Each month we ask clients to spend a few minutes reading through our newsletter with the goal of raising their investor IQ. There is nothing spookier than politicians that can’t get along. This month we cover a few of the tricks and treats that are coming out of Washington.

- Slashing Social Security benefits

- Largest Social Security raise in 40 years

- The great deflationary migration

- Climbing the wall of suspense

- NSAG News - Recession risk remains at historic lows

- Where will the equity markets go next?

Slashing Social Security benefits

The pending Social Security benefit reductions have people more scared than a slasher movie on Halloween. We have been planning for the changes for last two decades and the results will likely be more PG-13 vs Nightmare on Pennsylvania Avenue.

Washington has tricked the public for decades by providing the coveted Social Security statements with green bars across the top showing estimated benefits at various ages. However, buried in the fine print many have missed important disclosures. First, the trust fund is anticipated to reach the point of being insolvent in the early 2030s. This has caused many clients to improperly assume that the trust funds would be gone and benefits would be no longer paid out. While it might be a conservative approach to assume a $0 future benefit, this approach put an unnecessary stress on retirement cash flow projections.

The second detail missed is the most crucial. When the trust fund becomes insolvent, it is anticipated there will only be enough funds to pay for 78-80% of the anticipated benefits shown on the very same statement! I find it highly unlikely that Washington will proceed with reducing benefits to those who are already receiving them. Here are the options that could be taken to avoid social unrest:

- Raise Taxes… Washington has struggled to raise taxes and we don’t see their success being any easier here. In 2021, Social Security's Old-Age, Survivors, and Disability Insurance (OASDI) program taxes earned income up to $142,800 at a combined employee/employer rate of 12.4%. There is potential precedent to increase or remove the income cap. In 1993, Medicare's Hospital Insurance (HI) program’s income cap was removed. Recent conversations have shifted to create a donut hole with taxation resuming for earned income in excess of $400,000. The donut hole strategy will likely gain more support and significantly increase the amount of taxes being paid by top earners.

- Push back the retirement age… Since this option has been chosen before, we see this as the most likely. Social Security was never intended to provide benefits for 20-40 years. Medical advancements continually increase life expectancy and Social Security’s start date has not moved in a similar rate. Politicians will likely consider making adjustments to those who are at least 10-15 years away from their current full retirement age. This will provide plenty of time those impacted to adjust their retirement plans.

- Reduce benefits… I see a low probability of a reduction of benefits for low income families and current benefit recipients. Digging into the benefits formula, income earners below $50,000 receive a higher payout ratio from Social Security compared to what was contributed to those earning more than $50,000

- Asset or income phase out… Currently, Social Security is paid out regardless of asset level or retirement income. While I expect increased conversations around this topic, the reality is that additional phase outs will likely not significantly increase the financial strength of the Social Security Trust and distract from the tougher conversations that need to happen

- Removal/adjustment to COLA… Every year benefits are eligible for changes in cost-of-living adjustment based on various inflation items. Many pensions do not receive a COLA and I would not be surprised to see Social Security make a similar adjustment.

The end result will likely be a combination of adjustments noted above. While only time will tell how these conversations will proceed, we expect the net result will be an approximate reduced benefit of 20%, by waiting longer and/or less income to those who are at least 10-15 years away from their full retirement age.

Largest Social Security raise in 40 years

A long-awaited announcement for Social Security and Supplemental Security Income (SSI) beneficiaries is out. In line with expectations, 2022’s benefit will receive a 5.9% cost of living adjustment. Benefits increase on average by 2.6% and this is the largest benefit increase since 1982! The change is calculated by change in the Consumer Price Index (CPI-W) from the third quarter of 2020 through the third quarter of 2021. Ironically, paying out a larger benefit is like pushing the gas pedal down harder as you are speeding toward the cliff of the Social Security Trust fund becoming insolvent.

You might be interested to hear that North Star is expecting a small to 0% increase for 2023. Coming out of the global financial crisis, 2008’s benefit increase was 5.8% yet the rate of increase was 0% for 2009 and 2010. Energy and technology prices are a major contributor to the CPI-W for 2022’s benefit. However, both energy and technology have been deflationary pressures over the last few years and we expect this pattern to return for 2023’s benefit calculation.

Another important change for 2022 is that any income earned up to $147,000 will be taxed for Social Security (OASDI only). This amount is up 2.9% from 2021’s limit of $142,800.

The great deflationary migration

In a search for cheaper offices, labor and residences, west coast companies are quickly moving from California to Texas and east coast companies are moving from New York City to Florida. Across the country we are seeing urban sprawl as the primary driver for housing demand. While this trend is being accelerated by a large adoption of work-from-anywhere, thanks to COVID, we have been expecting this move for years. Millennials are the largest group by population and they have been under consuming homes and cars for a decade. Their desire for space for their growing families and cars to drive their kids to soccer practice will be a driving force of demand over the next decade.

Climbing the wall of suspense

A good suspense movie has more than a few twists and turns. 2021’s economic expansion will be no different. For almost 20 years, I have been playing a mental exercise that I like to refer to as “I read online…”. This month I am providing a sample of the of questions and concerns that clients have raised from their headline readings over just the first 15 days of October 2021. For each item I have included my counterpoints to help understand and deflate each potential risk.

- The scariest part of Halloween this year is the supply chain. A record number of container ships continue to sit anchored outside of US ports. This not only puts holiday sales at risk, but many parts of the supply change for virtually all companies across the country. We are even aware of additional potential delays like the Chinese New Year. Normally, when issues facing the economy are front and center on everyone's mind, it means that they are priced into the market. We reviewed Google search trends for Labor Shortages, Supply Chain and Inflation and found that all three headwinds at search levels never seen before, it's hard to argue that these are occurring behind the scenes and are not already mostly priced into the market.

- The Build Back Better Agenda is an ambitious $7 Trillion plan to create jobs, cut taxes, and lower costs for working families by increasing taxes on families earning over $400,000 and large corporations. Democrats recently proposed several $3.5 Trillion packages. We continue to hear from our contacts in Washington that Democrats did not have the votes to support these packages. In recent days we are now hearing that Nancy Pelosi and other Democrats are not only considering ways to reduce the scope of the $3.5 Trillion bill, but they are considering cutting programs all together from the bill.

- While Sen. Elizabeth Warren has intensified her opposition to Jerome Powell’s renewal appointment when his term ends in February 2022, Biden has recently stepped up to support Powell. While some Democrats and Republicans argue that Powell is being too accommodative for too long, we see his transparent wait and see approach as refreshing and well forecasted. While the future does hold a rapid and coordinated winddown of accommodation from Federal Reserves around the world, we expect Powell to remain consistent and flexible to adjust the slowdown based on current conditions.

- The largest pilots association, along with United Airlines, American Airlines, Southwest Airlines, JetBlue, Alaska Airlines and Hawaiian Airlines are supporting requirements for workers to get the COVID vaccine. Just a few weeks after the union representing American Airlines warned that staffing shortages could start as the holiday travel season begins if employees lose their jobs for refusing to get the COVID vaccine, Southwest Airlines canceled more than 1,800 flights. The US currently has recommended vaccination for more than 16 potentially harmful diseases that can be very serious, may require hospitalization, or even be deadly. Overtime, we foresee more schools, businesses and entities adding the COVID vaccine to their recommended list, which will continue to temporarily shift employees to employers that meet their vaccine comfort.

- It is easy to throw in the towel on investing in international stocks. The combination of falling interest rates and outsize growth of technology stocks in the US has driven our outperformance over the last few years. Going forward, we may experience a different performance paradigm. International stocks may benefit from a higher dividend yield, higher COVID vaccine rates, and price-to-earnings multiples roughly 30% lower than the US.

- On October 8, one client asked if they should exit the stock market based on a radio commentator saying, “the last two years in the market have been the best two years in the last 50 years.” We are so glad that we have built a trusting environment with our clients. This simple question helped to protect a client from misinformation and bad decisions. Not only has the market gone up since this date, but the commentator’s comments also were false! Over the past 45 years, there have been 75 periods or 15% of the time where the rolling two-year returns were better than where we stood on September 30, 2021.

- Bank stocks are struggling again this summer after underperformed growth stocks over the last few years. What is going to bring them back? Rising interest rates and better-than-expected loan losses will help to drive profits to the bottom line.

- Headlines and politicians are predicting that Oil prices could temporarily hit $100 by yearend. Several factors are at play, including supply disruptions, increased demand in Europe due to green energy shortages and increased demand for oil as a raw material for products. We have experienced rapid price inflation, however we expect many of these pressures to ease and create deflationary pricing pressures 12 months out.

- In October, The United States reached its debt ceiling or legislative limit on the amount of national debt that can be incurred by the U.S. Treasury, thus limiting how much money the federal government may pay on the debt they already borrowed. Since 1980, The United States has averaged more than one debt ceiling raise or suspension per year and almost 1.5 per year since 2008. A harsh lesson was learned by politicians in 2011 when The United States reached a crisis point of near default and the delay in raising the debt ceiling resulted in the first downgrade in the United States credit rating, a sharp drop in the stock market, and an increase in borrowing costs. We view the likelihood of this event repeating as very low and politicians quickly moved to find a resolution to avoid/delay a default this month.

- Buy now pay later is making a big come back. While household debt service ratios have hit 40-year lows, consumers are once again looking at ways to make purchases for items that they do not have the cash on hand to afford. While this is a concerning trend, the relative volume of dollars will be small for many years and therefore we will continue to monitor this sector of consumer debt financing.

- A colder and snowier winter expected for this year. Harsher winter weather could cause a positive demand for winter sporting goods and while further stressing the current shortage of snowplow drivers. Looking back at prior seasons, localized disruptions due to cold, snow or ice tend to be isolated to a few days and have minimal impact on the overall economy.

- The COVID-19 wave 3 surge had been predicted to be worse and longer than it is turning out to be. Further, there was much concern that a potential harsh winter in the US will increase cases as people are forced indoors. Our forecasting is on target for a short-lived and less impactful wave. Roughly 80% of the population now has some level of immunity due to either the vaccine, infection or both.

- For months now Evergrande has been increasing their risk of default. This growing financial crisis in China and recent headlines have scared investors into thinking they are the next Lehman Brothers. The reality is that while Evergrande is at a risk of default, they have a lot of physical assets and divisions that could be sold to reduce their liabilities. This was not the case for Lehman who got into trouble for synthetically creating derivatives products that were not backed by physical assets.

- A countdown is on for several Chinese companies being delisting in the US. This is an accounting and transparency fight that is 20 years in the making. Each company has a chance to stay listed if they comply with existing accounting and reporting standards with which other listed companies already comply. This push will help to increase the safety of investors.

- The IRS wants to look at your bank account and we are ok with it. As digital and gig parts of the economy evolve, the IRS needs to continually enhance their technology to increase their ability to monitor and collect taxes where applicable.

- For added measure, I will add one positive headline for the month. The potential rollout of a COVID-19 pill. In a similar application as Tamiflu, this inexpensive and easy to administer pill is taken four capsules twice a day for five days starting within five days after patients experienced the first symptoms of COVID-19. When the drug enters your bloodstream, it blocks the ability of the SARS-CoV-2 virus to replicate. We view this development as a potential game-changer in mentally and physically returning to normal around the globe.

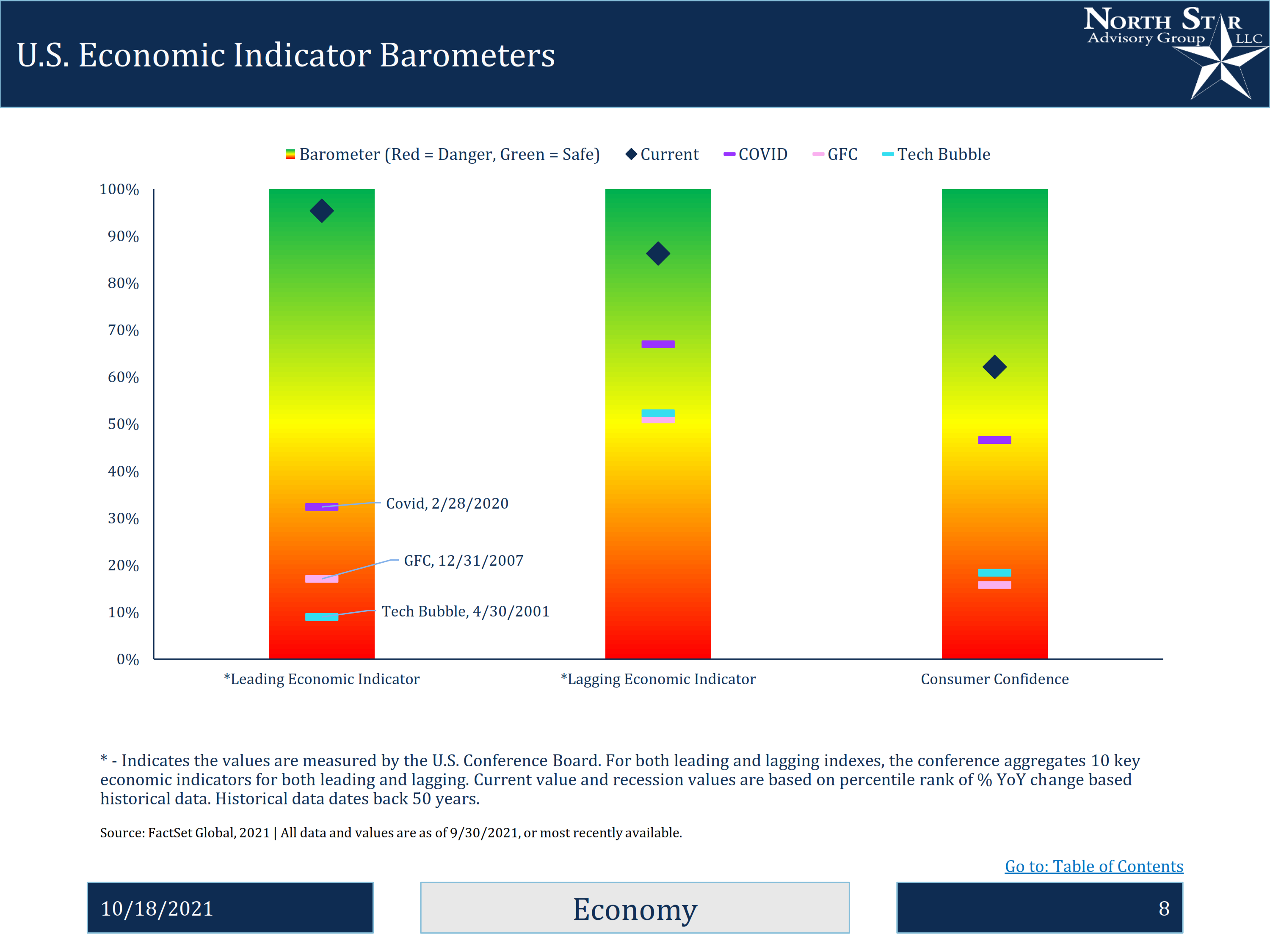

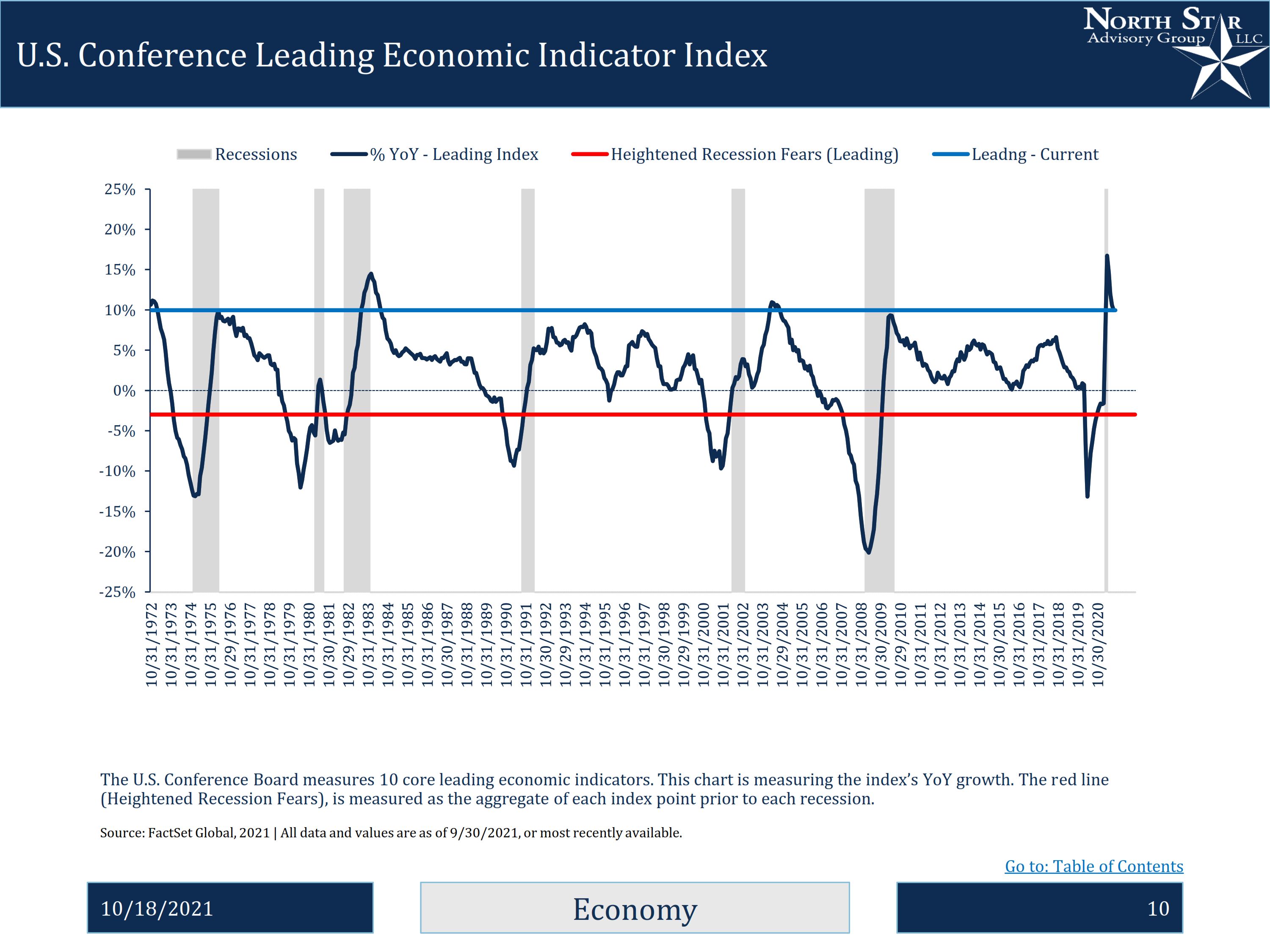

NSAG News - Recession risk remains at historic lows

NSAG’s research continues to show that the risk of a recession remains at historic lows. As professionals dedicated to continuing education, constant research and a high standard of ethics, we leave nothing to chance. Through virtually two decades, we have found that there’s something more powerful than luck, hope or hot tip when it comes to managing a portfolio’s allocation and risk. This month we unveil NSAG’s Raising your Investor IQ, a comprehensive view of Economic and Market conditions. NSAG has long relied on many of these data points to provide guidance to our portfolios and now we can update, share and expand this data each month.

One of the most accurate recession predictors has been the leading economic indicators. This indicator aggregates 10 key measures of where the economy is expected to go over the next few quarters. The current strength of the economy has only been experienced four times in the last 50 years and when we isolate to similar times just after a recession, the next recession was not experienced for another 5-10 years. While leading indicators tend to decline and bottom out prior to a recession occurring, lagging indicators tend to decline before the start of a recession and bottom out during the middle of the recession. At any time, it is not uncommon for one subcomponent to temporarily turn negative. The benefit of lagging indicators may be better used for providing insight as to when the end of a recession is near.

Click on either image to view the Full Document

Where will the equity markets go next?

As we showed above, the forward-looking earnings estimates continue to improve and the breadth of the recovery is wide. Both factors are supportive for the current level in the S&P 500 and additional modest growth into yearend. Analysts have underestimated the recovery from COVID and many investors have let their emotions sway their investment decisions. While the path forward will not be a straight line, we expect any pullbacks to be modest and focused on areas of bubbles and rising interest rates. The continued rotation from growth to value is likely to continue for at least the next year and should pick up steam as interest rates rise in connection with the Delta variant slowing down.

There continues to be virtually zero risk of a double-dip recession and the Federal Reserve is prepared to step in if necessary. We still believe we are in a secular bull market, which started in 2010 and typically lasts around 15-20 years. However, this secular market is likely to last longer.

We are passionately devoted to our clients' families and portfolios. Let us know if you know somebody who would benefit from discovering the North Star difference, or if you just need a few minutes to talk. As a small business, our staff appreciates your continued trust and support.

Please continue to send in your questions and see if yours gets featured in next month’s Timely Topics.

Best regards,

Mark Kangas, CFP®

CEO, Investment Advisor Representative