Each month we ask clients to spend a few minutes to read through our newsletter with the goal of raising their investor IQ. To properly address client questions on bubbles and their potential impact on the markets, this month’s Timely Topics is a long one. Enjoy!

- Why are professionals optimistic while retail investors are pessimistic?

- Have you ever thought about cashing out of the market?

- The outlooks for equities is increasing, while it is decreasing for bonds

- COVID hospitalizations have peaked and are falling

- Bubbles, bubbles everywhere!

- Where will the equity markets go next?

Why are professionals optimistic while retail investors are pessimistic?

The majority of the good news is buried and not in the headlines.

Household debt service ratio is the amount of debt payments as a percentage of disposable personal income. During the pandemic, household debt has plummeted to levels significantly lower than any other level in the last 40 years.

High frequency data is tracking the year-over-year changes in various consumer data points and spending patterns. Purchase mortgage applications is the only data point that is up significantly at 26% year-over year. However, consumer debit/credit transactions are only down 9%. Hotel occupancy continues to recover along with TSA traveler traffic and US seated dinners. North Star has fielded many calls from clients inquiring about taking two family vacations in 2021 since they didn’t take one in 2020.

The combination of multiple federal stimulus programs has successfully fended off a depression and quickly brought down the civilian unemployment rate for private production and non-supervisory workers.

Global Purchasing Manufacturing Indices (PMI) for manufacturing and services quickly rebounded to expansionary levels.

While the US’s fiscal trillions of dollars response to COVID-19 sounds staggering, it only represents 14% of GDP. Many other countries have responded with 25-40% of their GDP.

While inflation remains a concern, technological innovation is doing a good job of keeping the consumer price index (CPI) and core CPI low. In fact, it remains persistently lower than the Federal Reserve’s 2% long-term average target. Lower for longer should let the Fed stay accommodative to low rates and stimulative programs.

Oil is in everything and oil prices are recovering. While this sector of our economy is small, it helps to bring back a weakened part of the economy and ultimately show that demand is slowly returning.

Have you ever thought about cashing out of the market?

I have two secondhand stories of non-North Star clients who sold out of their portfolio before the November election. While concerns were understandable and shared by many, these two stories took it a step further and transferred the cash to their bank so they could withdraw the cash and put it in a safe in their house! Let that sink in for a second… six to seven figures of cash sitting in a house that used to be invested in the market. Withdrawing this amount of cash is not an easy task or safe.

Fast forward almost three months later, and the S&P 500 is now up greater than 15% from the beginning of November. What are these former investors supposed to do now?

Think about the process for them to get back in… First, they must admit that they made a mistake. Waiting for the market to “pull back” may do even further damage to their potential earnings. They must go back to the bank with all the cash to be redeposited and have conversations with their advisors about putting the money back to work. Many of the concerns that they had when they went to cash are likely still in place, so it will likely take weeks or months to redeploy the cash into stocks.

While emotion is present in decisions throughout our lives, emotion should not drive investment decisions. North Star’s process helps to remove the emotion so investors can sleep at night and stay focused on their long-term goals.

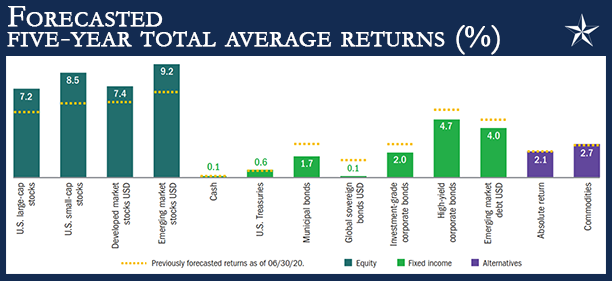

The outlooks for equities is increasing, while it is decreasing for bonds

In early January, North Star held an investment update meeting with Columbia. Columbia’s long-term strategic outlook aligns very closely with North Star’s views, so we thought we would share a few of their thoughts from our meeting.

On December 31, 2020, Columbia made a few significant changes to their five-year forward-looking forecast after adjusting their most recent forecasted returns to account for pandemic-driven volatility and global monetary policy. Overall, they raised their outlook for equities and decreased their outlook for bonds. The following are three trends that are driving Columbia’s updated forecast.

- Columbia expects economic growth to return to trend levels over the next five years and a recovery from the virus in the near term. If the vaccine rollout is successful this year, growth will likely be well above trend, as governments are following reflationary fiscal policies and central bankers are deploying expansionary monetary policies. At the same time, there’s a pent-up demand for many services.

- Inflation is likely to approach central bank targets sometime in the next five years, but not until the economy experiences lower levels of unemployment and labor market slack is eliminated. U.S. central bankers are focused on staying accommodative until broad employment measures approach historic lows.

- In anticipation of a recovery from a 2020 recession, we have higher estimates for equity returns over the medium term. Credit spreads have returned to precrisis levels and returns in fixed income are likely to be driven by bond yields. Monetary policy is likely to stay accommodative for the duration of our projections — return on cash is near zero and safe assets, such as treasuries or global sovereign bonds, are also likely to have very low returns.

Is now the time to invest into ESG?

U.S. attitudes towards environmental policy around protecting the environment and global climate change have steadily been increasing over the last decade. During the same time, inquiries into Environmental, Social & Governance (ESG) investing have increased from North Star’s clients. ESG investing focuses on companies that have a higher focus on with higher scores related to Environmental, Social & Governance. Due to the variety of investment options and personal objectives with ESG investing, it is important to start with a basic understand on the many ways to invest into ESG.

One of the ways to invest into ESG is through sustainable sector funds. These funds focus on "green economy" industries like renewable energy, energy efficiency, environmental services, water, infrastructure, and green real estate. Green economy companies can be found across a variety of conventionally defined sectors, and, according to one estimate, they constitute 5% of global market cap. Performance for many focused ESG funds like these have been negative for a decade with sky high performance over the last 6 months. This is a performance ride that most investors cannot stomach, and we have recommended against.

Diversified ESG funds exchange a milder ESG exposure to obtain a well-diversified portfolio. As a result, they tend to have low active risk and tracking error relative to the broader market. The right balance between ESG exposure and diversification is a matter of personal preference. With so many options available, there's likely a fund that aligns with your preference.

If you would like to learn more, we have an article that we can share that will walk you through the basics of EGS investing. Then North Star can help you look closer at how different funds approach ESG investing so we can appropriately weigh the pros and cons of each option.

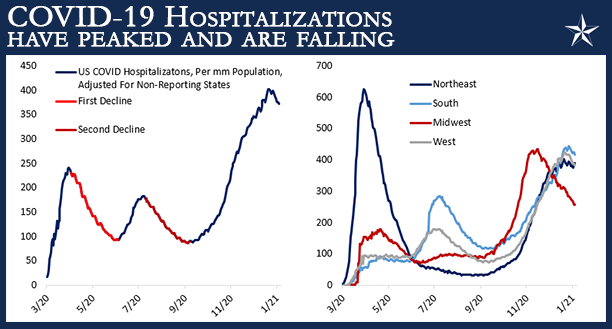

COVID hospitalizations have peaked and are falling

While the number of deaths due to COVID hit a record in data reported out yesterday, other data on COVID has turned positive in the past week. Testing remains very high, new cases have dropped, and perhaps most importantly, hospitalizations are dropping nationally. In the charts below, we show per capita hospitalization over the course of the pandemic, with three clearly defined surges. The initial pandemic broke out in March, driving a surge in tristate area hospitalizations as well as a few other parts of the country. Summer temperatures forced the Sunbelt indoors, sending hospitalizations spiking in warmer states like Arizona, Texas, and Florida. Then the fall surge arrived as hundreds of thousands were hospitalized thanks to surging caseloads in colder states. The Midwest got hit first, but eventually the whole country experienced a large uptick. Thankfully, the most recent surge appears to have petered out, and the prior two precedents suggest declines will persist.

For equity market investors, the question is what to own amidst a receding pandemic backdrop? The prior two declines in hospitalization lasted about two months from the first week-over-week decline to the subsequent first week-over-week increase. The patterns of outperformance weren't exactly the same across both periods, but in general, investors were well-served by exposure to Materials, Consumer Discretionary, and Small Cap stocks. Utilities, Consumer Staples, and Health Care were the worst sectors to own, though they did okay in the second downslope; Energy and Financials did worst for that period specifically. Surprising many, Technology was not the best sector to own in the second decline, the 4th quarter of 2020 or even January 2021.

Bubbles, bubbles everywhere!

Clients are inquiring about where we are seeing asset bubbles. We are already preparing a section to address this client question for February’s Timely Topics. Stay tuned to see where we see them forming.

Where will the equity markets go next?

COVID-19 numbers appear to be topping out and economies may be seeing light at the end of the tunnel. In December 2020, we were seeing a growing probability of the S&P 500 hitting 4,200 by the end of the year 2021. The breadth of the recovery we are seeing for the balance of 2021 along with some technical analysis, may see the S&P 500 exceed these numbers. While the path forward will not be a straight line, we expect any pullbacks to be modest. The markets should continue to be supported by the Federal Reserve, stimulus from central banks around the world, cash on the sidelines, low interest rates, recovering earnings and investors who overallocated to bonds.

We still believe we are in a secular bull market, which typically lasts around 15 years. Historically, it is not uncommon to have a bear market (which essentially occurred in Q4 of 2018) or even a brief recession (which we may be experiencing right now) during a secular bull market. Vaccine deployment is going to take the headlines for the next few months as we head into a really rough patch of time for the economy. On the bright side, it should be short lived and we should have a strong second half of 2021.

We are passionately devoted to our clients' families and portfolios. Let us know if you know somebody who would benefit from discovering the North Star difference, or if you just need a few minutes to talk.

As a small business, our staff appreciates your continued trust and support as we all work through these stressful and trying times for our country and world.

Please continue to send in your questions and see if yours gets featured in next month’s Timely Topics.

Best regards,

Mark Kangas, CFP®

CEO, Investment Advisor Representative