Each month we ask clients to spend a few minutes to read through our newsletter to with the goal of raising their investor IQ. What should investors be focusing on this month?

Here are the key topics that we cover this month:

- Washington & your portfolio

- A lesson from history: The mistake of selling out of fear

- Expect delays as nationwide productivity is slowing

- NSAG’s call w/ Jamie Diamond, CEO of JP Morgan Chase

- Recap, reply & two additional calls - What to expect in November’s Election

- Airline travel hits milestone while slowly recovering

- Charles Schwab completes acquisition of TD Ameritrade

- Free weekly online credit reports

- Where will the equity markets go next?

Washington & your portfolio

While the 2020 election season is finally winding down, we are likely to see prolonged controversy after November 3. Several betting markets and election experts currently give former Vice President Biden a lead over President Trump for winning, and Democrats are also the favorite for the Senate and House. The Senate is arguably the most important to follow and the control is narrowing and coming back to a virtual 50/50 tie. Of all elections of the post-WWII era, there have been six other Democratic sweeps of the Presidency, House, and Senate. We can always argue that “this time is different.” Democratic sweeps have typically come on market weakness both before and after Election Day. In these years, the S&P 500 has been down an average of 2.6% in the three months leading up to Election Day. Immediately after the election, there has historically been further downside pressure over the next few weeks, though those losses are reversed a bit afterward. By three months after the election, the S&P 500 has found itself at similar levels as Election Day on an average basis. Currently, we are expecting downside volatility to be short lived and be less than 10%.

October 2, it was announced that President Trump tested positive for COVID-19 and later that night was moved to Walter Reed National Military Medical Center for observation and treatment. Trump received a treatment of Dexamethasone, Remdesivir and Regeneron in addition to his current regiment of zinc, vitamin D, famotidine, melatonin and aspirin. While his case was thought to be mild, he was released three days later back to the White House. Trump’s positive COVID test caused the cancellation of one Presidential debate and changed the format of the third debate on October 22. Selling stocks on Trump’s COVID news would have been detrimental as the market has continued to move higher on hopes of an agreement for the next round of planned fiscal stimulus from Washington.

We believe it is unlikely that we will see a pre-election stimulus package and discuss this further in the following section “What to expect in November’s Election.” After the election, it is possible to see a $2 trillion package followed by an additional $4 trillion for infrastructure in early 2021 (originally slated as a $2 trillion bill for Q4 2020).

Expect the US Dollar to weaken

Every few months concerns arise over the fall of the “US Empire” and the role that the US Dollar plays as the reserve currency around the globe. While the reason for the change differs over time, we still do not see it happening any time soon. While the US Dollar will remain the reserve currency for the world, we expect it will continue to soften for three reasons.

First, a reduction in uncertainty on a number of fronts, including the election, global trade and relations with China, to name a few. Most people forget that in 2018-2020, the US Dollar rose by 10%, mostly due to trade war. A softening of the US Dollar should provide a tailwind for international and emerging market equities.

Second, the US is likely headed toward a divided Congress in 2021, which historically leads to less dramatic change and lower market volatility. This environment produces a “Goldilocks” effect: the equity markets are not too hot or too cold. Reduced volatility may lead to see investment dollars being placed into global markets instead of being parked into the US markets, which are perceived as more stable.

Finally, while interest rates in the US have been low, the US’s rates have been generally higher than 75% of rates available in other developed countries until recently. Foreign capital has flown into US Bonds, driving the US Dollar up and bringing down the US’s interest rates into parity with rates in other countries. US Dollar demand could decrease as rate volatility appears to have stabilized and the differential between interest rates in the US vs. Europe vs. Japan will likely stay in a narrow range.

A lesson from history: The mistake of selling out of fear

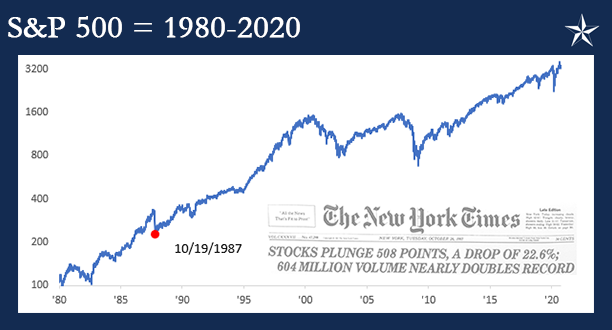

Thirty-three years ago (10/19/87), US equity markets experienced their worst single day decline on record as the S&P 500 fell 20.5% while the Dow dropped more than 22%. If you were alive or old enough to remember things at the time, you remember the 1987 crash. In the case of the Dow, it wasn't the worst single-day decline on record as the index dropped more than 23% on 12/12/1914, but the caveat here is that the 1914 decline came after a nearly five-month stretch where the stock market was closed due to World War I. In 1987, the only closure the crash followed was a two-day weekend.

While the crash of 1987 surprised most investors, it wasn't as though the weakness came out of the blue. In the two months leading up to the crash, the S&P 500 was already under significant pressure leading up to that day. For example, from the closing high on 8/25/1987 through the close on the Friday before the crash, the S&P 500 was already down more than 16%!

With the market already down 16% heading into the Monday crash, you wouldn't have faulted an investor for thinking the sell-off was overdone and putting some money to work right before. As the saying goes, buy low and sell high, right? While that approach may have sounded good in theory, in practice it was a disaster. It didn't take long before that initial investment was already down more than 20%, putting the investor in what would have seemed like an insurmountable hole.

Picking up a copy of the New York Times on 10/20/1987 would have only reinforced that sentiment. While they are more frequent now, headlines that spanned the entire front page used to be extremely rare, but the day after the crash, that's exactly what we saw, including one headline which read, "Does 1987 Equal 1929?" Given the sheer size of the decline and the headlines, it was reasonable for an investor to cut their losses and move on.

While the New York Times deemed the crash of 1987 as an event worthy of the entire front page, the Wall Street Journal took a more reserved approach dedicating just two columns to its main headline, and explaining that in reference to the question "A Repeat of '29?" that a "Depression in '87 Is Not Expected."

With the benefit of hindsight, while it was understandable for an investor to sell the day after the crash, it was the entirely WRONG move, as Black Monday essentially marked the low of that bear market. The '87 crash obviously looked disastrous on a short-term intraday chart of the S&P 500 from 1987, but from a longer-term perspective, it looks a lot less intimidating. The chart below shows the S&P 500 on a log-scale going back to 1987, and from this perspective, the 1987 crash now looks like a minor blip.

To further illustrate this point, let's take the theoretical example of the person who plowed some money into the stock market on the day before the crash. From a timing perspective, it couldn't have been worse. With the benefit of time, though, an investor who held on for the ride actually fared pretty well, even outperforming long-term Treasuries. As shown in the chart below, the S&P 500's annualized total return from the Friday before the '87 crash through this past Friday works out to 9.9%. Long-term US Treasuries have also performed well over the same time period, but with an annualized gain of 8.7%, they've underperformed the S&P 500. While past performance is not indicative of future results, the ability of long-term treasuries to keep up with equities is going to be virtually impossible. The average 10-year treasury yield in 1987 was 8.4%, compared to <1% in 2020!

The lesson here is clear: even the worst-timed trade ever worked out in the long-term. Panic selling after steep market drops throughout history has been the wrong move 100% of the time if your time frame is long enough.

A lesson from history: The mistake of selling out of fear in 2020

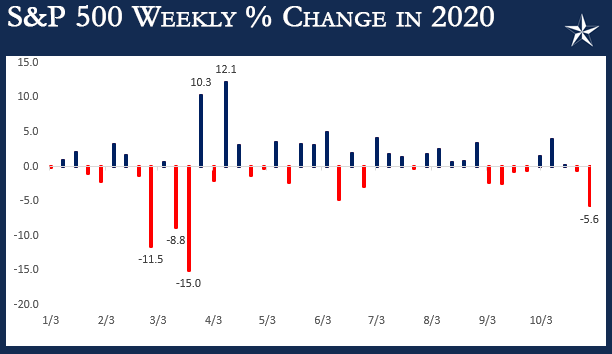

We devoted a good section of October’s Timely Topics to help educate clients about selling out of fear. Why? From conversations with clients, we could hear fear on the horizon. Between rising COVID cases around the country, pending election, and lackluster reactions to solid earnings reports, there were more than a few concerns on the minds of investors heading into the last two months of the year. Fast forwarding a few weeks, the S&P 500 finished the last week of October with a decline of 5.6% for the week. As visible from the following chart, this week ranked as the worst week since March and the fourth-worst week of the year.

November has been a strong month for the US equity markets, but sometimes putting numbers on the totals helps to put it in perspective. The Russell 3000, which encompasses large, mid, and small caps stocks, was up 9% in the first week of November! In most years, that's considered a good year, and it was only five trading days.

In terms of sectors, energy and communication services lead the way followed by, real estate, industrials and financials with average returns ahead of the Russell 3000. One sector notably absent from the list of outperformers is technology. That sector normally tops the list during periods of market strength, but the NASDAQ’s performance so far this month is 2.5% behind the Russell 3000. With technology stocks averaging a gain of 6.2%. It's at the back of the pack, but it's hard to consider the NASDAQ weak.

The massive change over these two weeks is one reason why encourage clients not to try to time the market.

Expect delays as nationwide productivity is slowing

NSAG has been back in the office since June and our productivity has increased; we hired our second Paraplanner in June 2020. However, we are seeing firsthand that working from home is now slowing productivity across the country at both large and small companies. There has been a decided change in productivity as of July this year. Initially at the start of COVID, the work from home productivity was high as workers pushed hard to help keep their jobs and the economy moving forward. Self-motivated workers can be productive no matter where they work, while others can be easily distracted. Kids learning from home are probably the biggest current distraction. However, we are also hearing that limited access to support technologies like faxes, scanners, printers, business speed/capacity internet, and office phone systems are also contributing to reduced productivity.

Our concerns were affirmed on Mark’s October call with Jamie Diamond (below).

NSAG’s call with Jamie Diamond, CEO of JP Morgan Chase

On October 1, Mark had an opportunity to sit in on small group meeting with Jamie Diamond. The following are a few of Jamie’s highlights from the call:

- There is a small chance of a double dip, so don’t rule it out.

- We are experiencing a bifurcated economy. If you are in the retail, hospitality and restaurant industry, you feel terrible. However, the consumer spending and housing-focused businesses are thriving.

- While initial productivity was high when workers went home for COVID in March, productivity has dropped significantly in the last few months.

- Chase is finishing up a comprehensive productivity research project. While they initially thought they would be able to have a high percentage of employees work from home in the future, they have found that as little as 30% actually can. Many companies like theirs are built on apprenticeship and in-person teaching. This summer alone, Chase had 3,000+ interns that never worked with someone one-on-one.

- Chase is looking to rebuild a long-term sustainable effort to put banking back into communities of the country that are not served by any bank. These are likely the same communities that banks pulled out of years ago due to lack of profitability. It will be interesting to see how long these new branches can last if they are not able to be profitable.

Recap, reply & two additional calls - What to expect in November’s Election

October 7, Frank Kelly, who is the Head of Government & Public Affairs for North & Latin America for Deutsche Bank, provided an update on the election and answered client questions. The following are a few of Frank’s highlights from the call:

- When you throw out the highest and lowest state polls, Biden & Trump are much closer than the media is letting us believe.

- The Shy voter swing for Trump could be as much as a 5% deviation in his favor.

- The Senate race is tightening up. There was a 60% chance that the Democrats took the senate a week ago. It is now a 50/50 toss-up without taking into consideration a sexting scandal developing in the NC race.

- Delays in the races/polls could be as long as 2-7 weeks. There are currently 200 lawsuits on how states are managing vote counting. The key battleground state of PA has expanded voting days to November 3, 4, 5, 6 & 7!

- It is very unlikely that we will see a stimulus program before the election.

- President Trump wants one-off packages so they are cleaner and more direct. Pelosi can only get support for a massive package.

- Pelosi is looking for a $2.2T+ package. Trump offered a $1.5T package.

- Either way… the Senate will not approve a package larger than $500B. Therefore, even if Trump and Pelosi agree on a number, the Senate is still not likely to approve.

- The massive $4T stimulus program for infrastructure is being pushed back from this fall to the spring of 2021.

- US/China Relations did not come up in the debate because both the Democrats and Republicans generally agree on this topic.

- Something is structurally wrong inside of China (income inequality, corruption, COVID death rates and they are attacking every other western country).

- The new division of our defense department called the Space Force will grow by over 6,200 personnel in the next year and has been allocated a budget of $15B for 2021.

Our October 7 call with Frank Kelly went so well, we were able to secure two more times with Frank. On call #2 & #3, Frank will provide his insight into what is going on behind closed doors in Washington on stimulus negotiations and what he is seeing real time as we head towards the November 3 election.

| Date & time | #2 = Thursday October 22 @ 2pm EST, each call will be ~50 minutes. #3 = Tuesday October 27 @ 2pm EST |

| R.S.V.P. | events@ns-ag.com |

Airline travel hits milestone while slowly recovering

The airline industry may be in crisis, but October 18 marked a big milestone for the industry. US total passenger throughput crossed back above the one million level for the first time since March 16. While the trend is higher, it is still down by a lot. Normal throughput is ~2.6 million passengers a day. Therefore, this recent milestone is still down more than 60% from the same day last year!

Looking deeper into the numbers, we continue to find positive trends. The increase in passenger traffic wasn't just a one-day blip. On a seven-day average basis, daily passenger traffic has also been steadily rising. Ten days ago, the seven-day average jumped back above the prior post-COVID high of ~780K from early September. Since then, we have seen a steady increase to the current level of ~872K, which is nearly 100K above the prior high.

Charles Schwab completes acquisition of TD Ameritrade

As you may have seen, the deal with TD Ameritrade officially closed on October 6.

We are excited about the potential benefits to our clients of what's on the horizon with the combined scale, technologies and product offerings.

It is important to know that for now, things remain business as usual. Schwab Advisor Services and TD Ameritrade Institutional will remain separate custodians until the account conversion is complete, and we expect that to take between 18 and 36 months. Mark has quietly heard that due to the size of the two firms, the integration could take up to 60 months. We will keep you apprised of important updates as we move through the process together.

Free weekly online credit reports

Credit reports may affect your mortgage rates, credit card approvals, apartment requests, or even your job application. Reviewing credit reports may also help you catch signs of identity theft early.

During these times of COVID-19, accessing your credit is important. That's why Equifax, Experian and TransUnion are now offering free weekly online reports through April 2021. Annualcreditreport.com is one of many sites that consumers can use to access the free reports.

Where will the equity markets go next?

As we sit less than 5% below market highs, our vision and communication has not changed since 2010. We still believe we are in a secular bull market, which typically lasts around 15 years. Historically, it is not uncommon to have a bear market (which essentially occurred in Q4 of 2018) or even a brief recession (which we may be experiencing right now) during a secular bull market. Markets will trade on fear or momentum from time-to-time. In-between earnings reports, the markets may even trade on a single data point (like Trump’s COVID test or stimulus updates). Eventually, the markets return to trading on fundamentals. We believe that fundamentals are slowly rebuilding across the globe. But the gains will be clouded until we get the first (or second) approved vaccine. Meanwhile the Fed and Treasury are doing a tremendous job of providing a financial bridge to get through the end of the year. The next round of stimulus will occur, but probably not until after the election.

We are passionately devoted to our clients' families and portfolios. Let us know if you know somebody who would benefit from discovering the North Star difference, or if you just need a few minutes to talk.

As a small business, our staff appreciates your continued trust and support as we all work through these stressful and trying times for our country and world.

Please continue to send in your questions and see if yours gets featured in next month’s Timely Topics.

Best regards,

Mark Kangas, CFP®

CEO, Investment Advisor Representative