Each month we ask clients to spend a few minutes reading through our newsletter with the goal of raising their investor IQ. This month’s topics include:

- Back to school

- The more you know… Bonds can be risky!

- Student debt payment forgiveness & delays

- Olympics, metals & your portfolio

- NSAG news

- Where will the equity markets go next?

Back to school

In 1986, Rodney Dangerfield starred in “Back to School.” Dangerfield played character who was so worried about his son’s success in college that he also enrolled in the university! I know there are a few clients out there that have at least contemplated Dangerfield’s approach. Dangerfield eventually joined the dive team to further provide support his son. While Dangerfield’s execution of the legendary “Triple Lindy” dive helped the university win the championship, his larger-than-life presence on campus only made his son’s college life more difficult.

Fast forward to 2021… schools, colleges and universities are starting up and sending a child back this fall may seem more nerve racking than trying to pull off the infamous Triple Lindy.

With the help of Washington DC, the navigation of COVID maybe the market’s version of executing the Triple Lindy. Looking at Q2 earnings so far, companies have crushed top-line estimates. More than 80% of the companies that have reported Q2 results have beaten consensus top-line revenue estimates. Looking at that same cohort of stocks going back to 2001, there has not been another quarter with as strong of a revenue beat rate. While off the peak of 80% from Q3 last year, EPS beat rates are also historically strong at 77.06%. Given those beat rates, misses have been hard to come by, especially for revenues. Only 18% of companies have missed sales estimates this season; the lowest reading since Q1 2005.

While the surge in sales beats is impressive, the rate at which companies are raising guidance is even more impressive. That rate eclipsed 20% this quarter, a record by a wide margin and is also at a high going back prior to 2001.

In spite of the strength of the underlying fundamentals, the market can’t get no respect. And if it wasn’t almost 17 years after Rodney Dangerfield’s passing, I am sure he would agree.

The more you know… Bonds can be risky!

Interest rates sitting near historic lows have caused many bond funds to take more risk in their search for yield (or income). This is often done by buying longer dated maturities and/or lower quality bonds. NSAG has seen this trend continue to pick up steam over the last few years. NSAG works to maintain a very minimal exposure to these types of bonds. Why? High yield bonds have long been referred to as junk bonds. Their credit quality is substandard and to lure investors in, they have to offer a higher interest rate. While the income is attractive, the risk profile is not. From 1986 to 2021, junk bonds have had a correlation to stocks of 0.61 and a correlation to bonds of 0.24. Therefore, junk bonds are more likely to move with the U.S. stock market than the aggregate bond market. Most bond investors are buying bonds for downside protection, not equity like exposure.

From 1995 through 1999, junk bonds gained 60% versus an astounding 250% return for the S&P 500. The spread over the past five years (121% for stocks versus 42% for junk bonds) seems tame by comparison. The spread between these returns would be further apart if you removed the positive impact of falling interest rates on junk bonds.

With junk bonds yielding ~4.3% (near all-time lows), at the very least investors should be expecting below-average returns going forward. Beginning yields tend to be a pretty good predictor on that front. Generally speaking, the higher the starting yield, the higher the prospective returns, and vice versa. Layer on the negative impact of rising rates and the future is looking even less bright for junk bonds.

Not all bonds are created equal, and many investors are not respecting the inherent risks in high yield bonds. This public service announcement is brought to you by NSAG.

Student debt payment forgiveness & delays

The U.S. Department of Education announced Thursday it will cancel $5.8 billion in student debt for more than 320,000 borrowers. The debt forgiveness, which will go to borrowers with a total and permanent disability, will be automatically granted using data already available to the Social Security Administration. Borrowers should start seeing the relief in September 2021.

The Biden administration also announced earlier this month that it will extend the payment pause for federal student loan borrowers through January 2022. Debt forgiveness has allowed consumers to redirect loan payments into other purchases in the economy. In an attempt to put pressure on Congress and Senate, the White House said this will be the final extension. Biden is seeking student loan forgiveness between $10,000-$50,000. We continue to urge borrowers with less than $50,000 in debt to redirect loan payments into savings until final legislation is passed. It remains unclear if any forgiveness will be passed and if there will be an income threshold. Either way, it is extremely unlikely that the administration will provide any benefit for debt payments that have already been made.

Support is growing on both sides of the political aisle for student loan forgiveness. The amount of forgiveness remains the debate. Both announcements are positive for those who are hopeful for debt forgiveness.

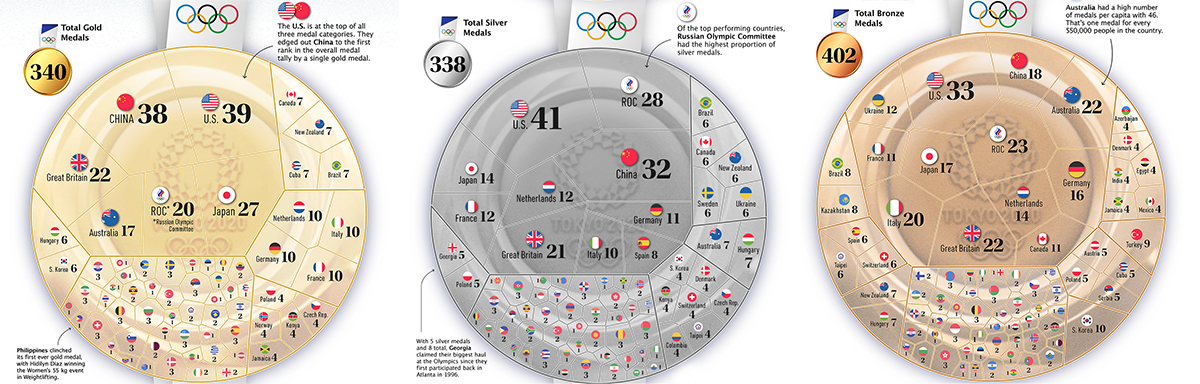

Olympics, metals & your portfolio

When the 2020 Olympics closed earlier this month, the United States athletes flew home with the largest medal count per country, with 113 total medals. Historically speaking, this a very minor haul compared to the 239 US medals from the 1904 St. Louis games and the 174 US medals from the 1984 Los Angeles games.

However, from a per capita basis, the US was ranked 59th with one medal for every 2.9 million residents. With less than 115,000 total residents, San Marino, Bermuda and Grenada have the highest medal per population counts.

At the Olympics, all first and second place winners took home silver. How? Gold medals are not pure gold. A pure gold medal would be too soft. Instead, they’re pure silver, with six grams of gold plating per medal. This creates a combined value of about $1,000 of precious metals per gold medal. Silver medals are the only ones made of a pure element and are valued around $550. While bronze is a well-recognized metal, it isn’t a pure element, and nor are the bronze medals technically bronze. They are brass and valued around $10 each. After reading this, many would be shocked to hear that Japan spent a total of $0 on all the metals for the Olympics! At Tokyo, 100% of the metals in the medals were recycled. Between 2017 and 2019, people across Japan donated old electronic devices, which had the precious metals extracted from them. In total, the government collected several million tons of equipment, and extracted 32 kilograms of gold, 3500 kilograms of silver and 2200 kilograms of copper and zinc for the bronze medals.

I am often asked about my suggested allocation for metals like gold and silver in portfolios. Generally, my ongoing recommended has been to allocate zero to minimal. Occasionally, there are very short-term trades or hedges could be made. Furthermore, I recommend holdings are in daily liquid ETFs where investors have minimal to no trading costs and have the ability to digitally increase or decrease their allocations. Metal performances have significantly underperformed other asset classes. Even during the inflationary summer of 2021, the values of these metals are falling. Since May 1st 2021, gold is +1%, silver is -9%, copper is -5% and platinum is -16%.

This summer’s deflationary pressures on metals have not only brought prices down, but also devalued the hard-earned medals from the Olympics, some of which are already being sold and auctioned off! The good news is that the awards were not made from lumber. That commodity is -69% since May 1st and now down 46% since January 1st.

NSAG news

|

In August, NSAG hired Kate Cizmadia as a second Client Service Specialist. She is responsible for coordinating client meetings, including scheduling, collecting and analyzing necessary information. In addition, she prepares client’s investment reviews and retirement cash flow projections, as well as assisting with the overall client relationship. |

Kate graduated from Cleveland State University in 2021 with a Bachelor’s Degree in Business Administration with a concentration in Finance and a Minor in Information Systems. Kate is currently studying for her certification as a Financial Paraplanner Qualified Professional™.

Kate lives in Westlake with her family, Labrador retriever Max and COVID kitten Ghost. Outside of work, she enjoys playing the piano and hiking in the Cleveland Metroparks. Kate’s favorite thing to do on the weekends is seeing live music and finding new restaurants to enjoy with friends.

Where will the equity markets go next?

In December 2020, we were expecting a strong year for the equity markets, and we were not let down. As we discussed above, the underlying fundamentals are strong and the breadth of the recovery is wide. Both factors are support for the current 4,400 level in the S&P 500 and additional modest growth into year-end. Analysts have underestimated the recovery from COVID and many investors have let their emotions sway their investment decisions. While the path forward will not be a straight line, we expect any pullbacks to be modest and focused on areas of bubbles and rising interest rates. The continued rotation from growth to value is likely to continue for at least the next year.

There continues to be virtually zero risk of a double-dip recession and the Federal Reserve is prepared to step in if necessary. We still believe we are in a secular bull market, which started in 2010 and typically lasts around 15-20 years. However, this secular market is likely to last longer.

We are passionately devoted to our clients' families and portfolios. Let us know if you know somebody who would benefit from discovering the North Star difference, or if you just need a few minutes to talk. As a small business, our staff appreciates your continued trust and support.

As a small business, our staff appreciates your continued trust and support as we all work through these stressful and trying times for our country and world.

Please continue to send in your questions and see if yours gets featured in next month’s Timely Topics.

Best regards,

Mark Kangas, CFP®

CEO, Investment Advisor Representative