Each month we ask clients to spend a few minutes to read through our newsletter to with the goal of raising their investor IQ. What should investors be focusing on this month?

Here are the key topics that we cover this month:

- November is a time to pause and give thanks

- Expect the US Dollar to weaken

- Stock markets are looking beyond near-term risks

- A lesson from history: The mistake of selling out of fear in the fall of 2020

- November’s manufacturing data shows continued strength

- Client question: What does JP Morgan’s negative GDP forecast for Q1-2021 mean for my portfolio?

- Where will the equity markets go next?

November is a time to pause and give thanks

Wall Street continues to search for solid ground amid a tug-of-war between the optimism of the coming vaccines and the continuing spread of the pandemic. Investors are concerned over the pending “dark winter” in which we are expecting to see the number of COVID cases continue to climb until we get into mid to late January. This month, we focus on a few key topics and questions which have been raised by clients.

Expect the US Dollar to weaken

Every few months concerns arise over the fall of the “US Empire” and the role that the US Dollar plays as the reserve currency around the globe. While the reason for the change differs over time, we still do not see it happening any time soon. While the US Dollar will remain the reserve currency for the world, we expect it will continue to soften for three reasons.

First, a reduction in uncertainty on a number of fronts, including the election, global trade and relations with China, to name a few. Most people forget that in 2018-2020, the US Dollar rose by 10%, mostly due to trade war. A softening of the US Dollar should provide a tailwind for international and emerging market equities.

Second, the US is likely headed toward a divided Congress in 2021, which historically leads to less dramatic change and lower market volatility. This environment produces a “Goldilocks” effect: the equity markets are not too hot or too cold. Reduced volatility may lead to see investment dollars being placed into global markets instead of being parked into the US markets, which are perceived as more stable.

Finally, while interest rates in the US have been low, the US’s rates have been generally higher than 75% of rates available in other developed countries until recently. Foreign capital has flown into US Bonds, driving the US Dollar up and bringing down the US’s interest rates into parity with rates in other countries. US Dollar demand could decrease as rate volatility appears to have stabilized and the differential between interest rates in the US vs. Europe vs. Japan will likely stay in a narrow range.

Stock markets are looking beyond near-term risks

Bob Doll, Chief Equity Strategist at Nuveen Asset Management, provided the following commentary to help North Star clients understand why stocks are holding up in spite of political and COVID news.

In November, investors have focused on the positive coronavirus vaccine trials, as well as the negatives surrounding spiking virus cases and mounting economic lockdowns around the world. Diminishing prospects for a near-term fiscal stimulus package also weighed on the markets. As a result, global equity prices were mixed. The rotation away from defensive areas toward more cyclical parts of the market continued, as energy, industrials, materials and financials all outperformed, while utilities and REITs lagged.

Bob’s ten observations and themes:- Financial markets have been focusing on the positives in recent weeks. Stocks have been largely ignoring the rising coronavirus cases, as investors are looking forward to vaccine availability and prospects for stronger economic growth in 2021.

- While stock prices have been rising, high yield credit spreads have been narrowing. The improving economic outlook, better-than-expected earnings growth and increased liquidity have been sparking a risk-on trading phase.

- Investor sentiment has improved sharply. Net bullish sentiment, as measured by the American Association of Individual Investors, rose from neutral to sharply bullish over the past several weeks. From a contrarian perspective, this suggests stocks could be vulnerable to a pullback.

- More near-term economic pain is likely. New cases in Europe have been surging for some time, and rising U.S. infection rates are overwhelming some regions’ health care systems. Policymakers also expect this week’s Thanksgiving holiday could trigger an accelerated surge. All of this suggests that economic disappointments are likely over the coming months.

- A lack of near-term fiscal stimulus is weighing on consumer spending. Retail sales rose only 0.3% in October, quite less than expected.

- Manufacturing and production, in contrast, have held up well. Industrial production grew by 1.1% in October, above consensus expectations.

- Global central banks continue to flood the markets with liquidity. Collectively, the assets of the U.S. Federal Reserve, the European Central Bank and the Bank of Japan rose from $7.2 trillion in March to a record $21.8 trillion in November. All three are also pushing their country’s fiscal policymakers for additional stimulus.

- Fiscal and monetary policymakers remain far apart. Last week’s news that Treasury Secretary Mnuchin requested terminating several Fed lending programs (and the Fed’s criticism of these plans) provides further evidence that it will be difficult to manage through economic turmoil in the coming months.

- Corporate earnings have held up surprisingly well this year. S&P 500 2020 consensus earnings are now at $137, down only 15% year over year. Should that level hold, it would mark the mildest earnings recession since 1960.

- Regulatory policies are likely to tighten in 2021. Next year, we expect President-elect Biden to advance a robust regulatory agenda that reverses much of President Trump’s policies implemented over the past four years. The bulk of the action will likely be concentrated in energy, climate change and labor areas.

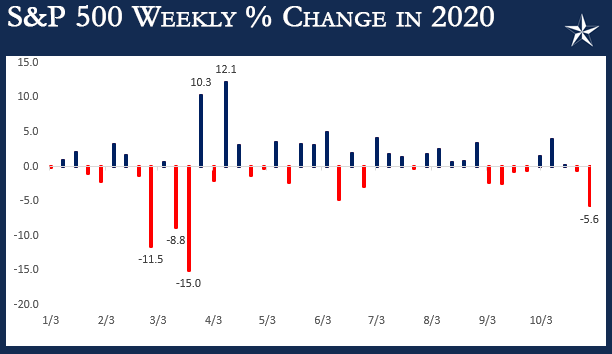

A lesson from history: The mistake of selling out of fear in 2020

We devoted a good section of October’s Timely Topics to help educate clients about selling out of fear. Why? From conversations with clients, we could hear fear on the horizon. Between rising COVID cases around the country, pending election, and lackluster reactions to solid earnings reports, there were more than a few concerns on the minds of investors heading into the last two months of the year. Fast forwarding a few weeks, the S&P 500 finished the last week of October with a decline of 5.6% for the week. As visible from the following chart, this week ranked as the worst week since March and the fourth-worst week of the year.

November has been a strong month for the US equity markets, but sometimes putting numbers on the totals helps to put it in perspective. The Russell 3000, which encompasses large, mid, and small caps stocks, was up 9% in the first week of November! In most years, that's considered a good year, and it was only five trading days.

In terms of sectors, energy and communication services lead the way followed by, real estate, industrials and financials with average returns ahead of the Russell 3000. One sector notably absent from the list of outperformers is technology. That sector normally tops the list during periods of market strength, but the NASDAQ’s performance so far this month is 2.5% behind the Russell 3000. With technology stocks averaging a gain of 6.2%. It's at the back of the pack, but it's hard to consider the NASDAQ weak.

The massive change over these two weeks is one reason why encourage clients not to try to time the market.

November’s manufacturing data shows continued strength

All-told, the flash PMI data was about as constructive as anything we’ve seen on the US economy since the start of the post-April rebound earlier this year.

- While some metrics that track consumer spending or the labor market have fallen off a bit in November, Markit’s Flash PMIs for the US showed a downright impressive backdrop.

- Manufacturing leaped to its highest reading since 2014, after a smaller gain in October.

- New orders rose at the fastest pace in two-and-a-half years, fueled by domestic orders given only modest improvement in new export orders.

- Unlike in Europe, where new COVID restrictions hurt Flash PMI readings for November, US data showed another rise in the headline data.

- Similar to manufacturing, this indication of services sector activity is at the highest levels since 2015.

- Services saw similar order growth, with a very strong (in fact, the strongest since at least 2009, when the survey began) employment number.

- On a composite basis (which weighs manufacturing and services by their respective shares of output), November saw the strongest US activity growth in more than five years.

- There are also signs in both manufacturing and services that the recovery in activity is becoming increasingly self-sustaining, meaning it is not being influenced by outside sources, such as the Federal Government.

- In addition to surges in backlogs, cost pressures are mounting as supply markets tighten; that tightness is likely to lead to more production and hiring down the road.

Client question: What does JP Morgan’s negative GDP forecast for Q1-2021 mean for my portfolio?

Gross domestic product (GDP) is a monetary measure of the market value of all the final goods and services produced in a specific time period. To put things in perspective, the quarterly GDP for the US typically ranges between +2 to +3%.

Last week, JPMorgan became the first major bank to predict that the US’s GDP in Q1-2021 will decline by 1% because of the COVID surge. We ran a comparison of the US’s quarterly GDP vs S&P 500 from 2001-2020. While past performance is not indicative of future results, we did not find a significant impact on the quarterly returns for the S&P 500 when the US’s GDP was between zero and -2.5%. We also found that once we got two to three quarters out from the initial impact of a GDP event, the market impact was significantly muted. Interestingly enough, we also didn’t find a significant impact on the quarterly returns for the S&P 500 when the US’s GDP was greater than 5%.

We are expecting a soft quarterly GDP for Q1-2020, but not nearly as negative as the impact on GDP in early 2020 due to the countrywide shutdowns. Almost a year after the initial shock of COVID and a potentially minimally negative GDP, the impact on portfolios should be very muted.

Where will the equity markets go next?

We still believe we are in a secular bull market, which typically lasts around 15 years. Historically, it is not uncommon to have a bear market (which essentially occurred in Q4 of 2018) or even a brief recession (which we may be experiencing right now) during a secular bull market. The Fed and Treasury are doing a tremendous job of providing a financial bridge to get through COVID, but more stimulus will be needed. The next round of stimulus will occur, but probably not until after Biden’s inauguration in January 2021.

We are passionately devoted to our clients' families and portfolios. Let us know if you know somebody who would benefit from discovering the North Star difference, or if you just need a few minutes to talk.

As a small business, our staff appreciates your continued trust and support as we all work through these stressful and trying times for our country and world.

Please continue to send in your questions and see if yours gets featured in next month’s Timely Topics.

Best regards,

Mark Kangas, CFP®

CEO, Investment Advisor Representative