks are at a 27.1% discount as of 12/31/2022. Over the past 22 years, on average, this discount has historically been 13.2%. The current discount is two standard deviations below the average (Seen in chart, “U.S. vs International Equity”). Over the course of the next few years, we expect mean reversion in these markets to occur which may include two main factors:

- A re-rating in valuation levels in the international markets could drive relative outperformance versus U.S. stocks.

- A declining of valuation in technology stocks would impact the U.S. stocks more than international markets.

On the other hand, if the global economy does slow down or weaken to a degree in 2023, we’d like to be overweight in stocks with lower valuation levels and higher dividend yields. Historically speaking, these two factors tend to decrease the implied risk and volatility for equity holdings.

Lastly, while extremely hard to predict, a re-opening of China, or some level of resolution in Ukraine could lead to additional re-ratings of both international and emerging stocks. As these two factors are very difficult to forecast, we are not weighing them heavily into our thesis. Although, it is likely that these two factors are sitting at their worst possible levels.

Large cap vs. small cap

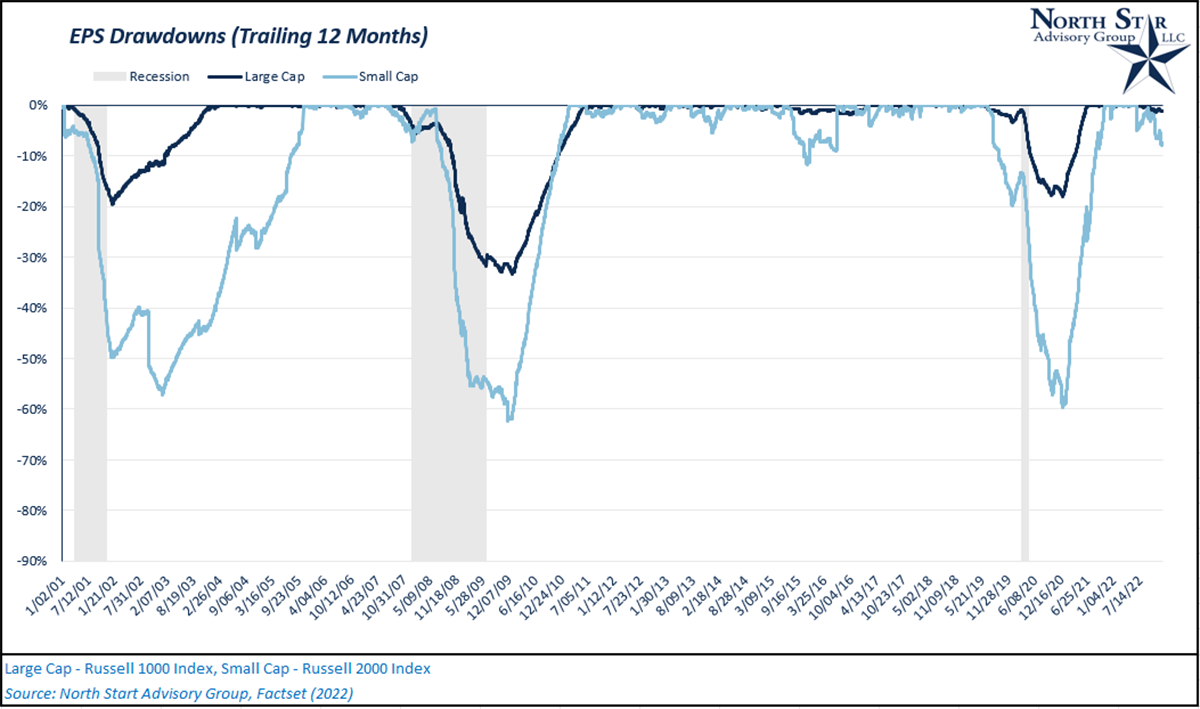

In 2022, large cap stocks and small cap stocks had performance of -19.1% and -20.4%, respectively. Going back further, the trailing two-year total returns were 2.27% and -8.64%, respectively. Over that same two-year period, large-cap EPS grew ~30% and small-cap EPS grew ~22%. So, over the past 24 months, we’ve seen a price divergence between the two cap groups.

In 2022, large cap stocks and small cap stocks had performance of -19.1% and -20.4%, respectively. Going back further, the trailing two-year total returns were 2.27% and -8.64%, respectively. Over that same two-year period, large-cap EPS grew ~30% and small-cap EPS grew ~22%. So, over the past 24 months, we’ve seen a price divergence between the two cap groups.

Why has this price divergence happened? Looking to 2023, the street is currently forecasting a decline in small-cap EPS, while large-cap forecasts remain slightly positive. During economic downturns or recessions, small-cap earnings tend to be more volatile in comparison to large-cap earnings. We can see this fact in the following chart, “EPS Drawdowns.”

Due to the declines many small-cap stocks have already experienced, valuations have a potentially attractive entry range for long-term investors. The current valuation level for small cap stocks is what makes this potentially attractive. As we’ve discussed on numerous occasions, the price you pay for an investment is a primary driver of your potential returns. In the chart, “P/E Entry Point vs. Subsequent Returns,” we analyze the relationship between the price paid at a hypothetical entry point and the subsequent 5-year annualized return. This relationship is based on the 22 years of monthly data on the Russell 2000 Index. Remember, equity prices tend to bottom prior to fundamentals (EPS) bottoming.

Going into 2023, we slightly favor mid and small cap stocks over large cap stocks.

Value vs. growth stocks

Moving into 2023, NSAG remains bullish on value versus growth stocks. To quickly recap, here is a breakdown of the typical characteristics seen in both styles of stocks.

Moving into 2023, NSAG remains bullish on value versus growth stocks. To quickly recap, here is a breakdown of the typical characteristics seen in both styles of stocks.

Growth:

- Higher valuation levels (P/E, P/B, etc.)

- Higher intermediate- and long-term growth estimates.

- Generally, less cyclical earnings (depending on the sector)

Value:

- Lower valuation levels

- Lower intermediate- and long-term growth estimates.

- Generally, more cyclical earnings (depending on the sector)

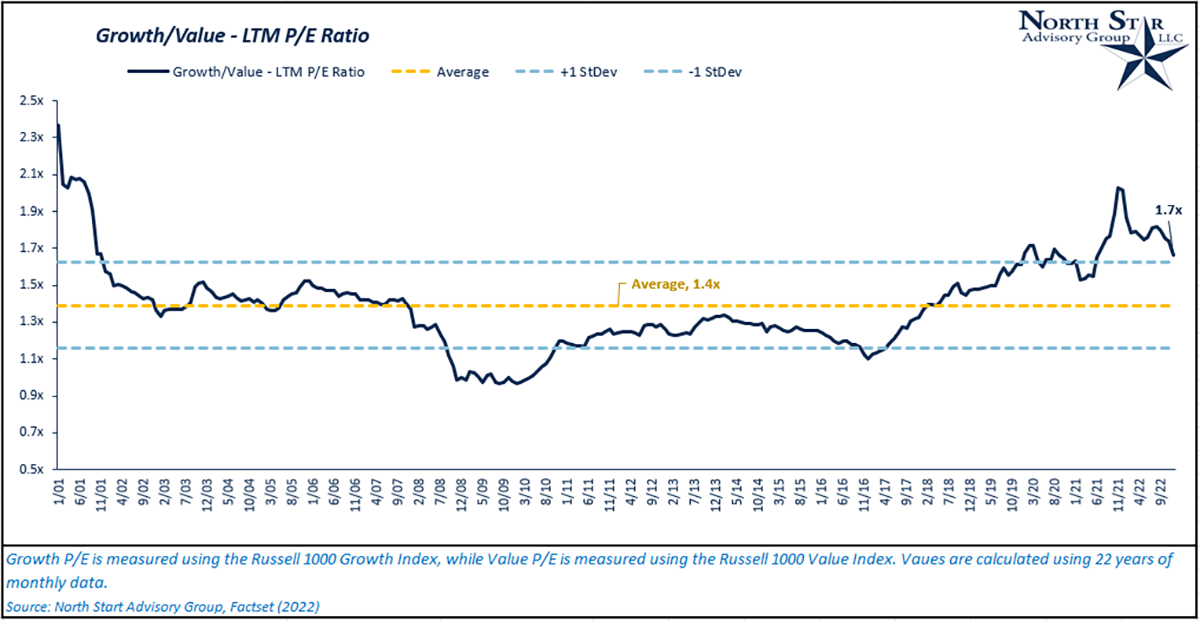

Growth equity will almost always trade at a valuation premium to value stocks, as future earnings estimates are weighed more heavily into the price of these stocks. Over the past 22 years, the average premium for growth stocks has been right around 40%. Currently, this premium stands at ~70% based on relative P/E ratios. While valuations across different market segments and styles have fallen in 2022 (growth valuation levels experience the most pain), the premium still remains elevated compared to its historical average. The premium over time can be seen in the chart, “Growth/Value – LTM P/E Ratio.”

Within value stocks, you’ll tend to find more exposure to cyclical parts of the economy. Cyclical refers to the level of sensitivity to the different business cycles. Cyclical sectors include energy, industrials, utilities, financials, consumer discretionary, and materials. While not every company in these sectors has the same level of cyclicality, the general theme remains in-tact. The Russell 1000 Value Index currently has a ~54% exposure to these six sectors, while the Russell 1000 Growth Index has exposure of ~32%. This is one of the reasons why value stocks generally performed better in 2022 versus growth stocks. If the economy does experience a recession, we would expect growth earnings to be somewhat more resilient when compared to value. Although, as discussed above, the price you pay for a stock greatly matters.

We still favor value over growth stocks in 2023, but it is no longer as one-sided when compared to 2022’s outlook.

Active vs. passive management

Heading into 2023, NSAG continues to believe that active management will generate strong relative performance and alpha for our clients. While we favored active management going into 2022, we are leaning even harder on active management going into 2023.

Heading into 2023, NSAG continues to believe that active management will generate strong relative performance and alpha for our clients. While we favored active management going into 2022, we are leaning even harder on active management going into 2023.

The past twelve months of volatility has created many dislocations within both the equity and fixed income markets. When financial markets go through stressful and volatile time periods, assets have a higher probability of being priced incorrectly. When an asset’s true intrinsic value is not equal to the asset’s market price, opportunities to generate alpha are created. In order to capitalize on these opportunities, we need to be actively discovering them and taking advantage in a timely manner.

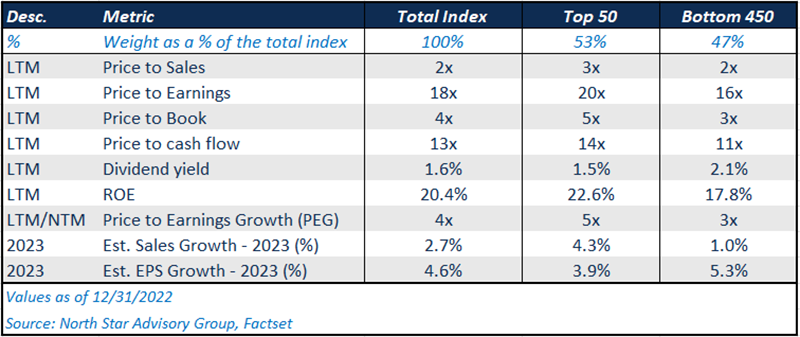

From a high level, let’s explore this topic further by analyzing the table below which compares the S&P 500 Index against the top 50 names in the S&P 500 and the bottom 450 names in the S&P 500.

The S&P 500 Index is a price-weighted index of the 500 most followed large cap companies in the U.S. “Price-weighted” means that each constituent’s weight is calculated as the constituent’s respective market capitalization divided by the sum of all constituent market capitalizations. By default, the largest companies are going to have the highest weights.

In the above table, we deconstructed the index into three custom indices: Total Index, Top 50 holdings, Bottom 450 holdings. For each group, the metrics are calculated as of 12/31/2022. The two growth estimates are calculated based on consensus Wall Street estimates for each constituent in the respective group. For this exercise, let’s assume these growth estimates are accurate.

- If you were to buy the “Total Index,” you’d be paying a multiple of 18x on earnings with a 1-year growth rate of 4.6%.

- If you were to buy the “Top 50,” you’d be paying a multiple of 20x on earnings with a 1-year growth rate of 3.9%.

- If you were to buy the “Bottom 450,” you’d be paying a multiple of 16x on earnings with a 1-year growth rate of 5.3%.

As a general rule of thumb, we’d like to pay a lower multiple with higher growth rates. This is where active managers can make a difference by strategically picking through the bottom 450 and reducing exposure to certain names in the top 50.

Hopefully in the end, using an active manager allows clients to find the best names, where intrinsic value is greater than the market price. In doing so, the risk of exposure to names that may be overpriced will be minimized.

We are passionately devoted to our clients' families and portfolios. Let us know if you know somebody who would benefit from discovering the North Star difference, or if you just need a few minutes to talk. As a small business, our staff appreciates your continued trust and support.

Please continue to send in your questions and see if yours gets featured in next month’s Timely Topics.

Adios to 2022 and cheers to the start of 2023!

Best regards,

Mark Kangas, CFP®

CEO, Investment Advisor Representative